Calculating the intrinsic value of AppFolio, Inc. (NASDAQ:APPF)

")

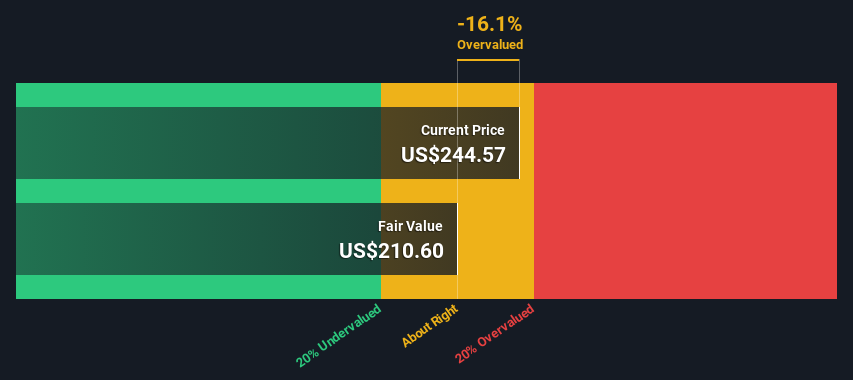

Key findings

-

AppFolio’s estimated fair value is $211 based on 2-step free cash flow to equity

-

With a share price of $245, AppFolio appears to be trading close to its estimated fair value

-

The analyst price target of $267 for APPF is 27% above our fair value estimate

How far is AppFolio, Inc. (NASDAQ:APPF) from its intrinsic value? Using the most recent financial data, we will check whether the stock is fairly valued by estimating the company’s future cash flows and discounting them to their current value. Our analysis will use the Discounted Cash Flow (DCF) model. Don’t be put off by the technical jargon, the math behind it is actually quite simple.

However, keep in mind that there are many ways to estimate the value of a company, and a DCF is just one method. If you still have pressing questions about this type of valuation, take a look at Simply Wall St’s analysis model.

Check out our latest analysis for AppFolio

The method

We use a two-stage DCF model which, as the name suggests, considers two phases of growth. The first stage is generally a higher growth phase that stabilizes toward the terminal value captured in the second “steady growth” stage. First, we need to estimate the next ten years of cash flows. Where possible, we use analyst estimates, but when these aren’t available, we extrapolate previous free cash flow (FCF) from the last estimate or reported value. We assume that companies with shrinking free cash flow will slow their rate of shrinkage, and that companies with growing free cash flow will slow their growth rate over this period. We do this to take into account that growth tends to slow more in the early years than in later years.

A DCF is all about the idea that a dollar in the future is worth less than a dollar today. Therefore, we need to discount the sum of these future cash flows to arrive at an estimate of present value:

Estimation of free cash flow (FCF) over 10 years

|

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

2032 |

2033 |

|

|

Leveraged FCF (in million US dollars) |

172.4 million US dollars |

209.7 million US dollars |

265.7 million US dollars |

USD 308.0 million |

344.4 million US dollars |

375.5 million US dollars |

401.8 million US dollars |

424.4 million US dollars |

444.2 million US dollars |

461.8 million US dollars |

|

Source of growth rate estimate |

Analyst x5 |

Analyst x5 |

Analyst x1 |

Estimated at 15.91% |

Estimated at 11.85% |

Estimated at 9.01% |

Estimated at 7.02% |

Estimated at 5.63% |

Estimated at 4.65% |

Estimated at 3.97% |

|

Present value (in million US dollars) discounted at 6.9% |

161 US dollars |

183 US dollars |

217 US dollars |

236 US dollars |

247 US dollars |

251 US dollars |

252 US dollars |

249 US dollars |

243 US dollars |

237 US dollars |

(“Est” = FCF growth rate, estimated by Simply Wall St)

Present value of 10-year cash flow (PVCF) = 2.3 billion US dollars

We now need to calculate the terminal value that takes into account all future cash flows after this ten-year period. The Gordon growth formula is used to calculate the terminal value at a future annual growth rate equal to the 5-year average of the 10-year Treasury yield of 2.4%. We discount the terminal cash flows to today’s value at a cost of equity of 6.9%.

Final value (TV)= FCF2033 × (1 + g) ÷ (r – g) = 462 million US dollars × (1 + 2.4%) ÷ (6.9% – 2.4%) = 10 billion US dollars

Present value of terminal value (PVTV)= TV / (1 + r)10= 10 billion US dollars ÷ (1 + 6.9%)10= 5.4 billion US dollars

The total value is calculated by adding the next ten years’ cash flows plus the discounted terminal value, which gives the total equity value, which in this case is $7.6 billion. In the final step, we divide the equity value by the number of shares outstanding. Relative to the current share price of $245, the company seems about fair at the time of writing. The assumptions in each calculation have a big impact on the valuation, so it’s better to consider this a rough estimate that isn’t accurate to the last cent.

Important assumptions

The above calculation relies heavily on two assumptions. The first is the discount rate and the other is the cash flows. You don’t have to agree with these inputs, I recommend repeating the calculations yourself and playing with them. The DCF also doesn’t take into account the possible cyclicality of an industry or a company’s future capital needs and therefore doesn’t provide a complete picture of a company’s potential performance. Since we consider AppFolio as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or weighted average cost of capital, WACC) which takes debt into account. In this calculation, we used 6.9%, which is based on a leveraged beta of 0.985. Beta is a measure of a stock’s volatility relative to the overall market. We get our beta from the industry average beta of globally comparable companies with an imposed limit of between 0.8 and 2.0, which is a reasonable range for a stable company.

SWOT Analysis for AppFolio

Strength

weakness

Opportunity

Danger

Looking ahead:

Valuation is only one side of the coin when building your investment thesis and ideally shouldn’t be the only analysis you review for a company. The DCF model is not a perfect tool for stock valuation. Instead, a DCF model is best used to test certain assumptions and theories to see if they would lead to an undervaluation or overvaluation of the company. For example, making a small adjustment to the terminal value growth rate can dramatically change the overall result. For AppFolio, we’ve compiled three additional points to review:

-

Risks: We think you should 2 warning signs for AppFolio We indicated this before investing in the company.

-

management:Have insiders increased their shares to capitalize on market sentiment regarding APPF’s future prospects? Read our management and board analysis with insights into CEO compensation and governance factors.

-

Other high-quality alternatives: Like a good all-rounder? Explore our interactive list of high-quality stocks to get a sense of what else you might be missing out on!

PS The Simply Wall St app runs a discounted cash flow valuation for every stock on the NASDAQGM every day. If you want to find the calculation for other stocks, just search here.

Do you have feedback on this article? Are you concerned about the content? Get in touch directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]

Celebrate the 4th of July at Jimmy’s Famous and secure your spot for the Big Bay Boom fireworks

Official media report that an army officer was killed in an Israeli attack on Syria