Best Buy Stock: A Value Trap (NYSE:BBY)

")

wtstock

A quick look at Best Buy (NYSE: BBY), the giant electronics retailer, can tell the casual investor that this is a great, classic value investment. Best Buy is a stock that currently trades at a below-market valuation multiple, pays a dividend of nearly 5%, and may Benefit from a device refresh cycle following groundbreaking AI announcements from many tech brands: what’s not to like?

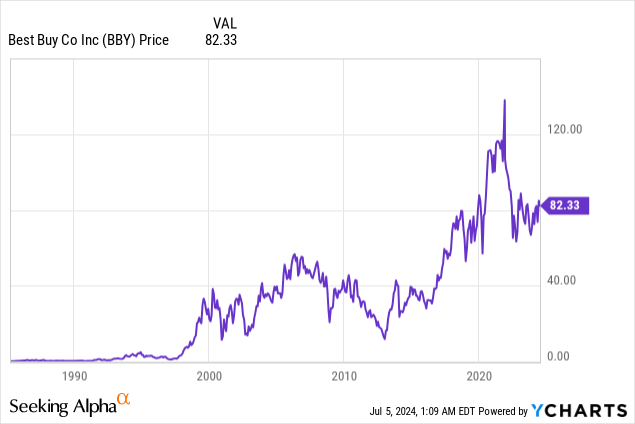

However, in my opinion, confidence in Best Buy is misplaced. The stock is up ~7% year-to-date and currently offers a 4.6% dividend yield, but I think ongoing risks are likely to put downward pressure on the share price as the year progresses.

I last wrote a bearish opinion on Best Buy in January, when the stock was trading closer to $75 per share. Best Buy has risen slightly since then, but has underperformed the broader market. I continue to point out a sell Rating for this stock because I believe two factors will undermine investor confidence in this name in the short term:

- Decline in sales growth in existing stores. It is important to note that Best Buy relies on sequential improvement in like-for-like sales, but we have not yet seen any indication that this is possible. In fact, first quarter sales growth was at the lower end of the company’s original guidance.

- The cash flow is low, and the Company’s shareholder return program exceeds the Company’s earnings on an FCF basis.

Below are the longer-term risks I see for Best Buy:

- More and more businesses are moving to the Internet: As more customers prefer e-commerce to in-store shopping, I believe consumer demand will shift away from third-party retailers and toward electronics brands.

- Best Buy must compete on price: To put it more bluntly, if Best Buy wants to compete directly with brands, it will have to do so on price. The company has found that consumers are increasingly looking for deals. Price competition will come at the expense of Best Buy’s margin, which is already shrinking.

- The replacement cycles are extended: The company has also found that customers are keeping their devices longer, partly due to the weaker economic environment, which is impacting sales.

All in all, despite Best Buy’s dividend and the currently low 13.5x P/E (based on the Wall Street consensus of $6.10 pro forma EPS this year) I still want to avoid that name.

Weak comparable sales: Is it wise to bet on a turnaround?

First, investors need to keep in mind that comparable sales (also called same-store sales), which measure sales growth without taking into account store openings and closings during the same period, continue to decline by a high single-digit percentage.

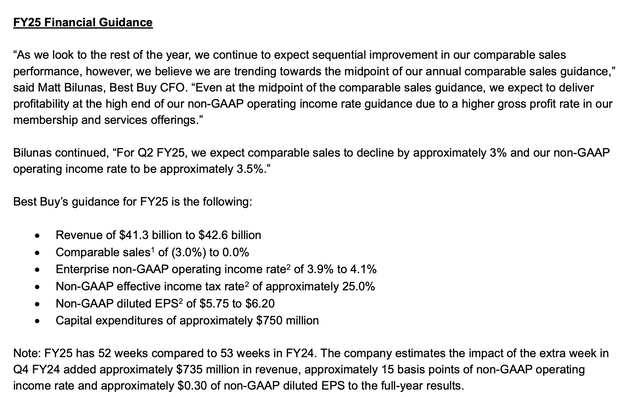

And yet the company’s outlook for fiscal 2025 (Best Buy’s fiscal year ends in January 2025), and thus consensus hopes for Best Buy, are based on comparable sales Improvement.

Best Buy Fiscal Year 2025 Outlook (Best Buy Q1 Earnings Release)

The company’s FY25 outlook is shown above. To achieve pro forma earnings per share of $5.75-$6.20 (note that the consensus of $6.10 is currently at the high end of that range), the company is relying on reducing the decline in existing store sales to -3% or flat year-on-year.

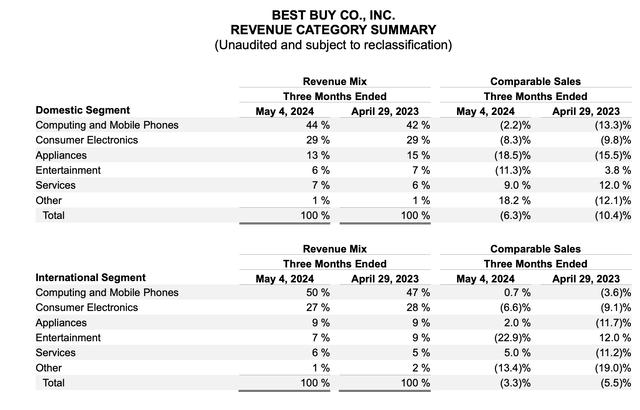

And yet, Best Buy’s comparable sales fell 6.1% last quarter. The international segment fared slightly better, with a 3.3% decline (though it should be noted that the international segment still represents less than 10% of the company’s total revenue), while the domestic segment’s comparable sales fell 6.3% year over year.

