A look at the intrinsic value of WestBond Enterprises Corporation (CVE:WBE)

")

Key findings

-

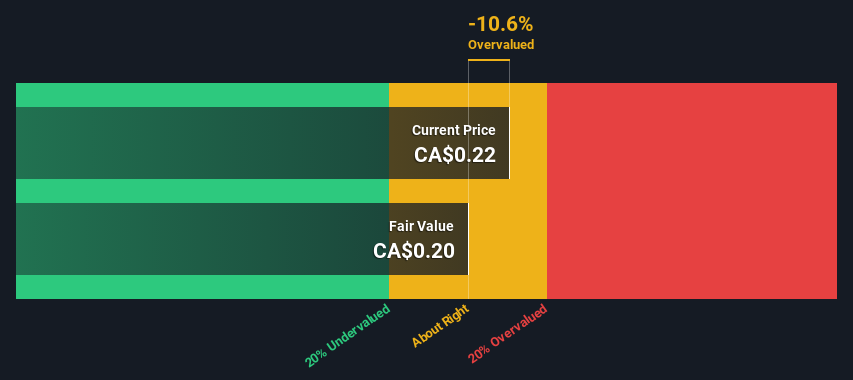

Using the dividend discount model, the fair value of WestBond Enterprises is estimated at CA$0.20.

-

WestBond Enterprises’ share price of CA$0.22 suggests that the price is at a similar level to the estimated fair value.

-

WestBond Enterprises’ competitors appear to be trading at a higher premium to fair value, based on the industry average of -37%.

In this article, we will estimate the intrinsic value of WestBond Enterprises Corporation (CVE:WBE) by taking the expected future cash flows and discounting them to today’s value. Our analysis will use the Discounted Cash Flow (DCF) model. Before you think you can’t understand it, just keep reading! It’s actually a lot less complex than you think.

We generally believe that the value of a company is the present value of all the cash it will generate in the future. However, a DCF is just one valuation metric among many and is not without its flaws. For those who enjoy stock analysis, the Simply Wall St analysis model presented here might be of interest.

View our latest analysis for WestBond Enterprises

The model

Because WestBond Enterprises operates in the forestry sector, we need to calculate intrinsic value a little differently. This approach uses dividends per share (DPS) because free cash flow is difficult to estimate and often unreported by analysts. Unless a company pays out the majority of its free cash flow as dividends, this method will typically underestimate the value of the stock. It uses the “Gordon Growth Model,” which simply assumes that dividend payments will continue to grow at a sustainable growth rate forever. For a number of reasons, a very conservative growth rate is used that cannot exceed that of a company’s gross domestic product (GDP). In this case, we used the 5-year average 10-year Treasury bond yield (1.8%). The expected dividend per share is then discounted to today’s value using a cost of equity of 12%. Relative to the current share price of CA$0.2, the company seems about fair at the time of writing. Since the assumptions of a calculation have a major impact on the valuation, it is better to consider it as a rough estimate and not accurate to the last cent.

Value per share = Expected dividend per share / (Discount rate – Perpetual growth rate)

= 0.02 CA$ / (12% – 1.8%)

= 0.2 CA$

The assumptions

The above calculation relies heavily on two assumptions. The first is the discount rate and the other is the cash flows. You don’t have to agree with these inputs, I recommend repeating the calculations yourself and playing with them. The DCF also doesn’t take into account the possible cyclicality of an industry or a company’s future capital needs and therefore doesn’t provide a complete picture of a company’s potential performance. Since we consider WestBond Enterprises as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or weighted average cost of capital, WACC) which takes debt into account. In this calculation, we used 12% which is based on a leveraged beta of 1.692. Beta is a measure of a stock’s volatility relative to the overall market. We get our beta from the industry average beta of globally comparable companies with an imposed limit of between 0.8 and 2.0 which is a reasonable range for a stable company.

Looking ahead:

Valuation is only one side of the coin when developing your investment thesis and ideally should not be the only analysis you examine for a company. It is not possible to get a foolproof valuation using a DCF model. Rather, it should be viewed as a guide to “what assumptions must hold for this stock to be under/overvalued.” If a company grows differently or its cost of equity or risk-free rate changes significantly, the outcome can be very different. For WestBond Enterprises, we have compiled three relevant factors that you should examine in more detail:

-

Risks: Every company has them, and we have found 3 warning signs for WestBond Enterprises (1 of which is worrying!) that you should know about.

-

Other solid companies: Low debt, high returns on equity, and good past performance are the foundation of a strong company. Check out our interactive list of stocks with solid business fundamentals to see if there are any other companies you may not have considered!

-

Other environmentally friendly companies: Are you concerned about the environment and believe that consumers will increasingly buy environmentally friendly products? Browse through our interactive list of companies thinking about a greener future and discover some stocks you may not have thought of yet!

PS The Simply Wall St app runs a discounted cash flow valuation for every stock on the TSXV every day. If you want to find the calculation for other stocks, just search here.

Do you have feedback on this article? Are you concerned about the content? Get in touch directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Join a paid user research session

You will receive a $30 Amazon Gift Card for 1 hour of your time and help us build better investment tools for individual investors like you. Sign up here

Report: McDonald’s is weakening in customer satisfaction

See road closures and parking plan for the University of Michigan move-in