Eugene Technology Ltd and two other KRX stocks are below estimated value

Last year, the South Korean market recorded a modest growth of 5.0%, and expectations for annual earnings growth in the near term are an impressive 30%. In such an environment, identifying stocks trading below their estimated value could provide investors with potential growth opportunities.

The 10 most undervalued stocks in South Korea based on cash flows

|

Surname |

Current price |

Fair value (estimated) |

Discount (estimated) |

|

Caregen (KOSDAQ:A214370) |

₩22450.00 |

44549,16 € |

49.6% |

|

Anapass (KOSDAQ:A123860) |

₩25250.00 |

48541,20 € |

48% |

|

KidariStudio (KOSE:A020120) |

4080,00 € |

7404,33 € |

44.9% |

|

Tax free worldwide (KOSDAQ:A204620) |

3565,00 € |

6215,37 € |

42.6% |

|

Revu (KOSDAQ:A443250) |

₩10990.00 |

20,987.95 € |

47.6% |

|

Lutronic (KOSDAQ:A085370) |

36700,00 € |

63217,94 € |

41.9% |

|

SK Biopharmaceuticals (KOSE:A326030) |

77500,00 € |

149,728.31 € |

48.2% |

|

Genomictree (KOSDAQ:A228760) |

23,400.00 € |

39,870.28 € |

41.3% |

|

Beam (KOSDAQ:A228670) |

12010,00 € |

20,596.36 € |

41.7% |

|

NEXON Games (KOSDAQ:A225570) |

17900,00 € |

28212,32 € |

36.6% |

Click here to see the full list of 37 stocks from our Undervalued KRX Stocks Based on Cash Flows screener.

Here’s a look at some of the choices from the screener

Overview: Eugene Technology Co., Ltd. specializes in the manufacture and sale of semiconductor equipment and parts. The company operates both in South Korea and internationally and has a market capitalization of approximately ₩1.06 trillion.

Operations: The company generates its revenue primarily from two segments: semiconductor equipment, which generates ₩257.39 billion, and industrial gas for semiconductors, which contributes ₩10.01 billion.

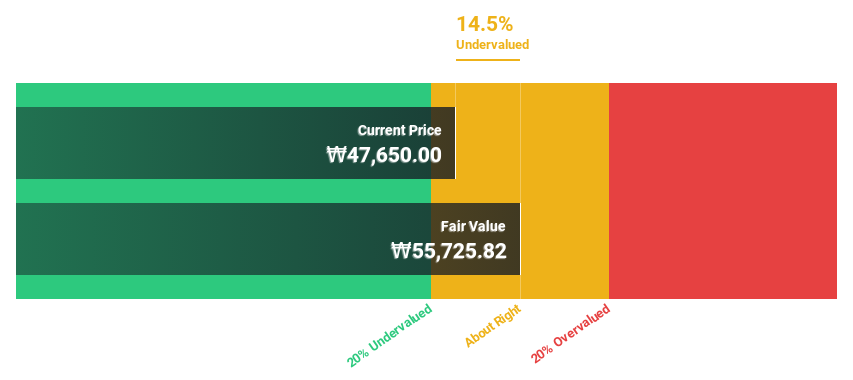

Estimated discount to fair value: 14.5%

Eugene Technology Ltd. currently trades at ₩47,650, below our fair value estimate of ₩55,725.82. Despite a recent decline in net income and earnings per share as reported in its first quarter 2024 results, the company is poised for robust growth, with revenue and earnings expected to grow 21% and 47.7% annually, respectively. However, return on equity is expected to remain low at 16.5%, and the stock has faced high volatility over the past three months.

Overview: ISU Petasys Co., Ltd. is a global printed circuit board (PCB) manufacturer with a market capitalization of approximately ₩3.64 billion.

Operations: The focus of the company’s business activities is on the worldwide production and distribution of printed circuit boards.

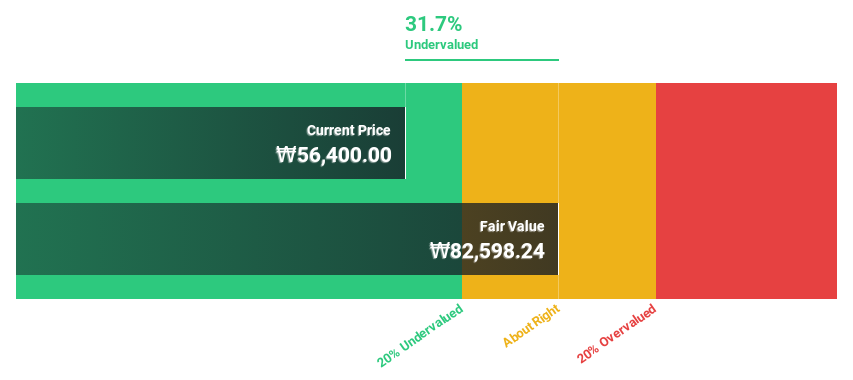

Estimated discount to fair value: 35%

ISU Petasys is significantly undervalued at ₩57,400 versus our fair value estimate of ₩90,930.23. The company’s revenue and earnings are expected to grow 16.2% and 41.5% annually, respectively, outperforming the South Korean market average. Despite this growth potential, there are concerns about high share price volatility and insufficient debt coverage by operating cash flow. In addition, profit margins have declined to 7% from 15.1% last year.

Overview: Cosmax, Inc. is a company engaged in the research, development, production and manufacturing of cosmetics and health foods both in Korea and worldwide and has a market capitalization of approximately ₩2.03 trillion.

Operations: The company operates in the areas of cosmetics and health-promoting functional foods and generates its sales internationally.

Estimated discount to fair value: 28.2%

Cosmax, with a current price of ₩179,000, is below our fair value estimate of ₩250,409.13, suggesting that the company is undervalued. Its earnings have increased by 467.9% over the past year and are expected to grow at a rate of 26.74% annually. Despite the robust revenue growth forecast of 13.1% per year – which beats the Korean market average – the company’s earnings growth lags behind the market rate of 29.6%. In addition, high levels of debt could pose financial risks in the future.

Make it happen

Would you like to explore some alternatives?

This Simply Wall St article is of a general nature. We provide commentary based solely on historical data and analyst forecasts, using an unbiased methodology. Our articles are not intended as financial advice. They do not constitute a recommendation to buy or sell stocks, and do not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Companies discussed in this article include KOSDAQ:A084370, KOSE:A007660 and KOSE:A192820.

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]

Who is Renato Veiga? Statistics, transfer value, positions

Former singer of “Lostprophets” stabbed to death over drug debts