Comet Holding leads the value stock trio on the SIX Swiss Exchange

Swiss stocks experienced a downturn on Tuesday, overshadowed by broader European market trends and concerns about potential interest rate changes from the Federal Reserve and European Central Bank. In this cautious market environment, identifying undervalued stocks like Comet Holding can offer investors potential value opportunities.

The 10 most undervalued stocks in Switzerland based on cash flows

|

Surname |

Current price |

Fair value (estimated) |

Discount (estimated) |

|

COLTENE Holding (SWX:CLTN) |

CHF 46.50 |

76,58 CHF |

39.3% |

|

Burckhardt Compression Holding (SWX:BCHN) |

CHF 599.00 |

CHF 849.08 |

29.5% |

|

Julius Baer Group (SWX:BAER) |

CHF 51.18 |

CHF 96.31 |

46.9% |

|

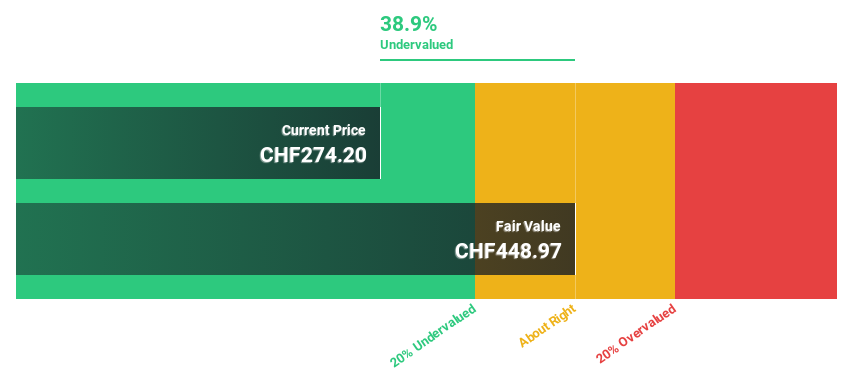

Sonova Holding (SWX:SOON) |

CHF 279.20 |

CHF 463.92 |

39.8% |

|

Temenos (SWX:TEMN) |

62,65 CHF |

85,86 CHF |

27% |

|

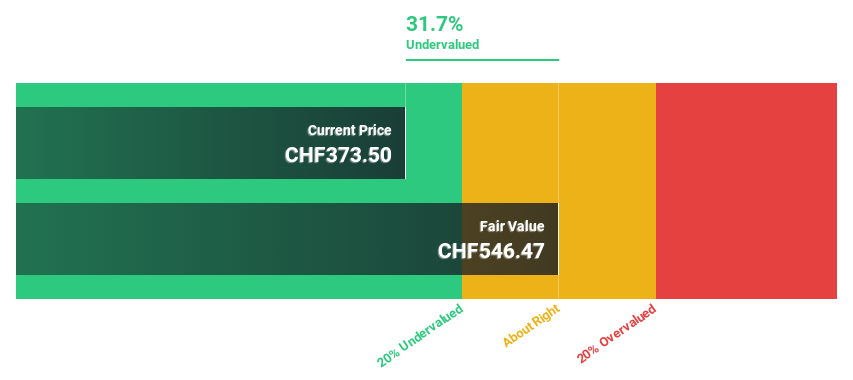

Comet Holding (SWX:COTN) |

CHF 357.00 |

CHF 581.31 |

38.6% |

|

SGS (SWX:SGSN) |

CHF 79.60 |

125,39 CHF |

36.5% |

|

Medartis Holding (SWX:MED) |

CHF 69.00 |

129,75 CHF |

46.8% |

|

Kudelski (SWX:KUD) |

1,40 CHF |

1,88 CHF |

25.5% |

|

Sika (SWX:SIKA) |

CHF 255.30 |

CHF 329.12 |

22.4% |

Click here to see the full list of 13 stocks from our Undervalued SIX Swiss Exchange Stocks Based on Cash Flows screener.

Let’s examine some outstanding options from the results in the screener

Overview: Comet Holding AG operates worldwide and offers solutions in the field of X-ray and radiofrequency technology in Europe, North America, Asia and other regions with a market capitalization of CHF 2.79 billion.

