A look at the fair value of Parker-Hannifin Corporation (NYSE:PH)

")

How far is Parker-Hannifin Corporation (NYSE:PH) from its intrinsic value? Using the most recent financial data, I’m going to examine whether the stock is fairly valued by taking the expected future cash flows and discounting them to today’s value. I’m going to use the discounted cash flows (DCF) model. This may sound complicated, but it’s actually quite simple! Anyone interested in learning more about intrinsic value should check out Simply Wall St’s analysis model. If you’re reading this and it’s not September 2018, I highly recommend you check out the latest calculation for Parker-Hannifin by following the link below.

Check out our latest analysis for Parker-Hannifin

The calculation

I use the two-stage growth model, which simply means that we consider two stages of growth of the company. In the initial stage, the company may have a higher growth rate, and in the second stage, a stable growth rate is usually assumed over time. In the first stage, we need to estimate the company’s cash flows for the next five years. To do this, I used the consensus of the analysts covering the stock, as you can see below. I then discount the sum of these cash flows to get an estimate of the present value.

5-year cash flow forecast

|

2019 |

2020 |

2021 |

2022 |

2023 |

|

|

Leveraged FCF (in million US dollars) |

1.73 thousand € |

1.87 thousand € |

1,61,000 USD |

2,11,000 USD |

2,10,000 USD |

|

source |

Analyst x8 |

Analyst x8 |

Analyst x3 |

Analyst x1 |

Estimated -0.42% |

|

Present value discounted at 11.05% |

1.56 thousand € |

1,52,000 € |

1.17 thousand US dollars |

1,39K € |

1.24 thousand € |

Present value of 5-year cash flow (PVCF)= 6.88 billion US dollars

After calculating the present value of future cash flows in the first 5-year period, we need to calculate the terminal value, which takes into account all future cash flows after the first period. For various reasons, a very conservative growth rate is used, which cannot exceed that of GDP. In this case, I used the interest rate on 10-year Treasury bonds (2.9%). In the same way as with the 5-year “growth” period, we discount this to today’s value at a cost of equity of 11.1%.

Final value (TV) = FCF2022 × (1 + g) ÷ (r – g) = $2.10 billion × (1 + 2.9%) ÷ (11.1% – 2.9%) = $26.65 billion

Present value of terminal value (PVTV) = TV / (1 + r)5 = 26.65 billion US dollars ÷ (1 + 11.1%)5 = 15.78 billion US dollars

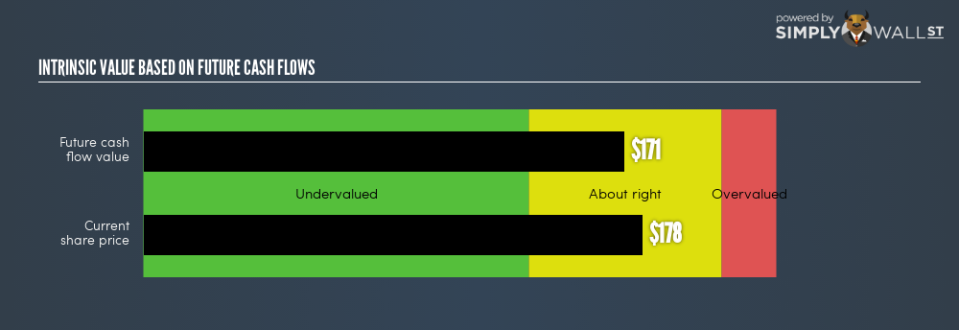

The total value is the sum of the next five years’ cash flows and the discounted terminal value, which gives the total value of equity, which in this case is $22.66 billion. To get the intrinsic value per share, we divide it by the total number of shares outstanding, or the equivalent number if it is a depositary receipt or ADR. This results in an intrinsic value of USD 171.17Compared to the current share price of $177.72, the stock is fairly valued, possibly slightly overvalued, and not currently available at a discount.

Important assumptions

The above calculation relies heavily on two assumptions. The first is the discount rate and the other is the cash flows. You don’t have to agree with my inputs, I recommend repeating the calculations yourself and playing around with it. Since we are considering Parker-Hannifin as potential shareholders, the cost of equity is used as the discount rate and not the cost of capital (or weighted average cost of capital, WACC) which takes debt into account. In this calculation, I used 11.1% which is based on a leveraged beta of 1.15. This is derived from the bottom-up beta method based on comparable companies, with an imposed limit of between 0.8 and 2.0 which is a reasonable range for a stable company.

Next Steps:

Valuation is only one side of the coin when developing your investment thesis and should not be the only metric you consider when researching a company. For PH, I have compiled three key factors to examine in more detail:

-

Financial health: Does PH have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors such as leverage and risk.

-

Future income: How does PH’s growth rate compare to its competitors and the overall market? Learn more about analyst consensus numbers for the coming years by using our free chart of analyst growth expectations.

-

Other high-quality alternatives: Are there other high-quality stocks you could hold instead of PH? Explore our interactive list of high-quality stocks to get an idea of what else you might be missing out on!

PS. The Simply Wall St app calculates a discounted cash flow for every stock on the NYSE every 6 hours. If you are looking for the calculation for other stocks, just search here.

To help our readers look beyond the short-term volatility of the financial market, we aim to provide you with long-term focused research analysis based solely on fundamental data. Please note that our analysis does not take into account the latest price-sensitive company announcements.

The author is an independent writer and had no ownership interest in any stocks mentioned at the time of publication. If you find any errors that need to be corrected, please contact the editor at [email protected].

Bill Gates uses these 4 tricks to read 50 books a year, but reveals his only problem with reading: “If I don’t agree with the book …”

Has the Utah Hockey Club mastered its first NHL draft? – Deseret News