IYT ETF: Railroads defend themselves against previous union actions (BATS:IYT)

")

MOZCO Mateusz Szymanski

The iShares US Transportation ETF (Bats:IYT) is a relatively high US multiple pick that covers some of the railroad stocks as well as Uber (UBER). Railroad stocks offer a mixed picture, as we discussed in our last coverbecause of the success of unions pushing for more time off in addition to wages. Wages are a huge cost there. Uber is struggling with similar labor issues, with governments interfering to push through some sort of driver protections at Uber, also to make Uber less competitive with local taxi lobbies. Since ongoing inflation is likely to keep wage inflation at these companies as a key tailwind to the bottom line, we don’t want to buy IYT at a high multiple.

IYT breakdown

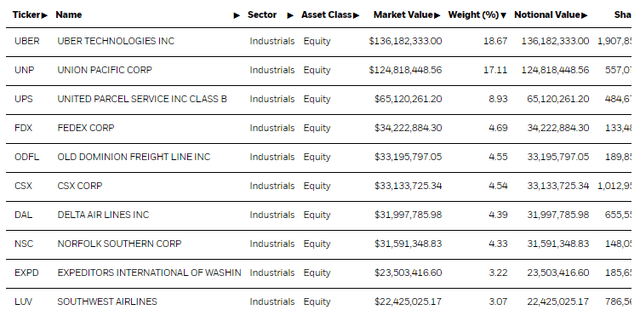

Top holdings from IYT (iShares.com)

IYT has a whole range of holdings at 44, but there is a clear bias towards the two top picks of Uber and Union Pacific (UNP). Together they make up 36% of the portfolio. Rail in general, including UNP, makes up 26% of the portfolio. 44% of the portfolio is just Uber and the rail stocks.

The first year P/E is around 20. This does not include Uber’s P/E, which is negative as Uber continues to invest in new services and products, driving it into negative profit territory. The expense ratio is 0.4%, which is not unreasonable for an ETF with a fairly specific industry mandate, less idiosyncratic than something like “healthcare.”

Uber’s 20x P/E implies an earnings yield slightly behind the current risk-free rate, meaning some level of earnings growth must be present. While freight has seen some good news recently, rail stocks are less certain. The picture is not entirely bad for them, taking UNP as an example. The move away from coal is doing their mix good. This offsets some of the pressure they are feeling in compensation costs, which have increased due to the need to increase headcount due to new collective bargaining agreements, as well as explicit wage increases that will be around 5% per year over the next few years. Last year they had a positive earnings impact from some one-off real estate gains. Without these, earnings would have increased slightly, which is impressive. While core growth is being achieved, it is complex and may not continue next year. They do not provide guidance.

We have similar concerns with Uber. It’s clear that Uber can’t get away with an operating model so different from taxis in various jurisdictions, before NYC and now Minnesota. That reduces the attractiveness of the stock. What’s happening in particular is that governments are insisting on effective wage increases, either explicitly or by requiring idle compensation, like with taxis. Uber has a lot of forces to contend with, it’s increasing its litigation reserves and generally has to invest a lot of money to maintain revenue growth. The company is also complex and struggles with fairly high leverage factors.

Bottom line

The railroad’s core growth isn’t too bad. Fuel surcharges declined, offset by lower fuel costs in earnings. Mix effects help offset the loss of one-time gains from last year. But they have multi-year commitments to raise wages and also need more staff. It’s not a sure thing. Uber is also relatively complex, and its ongoing tech growth profile could be tarnished if markets become more risk-averse again for some reason. The 20x P/E for the railroad stocks is no better deal than fair. As for Uber, someone investing in this ETF may want to avoid the fairly orthogonal exposure to the rest of the industrial stocks in the IYT, especially since growth is capital intensive and still unprofitable, with further headwinds coming from earnings due to regulatory developments and pressures that will penalize Uber in jurisdictions where it hasn’t already been penalized in one way or another. There are still plenty of better deals than a 5% earnings yield.

Thanks to our global reporting, we have increased our global macro commentary on our marketplace service here on Seeking Alpha. The Value LabWe focus on long-only value ideas where we try to find international mispriced stocks and target Portfolio return of approx. 4%We have done really well over the last 5 years, but we have also had to get our hands dirty in the international markets. If you are a value investor who is serious about protecting your wealth, we at Value Lab could be an inspiration to you.

Taylor Swift plans to attend “as many games as possible” during Travis Kelce’s upcoming season as the Eras Tour comes to an end

Can the Israeli government be expected to change during a war or remain the same? – Israel News