Operations: Comet Holding’s sales are generated in three main segments: X-Ray Systems (IXS) with CHF 116.96 million, Industrial X-Ray Modules (IXM) with CHF 100.26 million and Plasma Control Technologies (PCT) with CHF 193.16 million.

Estimated discount to fair value: 38.6%

Comet Holding is significantly undervalued at a price of CHF 357 based on a discounted cash flow analysis with an estimated fair value of CHF 581.31. Despite a decline in profit margin from 13.3% last year to 3.9%, Comet’s profit is expected to grow by 43.14% annually over the next three years, significantly outperforming the Swiss market growth rate. The stock remains highly volatile, reflecting its current trading status at 38.6% below fair value and the potential for significant appreciation.

Overview: Sonova Holding AG is a company specializing in the manufacture and distribution of hearing solutions for adults and children in regions such as the USA, Europe, the Middle East, Africa and the Asia-Pacific region with a market capitalization of CHF 16.71 billion.

Operations: Sonova generates its sales primarily in the hearing aid segment, which generated 3.36 billion francs, and in the cochlear implants segment, with sales of 282.40 million francs.

Estimated discount to fair value: 39.8%

Sonova Holding appears to be undervalued by DCF standards with a current share price of CHF 279.20, suggesting a fair value of CHF 463.92. Despite high debt, Sonova’s robust forecast sales growth of 7.1% annually outperform the Swiss market at 4.4%, coupled with earnings growth forecast of 9.9% per year – higher than the market average of 8.4%. In addition, return on equity is expected to be strong at 26.2% in three years, suggesting potential for improving financial performance despite not achieving very high growth rates.

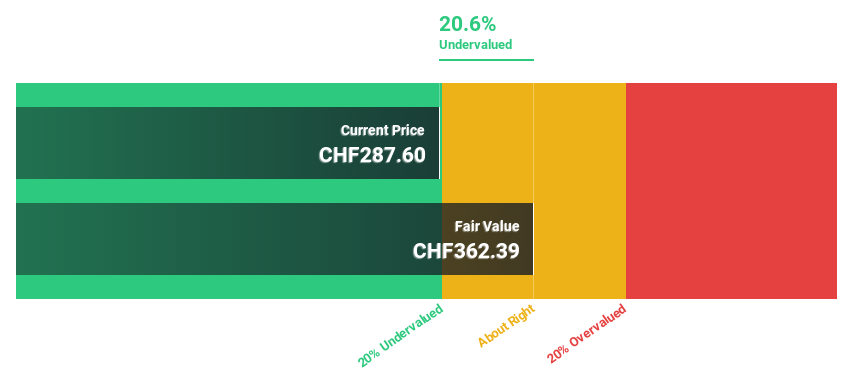

Overview: Swissquote Group Holding Ltd operates worldwide and offers a range of online financial services to retail, high net worth individuals and professional institutional clients with a market capitalization of CHF 4.24 billion.

Operations: The company generates its revenue mainly from two segments: Leveraged Forex, which generated CHF 101.09 million, and Securities Trading, which contributed CHF 429.78 million.

Estimated discount to fair value: 20.6%

Swissquote Group Holding is trading at CHF 288.2 below its estimated fair value of CHF 363.11, reflecting a possible undervaluation based on DCF analysis. While earnings growth is not exceptional, it will outperform the Swiss market with a forecast annual increase of 14%. In addition, the company’s revenue growth forecast of 10.3% annually also exceeds the market expectation of 4.4%. In addition, Swissquote’s return on equity is expected to be a solid 23.1% in three years.

Turning ideas into action

Looking for other investments?

This Simply Wall St article is of a general nature. We comment based solely on historical data and analyst forecasts, using an unbiased methodology. Our articles are not intended as financial advice. They do not constitute a recommendation to buy or sell stocks and do not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Companies discussed in this article include SWX:COTN SWX:SQN and

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]

NJ Transit drivers on the verge of a strike

Taylor Swift said in an old interview that Mary’s song was about eternal love

:max_bytes(150000):strip_icc():focal(1026x548:1028x550)/Shannen-Doherty-Chris-Cortazzo-071424-2-4591beb5b41346d2b1c3072cff99dcdd.jpg "Shannen Doherty spent time with her boyfriend Chris Cortazzo in her last public photo before her death")