Nathan is Famous: Famous for a Reason (NASDAQ:NATH)

")

OkiMdp

thesis

Nathan’s famous (NASDAQ:NATH) is significantly underestimated and undervalued, offering investors the opportunity to invest in a leading premium hot dog brand with significant upside potential (over 50% from recent prices) and limited downside potential. Nathan’s can be considered a Hot Dogs due to consumer preferences and operates an asset-light business model that enables robust free cash flow generation. In addition, Nathan’s is an excellent acquisition candidate with acquisition multiples suggesting triple-digit upside potential.

overview

Nathan’s has its roots in a hot dog stand in Coney Island in 1916. The recipe for the spice blend they use was developed by Ida Handwerker, Nathan’s wife. The brand has grown outside of New York over time, while the franchise traces its humble beginnings each year with the annual hot dog eating contest on ESPN.. Although the concept of hot dogs is quite simple, Nathan’s has fallen into stock market obscurity for several reasons. First, there is no coverage of the security on Wall Street, making it difficult to analyze. Second, the company does not conduct conference calls, which are a regular occurrence at most publicly traded companies. Third, this simple hot dog company operates in three different segments, each with unique opportunities, challenges, and margin profiles and growth rates.

Business areas

Below, I’ll cover each segment of Nathan’s. Note that percentage of revenue and year-over-year growth are based on FactSet data and are as of March 2024.

Restaurants: 12.1% of sales; 0.0% growth

- Thoughts:

- Restaurants have increasingly become a small part of the overall pie as licensing and branded product programs grow faster. I expect this to continue. Competition is too fierce to justify the expansion of company-owned stores.

- Margins:

- Company-owned stores generate low single-digit margins (including all company-owned operating costs). Franchise fees and royalties account for virtually 100% of the margin. Taken together, restaurants generate a low single-digit margin.

- Competitors:

- The competition is varied and numerous. In the quick service restaurant space, NATH competes with companies such as McDonald’s, Burger King, Hardee’s/Carl’s Jr. and others.

Branded product range: 63.3% of sales; 9.6% growth

- Thoughts:

- The Branded Product Program has grown rapidly since the pandemic and is the largest segment overall. Given NATH’s unique taste and fries and hot dog portfolio, I believe this will continue to be the fastest growing and biggest opportunity for NATH. Locals are trying to justify higher prices in an inflationary world and NATH’s unique taste helps them do that.

- Margins:

- Low double-digit gross margins (around 13% to less than 20% on average), currently on the lower end due to beef price inflation.

- Competitors:

- Competitors include other hot dog vendors, including Ball Park and Sahlen’s.

Licensing: 24.6% of sales; 0.4% growth

- Thoughts:

- Consumers are increasingly eating at home as out-of-home food prices have soared due to wage increases. NATH’s continued expansion into stores across the country should support growth. Prices will lag behind peak beef prices, but that’s OK because NATH isn’t bearing the costs.

- Margins:

- Practically 100%.

- Competitors:

- Licensed products are frozen foods available in local grocery and convenience stores. Major competitors include Ball Park, Oscar Mayer and Ore-Ida (French fries).

Brand and taste dominance

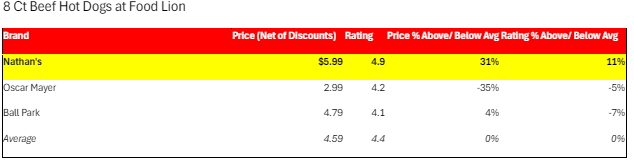

Warren Buffett talks a lot about market share. While brands like Oscar Mayer have a strong market share, their hot dogs are of lower quality and do not have the distinct taste and brand recognition of Nathan’s. Nathan’s has a larger market share. The hot dog eating contest gives over 2 million viewers annually significant exposure to the Nathan’s brand, something the competition cannot match. Additionally, Nathan’s is widely praised. Consumer Reports and Bon Appétit have both named Nathan’s Skinless Beef Franks as their top hot dog choice. Don’t just take their word for it! The table below summarizes data from the Food Lion website on 8-packs of hot dogs (data retrieved in late April). Note that Nathan’s charges a premium and receives ratings that are well above the brands with the largest market share in hot dogs.

Food Lion

Consolidation

The hot dog industry in the United States is concentrated. According to MRI-Simmons data, the top 5 brands (Nathan’s is number 5) accounted for nearly 60% of the brands most consumed by consumers. All of the top 5 brands except NATH are owned by large companies. Oscar Mayer is owned by Kraft Heinz (KHC). Hebrew National is owned by Conagra (CAG). Bar S is part of Sigma Alimentos, which in turn is owned by Alfa SAB de CV. The most recent transaction in the hot dog space in the United States was the acquisition of Hillshire by Tyson Foods (TSN), which owns the Ball Park brand. The acquisition occurred in 2014 at over 16x EV-to-EBITDA (over 60% above NATH’s TTM multiple). In the larger snack space, JM Smucker acquired Hostess in 2023 for 17.2x EV-to-EBITDA (again, well above NATH’s multiple). Insiders own 25% of NATH and Executive Chairman Howard Lorber owns about 3/4 of that. Lorber has had a major influence on Nathan’s development over the years as both a private and public company, taking the company from a restaurant company to a licensing giant. Given that Lorber is 75 years old, one has to wonder what happens to his shares when he dies. While CEO Eric Gatoff is a strong and capable manager for a standalone NATH, I see a larger company going after Nathan’s as the company has a strong cash flow profile and incredible brand recognition in a relatively commoditized space. One of the suitors would likely be Smithfield as the company already works with Nathan’s through its licensing partnership. However, Nathan’s is a good acquisition candidate overall because it has a low multiple (<10x EV-to-EBITDA), above-comparable revenue growth (4.9% over 10 years), and above-comparable profitability (15% 5-year average net profit margin).