Best Buy Comparable Sales by Category (Best Buy Q1 Earnings Release)

There is no bright spot in Best Buy’s major categories. While comparable sales are higher in services (e.g. support services like Geek Squad), that is a very small percentage of total sales. In contrast, the home appliances and entertainment categories are seeing massive year-over-year declines.

The company relies on both a friendlier environment for consumer spending as well as increased demand from the introduction of AI products will help comparable sales return to growth. According to CEO Corie Barry’s remarks on the first quarter conference call:

From a major category perspective, we continue to expect sales in our computer category to grow for the full year. We expect sales to decline overall for the remaining product categories, partially offset by growth in our services revenue. As we plan for the next three quarters, we expect our comparable sales to improve sequentially. Specifically, for the second quarter, we expect comparable sales to decline approximately 3% compared to the 6% decline we experienced in the first quarter. Based on current month sales and results, our estimated comparable sales for May are expected to be better than our second quarter guidance. These results are encouraging, but from a timing perspective, we do not surpass last year’s Memorial Day sales until our first week of business in June, and we continue to be very careful with the periods between sales events.

Let’s talk about computers and the exciting things happening there. We expect the category to benefit as early replacement and upgrade cycles gain momentum and new products with even more AI capabilities come to market throughout the year. We’ve seen early signs of improvement as comparable sales for laptops were slightly positive year over year in Q4 and that trend continued in Q1. Last week, Microsoft announced that Copilot Plus and laptops from Microsoft, Dell, HP, Lenovo and Samsung are now available for pre-order on our website and will be available starting June 18. These devices are faster, have better battery life, are more efficient, they run much cooler and have basic Copilot features like summaries that help quickly summarize pages of documents or long email threads.”

Of course, it’s no safe bet to bet on a growth acceleration that hasn’t yet happened. We don’t have any concrete results to show that Microsoft’s Copilot Plus announcements or Apple’s Apple Intelligence announcement at WWDC will cause a slowdown in the refresh cycle at Best Buy and other retailers.

Dividend risks

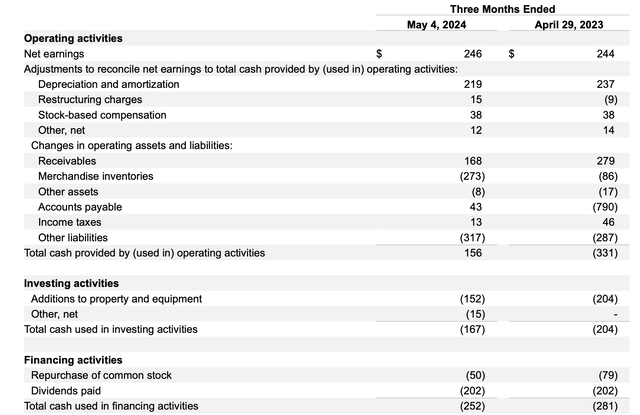

In the meantime: Best Buy is spending money on dividends and stock buybacks like a company that generates way more revenue than it actually does. Take a look at its first-quarter cash flow statement below:

Best Buy FCF (Best Buy Q1 Earnings Release)

Operating cash flow in the first quarter was only $156 million, and after deducting $152 million for capital expenditures, FCF was almost zero. At the same time Best Buy spent $252 million on dividends ($202 million, $0.94 per share per quarter) and buybacks ($50 million).

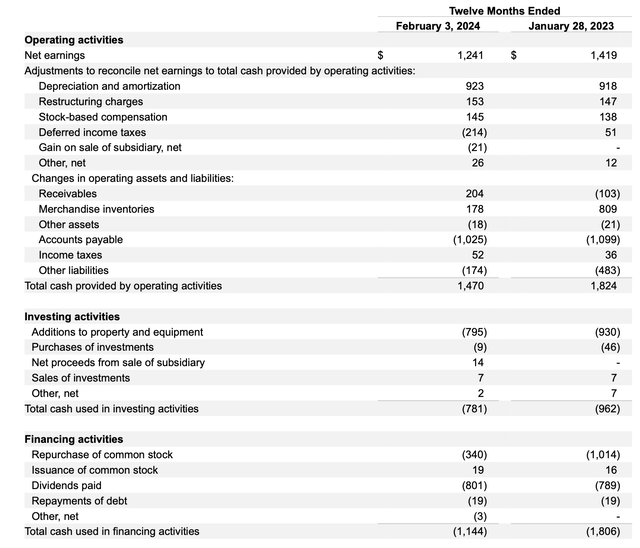

This isn’t just a seasonal cash flow issue either, as we know that Q1 tends to be a weaker sales quarter for Best Buy. The same problem existed throughout fiscal 2023 as well. As shown below, Best Buy generated $1.47 billion in operating cash flow in fiscal 2023, but only $675 million in FCF after capital expenditures:

Best Buy FY23 FCF (Best Buy Q4 Earnings Release)

Meanwhile, the company spent $801 million on dividends and $340 million on share buybacks, for a total return on capital of $1.14 billion.

The central theses

In other words, don’t make the mistake of thinking that Best Buy’s dividend is anywhere near safe. The company is currently in a roughly neutral cash position ($1.21 billion in cash and $1.15 billion in debt, or $60 million in net cash). could increase its debt to further fund its dividend hole. But a bet on Best Buy is essentially a bet that the consumer electronics sector will experience a wave of new purchases inspired by new AI features, and that is far from guaranteed. I’m staying on the sidelines here.

shares?")

Should value investors buy HCA Healthcare (HCA) shares?

Travis Kelce announces “even more memories” with Taylor Swift after making surprise appearance on Eras tour in London