Western Digital: Flash offshoots unlock new values (NASDAQ:WDC)

")

Photo by JHVE

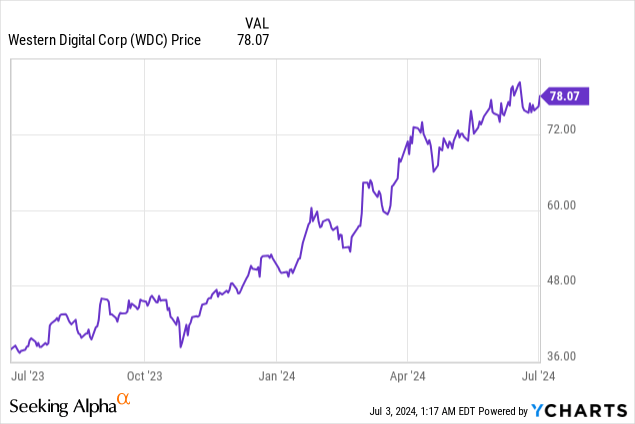

Suddenly, chip stocks are rising again out of sympathy with NVIDIA Corporation (NVDA). Western Digital Corporation (NASDAQ: WDC), a manufacturer of hard drives and NAND flash technology, has risen by over 50% since the beginning of the year after a multi-year slump and has Western Digital is just one notch above its 2021 highs.

Hopeful investors are betting on a number of things for Western Digital: a higher valuation on the back of an impending spin-off of Western Digital into two companies, long-term tailwinds in generative AI that are increasing storage demand, and continued high NAND flash prices to maintain Western Digital’s margins.

I last wrote a bearish article on Western Digital in early 2021, when the stock hit a multi-year high. Now, amid new industry dynamics and a strong growth revival, I am changing my rating on Western Digital to a Buy recommendation, before the planned spin-offs.

We must acknowledge that there are risks and contingencies that make a sustainable rally possible for Western Digital (which we will discuss later in this article), but overall, I expect several catalysts to continue to boost Western Digital, especially if one or both of Western Digital’s businesses reinstate the company’s dividend payment after the spin-off (Western Digital paid a quarterly dividend payment of $0.50 to storage markets that collapsed in 2020).

Hot storage market

The first factor to highlight: the storage market is currently heating up. We can attribute most of the upside to long-term tailwinds from demand for generative AI. As most investors know, AI requires massive amounts of data on which generative models answer queries and generate answers. This, in turn, has driven demand for cheap, fast storage. While this is certainly commoditized, Western Digital (along with rival Micron Technology, Inc. (MU)) has long been one of the leading suppliers of storage hardware and thus stands to benefit tremendously from increased prices, especially for NAND flash memory.

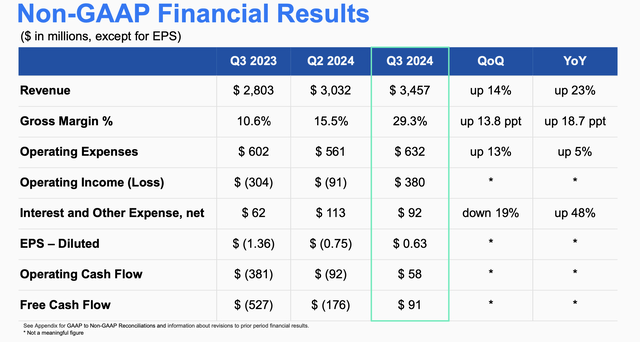

In Western Digital’s last quarter, the third quarter (March quarter), revenue increased 23% year-on-year to $3.46 billion, beating Wall Street’s expectations of $3.35 billion (+20% year-on-year). Gross margins also increased 19 points compared to last year This is due to favorable NAND flash pricing, which resulted in a 29.3% increase, which in turn led to significant operating income, earnings per share and free cash flow – in contrast to the sharp losses last year.

Western Digital Q1 Highlights (Western Digital Q1 Shareholder Presentation)

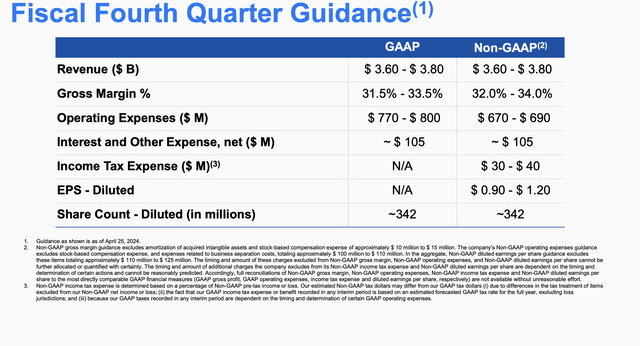

The company expects this trend to continue well into the fourth quarter, forecasting revenue of $3.60 billion to $3.80 billion, representing year-over-year growth of 40% on a mid-year basis, and gross margins improving three to five percentage points sequentially to a range of 32-34%.

Western Digital Q4 Outlook (Western Digital Q1 Shareholder Presentation)

Spinoff takes advantage of favorable market position

It is important to recognize that Western Digital’s recent success is due to the lightning Although the HDD (hard disk) segment also recorded growth.

