Three value stocks on the SIX Swiss Exchange with estimated discount opportunities

The recent fluctuations in the Swiss market, characterized by a downturn due to concerns about US economic data and interest rate decisions by the US Federal Reserve, have made investors cautious. In these conditions, identifying undervalued stocks on the SIX Swiss Exchange could offer opportunities for value-oriented investors.

The 10 most undervalued stocks in Switzerland based on cash flows

|

Surname |

Current price |

Fair value (estimated) |

Discount (estimated) |

|

COLTENE Holding (SWX:CLTN) |

CHF 47.00 |

75,89 CHF |

38.1% |

|

Burckhardt Compression Holding (SWX:BCHN) |

CHF 584.00 |

824,20 CHF |

29.1% |

|

Julius Baer Group (SWX:BAER) |

CHF 50.92 |

CHF 96.39 |

47.2% |

|

Sonova Holding (SWX:SOON) |

CHF 274.80 |

CHF 449.16 |

38.8% |

|

Temenos (SWX:TEMN) |

CHF 61.00 |

84,36 CHF |

27.7% |

|

Comet Holding (SWX:COTN) |

CHF 357.50 |

CHF 546.94 |

34.6% |

|

SGS (SWX:SGSN) |

80,76 CHF |

CHF 122.80 |

34.2% |

|

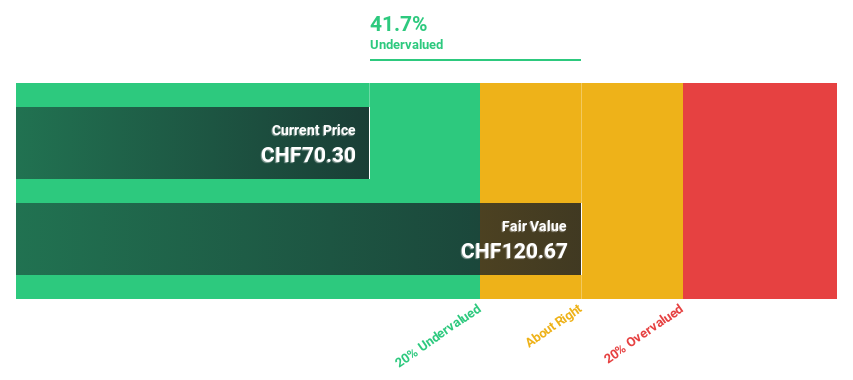

Medartis Holding (SWX:MED) |

69,70 CHF |

CHF 120.61 |

42.2% |

|

Kudelski (SWX:KUD) |

1,44 CHF |

1,87 CHF |

22.9% |

|

Galderma Group (SWX:GALD) |

CHF 76.49 |

150,16 CHF |

49.1% |

Click here to see the full list of 13 stocks from our Undervalued SIX Swiss Exchange Stocks Based on Cash Flows screener.

Let’s dive into some of the best options from the screener

Overview: Medartis Holding AG is a global medical technology company specializing in the development, manufacture and sale of implant solutions and has a market capitalization of approximately CHF 946.57 million.

Operations: The company generates sales of CHF 212.01 million in the medical devices sector.

Estimated discount to fair value: 42.2%

Medartis Holding is significantly undervalued based on discounted cash flow. The price is at CHF 69.7 against a fair value of CHF 120.61, which represents an undervaluation of 42.2%. Despite recent shareholder dilution and low forecast return on equity of 7%, the company’s earnings are expected to grow by 60.44% annually over the next three years, outperforming the Swiss market growth. In addition, revenue growth forecasts are at 13.3% annually, also above the market average.