Evaluation

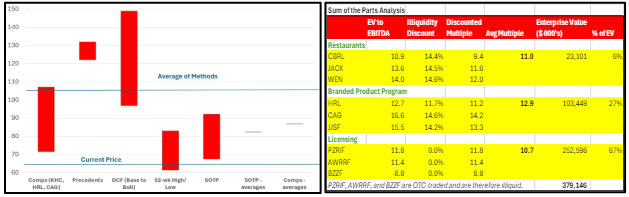

I performed DCF analysis for bull and base case scenarios and valued based on comparable companies (Hormel, ConAgra and Kraft Heinz). I split NATH into the three segments and performed a sum-of-the-parts analysis (see right). I will explain these methods further.

For the DCF base case, I assumed revenue growth of 3.0% in 2025, followed by a 0.5% decline through 2029 (after which growth is 0.0%). This assumes that margins do not recover from the losses they suffered during inflation, but actually decline to 33.6% (gross) as the branded product program becomes a larger portion of revenue. Operating expenses increase over time to 11.4% of revenue (10.8% in 2023). I use a WACC of 8% and a terminal growth rate of -2%. In addition, I assume no change in shares outstanding. This comes to $96.80 per share.

For the bull case DCF, I assume the same revenue growth pattern as the base case; however, gross margins recover significantly by 2030 (from 34.2% in 2024 to 35.8%). Operating expenses follow the same path as the base case. The WACC I used is 6% and the terminal growth rate is 1%. Again, no changes were made to shares outstanding. That works out to $147.36 per share for me.

For the previous transactions, I simply applied 16x (conservative estimate since Hillshire was acquired for more than that amount) and 17.4x EV to EBITDA (the multiple at which Hostess was acquired) to NATH’s EBITDA.

For the Sum of the Parts (SOTP), I used the following tickers in the right table below and applied the corresponding average multiples of the three tickers under each segment to the respective segment. To get the lower bound of the range, I did the same and just used the lowest peer multiple per segment. For the corporate expenses, I applied them to each segment based on the segment’s contribution to gross profit.

For comps, I simply applied the multipliers of HRL, CAG and KHC to NATH. Please note that I applied an illiquidity discount to both comps and SOTP. The illiquidity discount for comps and SOTP was based on bid-ask spreads.

Based on averages of DCF, SOTP, precedents (Hillshire and Hostess) and comparables, I came up with $105, which represents over 50% upside. Note that very negative growth and high WACC assumptions are needed in the DCF to get to a price below today’s price. Using the same assumptions as the base case except that margins drop to 32.3% by 2030, and using a 9% WACC and a -3% growth rate, I came up with $64.23 (less than 8% downside).

Author’s own work

Risks

Beef Prices In its third-quarter earnings release on Feb. 1, Nathan’s cited beef prices as the primary reason for margin erosion. While average selling prices in the Branded Product Program rose 8% for the 39 weeks ended December, beef and beef cuts saw a 12% increase over the same period. Although Nathan’s offers a premium hot dog, as seen in the Food Lion chart, Nathan’s price increases tend to lag behind inflation spikes. Conversely, when beef prices fall, average selling prices remain stable. Price increases should strengthen licensing as long as volumes are not impacted. The bullish scenario DCF assumes margins normalizing, while the baseline DCF assumes continued pressure to be conservative.

Work

Nathan’s is in the restaurant business and wage pressures are increasing, particularly in New York where the company’s restaurants are operated. These pressures can also be felt by franchisees and reduce franchise profitability. Nathan’s gets 4.5% of its sales from franchisees, so the impact on profits is not directly felt. However, if franchisees are struggling, it can affect the number of openings/closings.

Illiquidity

Average daily trading volume is about $250,000 worth of shares. It can be difficult to enter and exit the position without changing the share price. In addition, the bid-ask spread tends to be large (up to about 15%), which can increase the cost of buying shares and reduce the value of shares sold upon exit.

Diploma

In summary, Nathan’s is attractively valued as a standalone company and is a compelling acquisition target, whether compared to publicly traded peers or acquisition multiples. The company is asset-light and generates stable free cash flow, while benefiting from a unique brand and flavor that is attracting increasing attention.

Whole Latte Love Café receives $10,000 for future academy

Michigan State Men’s Basketball Season Opener Announced