Western Digital Segment Results (Western Digital Q1 Shareholder Presentation)

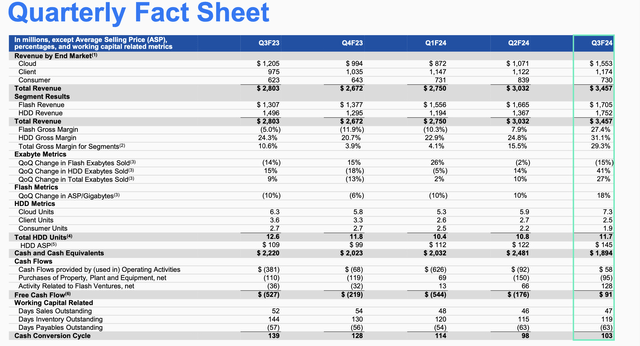

The chart above breaks down the Flash and HDD segments. Flash revenue grew 30% year-over-year, while HDD revenue grew at a slower 17%.

But importantly, it is NAND prices that drives revenue growth. Actual exabyte shipments for flash actually declined -15% in Q3 versus Q2, but this was more than offset by an 18% quarter-over-quarter price increase (leading to a 2% quarter-over-quarter increase in flash revenue).

NAND has always been a highly cyclical industry, which is why Western Digital and many of its competitors typically trade at a P/E ratio below that of the broader market indices.

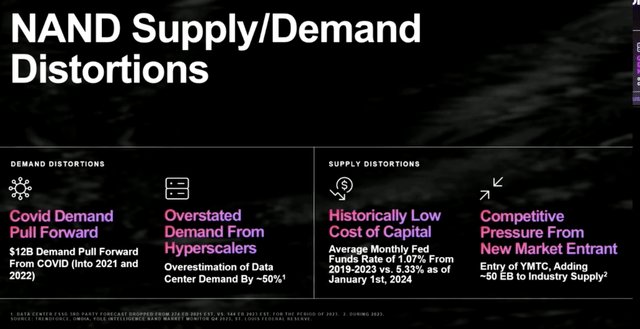

In a recent investor presentation in June on NAND industry dynamics and the company’s decision to spin off the NAND flash segment into a separate company, Western Digital’s flash segment executives emphasized that the NAND industry is suffering from a poor 2022-2023 fiscal year for several reasons.

NAND Market Dynamics (Western Digital’s New Era of NAND Shareholder Presentation)

The COVID era pulled demand into 2021 (the stock’s previous high) and early 2022, which was particularly boosted by cloud hyperscalers (think Meta Platforms, Inc. (META)) investing heavily in data centers at the time in anticipation of higher traffic. Combined with lower COVID-era capital costs at lower interest rates, Western Digital and its competitors engaged in an investment race to maintain market share, resulting in lower NAND prices and oversupply.

Now, however, the company believes it is exiting that dynamic. The oversupply in the market is naturally dissolving while new AI-driven demand is driving up flash prices. In the “New Era of NAND” investor presentation, the company’s Flash segment EVP stated that he believes the industry is heading toward a phase where demand relative to fully utilized supply capacity is over 100%, which is a driver for further NAND flash price increases.

This is the rationale behind Western Digital’s plan to split its flash division into a separate company, first announced in October 2023. As a reminder, the company currently operates its flash segment as a joint venture with a Japanese company called Kioxia (with 50.1% ownership), which in turn is backed by another memory industry rival, SK Hynix. The companies are jointly responsible for flash innovation, but Kioxia takes on a larger share of the manufacturing burden and is responsible for wafer building.

Valuation should be released through spin-off, but risks should be kept in mind

Large corporate spin-offs are rare, especially in the technology sector (the most recent major that springs to mind is HP, which split into software company Hewlett Packard Enterprise Company (HPE) and printer and PC maker HP Inc. (HPQ).) The motivation is almost always to increase valuation multiples for a higher-value segment: in Western Digital’s case, that’s the flash segment, which it believes can return to premium margins.

As a merged company, Western Digital is currently being valued at a low 9.8x P/E compared to consensus estimates of $8.01 pro forma earnings per share for the next fiscal year FY25 (the year ending June 2025 for Western Digital).

In my opinion, the spin-off has the potential to bring higher multiples to the Flash unit, increasing the overall value for investors. However, there are a few risks we need to keep in mind:

- The cyclical fluctuations in the storage industry are a reality of business. Western Digital is wisely spinning off its flash business at what it believes is an opportune time, but periods of oversupply and weak demand have always been a feature of the storage industry.

- The current growth drivers could have a very short end. What happened at the beginning of the COVID era, when hyperscalers pulled back on data center investments, only to see demand slow in 2022-2023, may well apply to the current AI-driven era.

- debt burden. Western Digital is still heavily indebted. The consolidated company currently has debt of $5.0 billion, bringing its leverage to nearly three times its assets.

The central theses

Despite the risks, I think Western Digital is an attractive short- to medium-term investment. Once the details of the spin-off are finalized, I believe there is an opportunity for investors to capture value in this stock beyond its current P/E of less than 10, particularly as the company continues to expect sequential improvement in NAND industry momentum and expects improved growth and higher margins in the fourth quarter.

Use short-term price declines as a buying opportunity.

Facts about Paul Young: Singer’s age, wife, kids, songs and career explained

NCIS star explains how David McCallum’s death changed the series