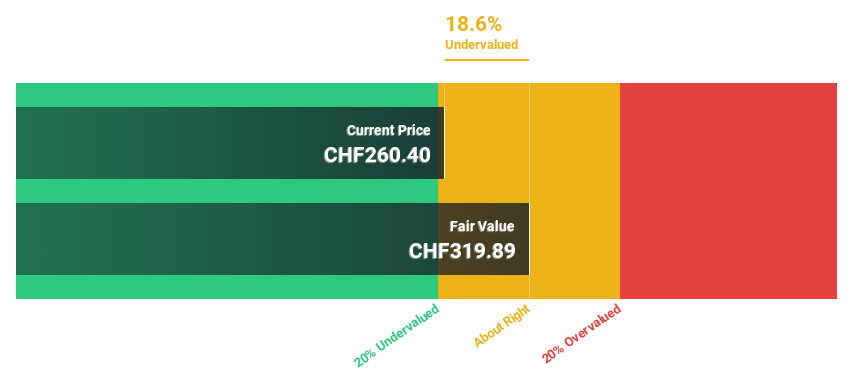

Overview: Sika AG is a global specialty chemicals company that offers products and systems for bonding, sealing, dampening, reinforcing and protecting in the construction sector and the automotive industry and has a market capitalization of around CHF 41.71 billion.

Operations: The company generates sales of CHF 9.45 billion with products from the construction industry and CHF 1.78 billion with products from industrial manufacturing.

Estimated discount to fair value: 18.9%

Sika is trading at CHF 260, 18.9% below its estimated fair value of CHF 320.77, which represents a slight undervaluation based on discounted cash flows. Although the company is highly leveraged, it is poised for robust growth. Earnings are expected to grow by 12.53% and sales by 6.2% per year – both rates exceeding the Swiss market average of 8.4% and 4.4% respectively. Recent expansions in China and Peru underscore Sika’s strategic initiatives to expand its global manufacturing footprint and product offering in emerging markets.

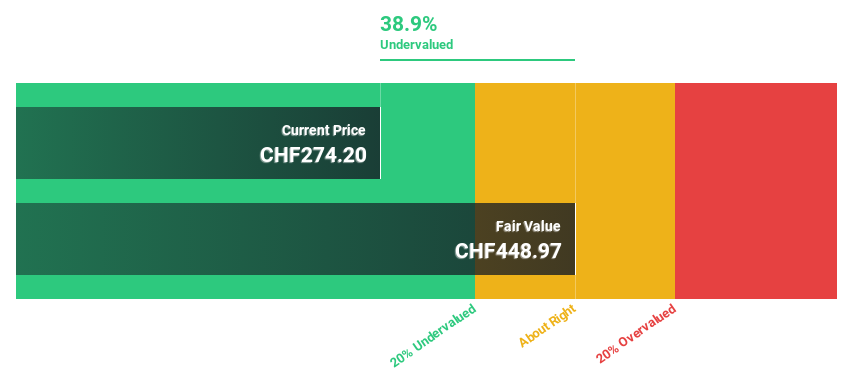

Overview: Sonova Holding AG is a company that produces and distributes hearing solutions for adults and children in various regions of the world. The market capitalization is approximately CHF 16.38 billion.

Operations: The company’s sales are generated mainly in two segments: cochlear implants, which contributed CHF 282.40 million, and hearing aids, which brought in CHF 3.36 billion.

Estimated discount to fair value: 38.8%

Sonova Holding’s current share price of CHF 274.8 is well below our calculated fair value of CHF 449.16, suggesting a potential undervaluation. The company’s earnings are expected to grow by 9.91% annually, outperforming the Swiss market forecast of 8.4%. Despite the high debt level, Sonova is expected to deliver a return on equity of 26.2% in three years. In addition, the sales growth forecast of 7.1% annually also exceeds the market average of 4.4%. The latest financial results showed a robust performance with sales of CHF 3.63 billion and net profit of CHF 609.5 million for the fiscal year ending March 2024.

Turning ideas into action

Curious about other options?

This Simply Wall St article is of a general nature. We provide commentary based solely on historical data and analyst forecasts, using an unbiased methodology. Our articles are not intended as financial advice. They do not constitute a recommendation to buy or sell stocks, and do not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Companies discussed in this article include SWX:MED, SWX:SIKA and SWX:SOON.

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]

Why will Málaga’s famous shopping street Calle Larios be covered with a huge decorative carpet of salt in the coming weeks?

Motorcyclist dies in 48 degree heat in Death Valley