A look at the fair value of Asian Granito India Limited (NSE:ASIANTILES)

")

Today I’m going to provide a simple overview of a valuation method that estimates the attractiveness of Asian Granito India Limited (NSE:ASIANTILES) as an investment opportunity by taking the expected future cash flows and discounting them to their present value. This is done using the Discounted Cash Flows (DCF) model. This may sound complicated, but it’s actually quite simple! Those interested in learning more about intrinsic value should check out Simply Wall St’s analysis model. Please also note that this article was written in August 2018, so be sure to check out the updated calculation by following the link below.

Check out our latest analysis for Asian Granito India

What is the value?

I use the two-stage growth model, which simply means that we consider two stages of growth of the company. In the initial stage, the company may have a higher growth rate, and in the second stage, a stable growth rate is usually assumed over time. First, we need to get estimates of the next five years’ cash flows. To do this, I used the consensus of the analysts covering the stock, as you can see below. Then I discount the sum of these cash flows to get an estimate of the present value.

5-year cash flow forecast

|

2019 |

2020 |

2021 |

2022 |

2023 |

|

|

Leveraged FCF (₹, million) |

573,67 € |

360,50 € |

395,78 € |

434,51 € |

477,03 € |

|

source |

Analyst x3 |

Analyst x2 |

Estimated at 9.79% |

Estimated at 9.79% |

Estimated at 9.79% |

|

Present value discounted at 13.92% |

503,56 € |

277,77 € |

267,68 € |

257,96 € |

248,60 € |

Present value of 5-year cash flow (PVCF)= ₹1.56 billion

We now need to calculate the terminal value, which takes into account all future cash flows after the five years. For various reasons, a very conservative growth rate is used, which cannot exceed that of GDP. In this case, I have used the interest rate on 10-year Treasury bonds (7.7%). In the same way as with the 5-year “growth” period, we discount this to today’s value at a cost of equity of 13.9%.

Final value (TV) = FCF2022 × (1 + g) ÷ (r – g) = ₹477.0 million × (1 + 7.7%) ÷ (13.9% – 7.7%) = ₹8.30 billion

Present value of terminal value (PVTV) = TV / (1 + r)5 = ₹8.30 billion ÷ (1 + 13.9%)5 = ₹4.32 billion

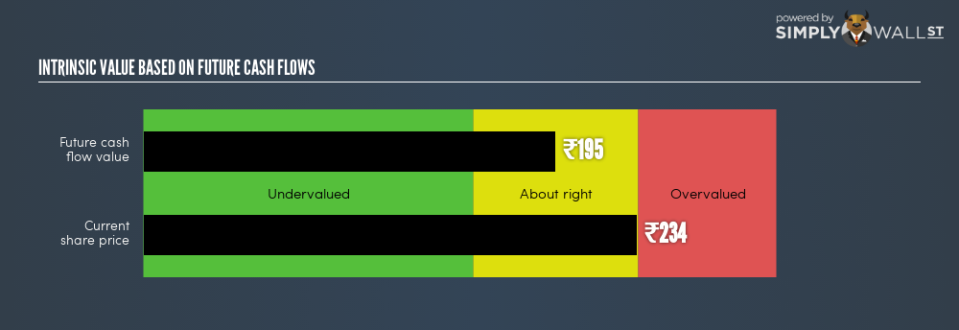

The total value is the sum of the next five years’ cash flows and the discounted terminal value, which gives the total value of equity, which in this case is ₹5.88 billion. The final step is to divide the equity value by the number of shares issued. If the share is a depositary receipt (represents a specific number of shares of a foreign company), we use the appropriate number. This gives an intrinsic value of ₹195.44Relative to the current share price of ₹233.9, the stock is fairly valued, perhaps even slightly overvalued, at the time of writing.

Important assumptions

I would like to point out that the key inputs for a discounted cash flow are the discount rate and of course the actual cash flows. You don’t have to agree with my inputs, I recommend repeating the calculations yourself and playing around with it. Since we are considering Asian Granito India as potential shareholders, the cost of equity is used as the discount rate and not the cost of capital (or weighted average cost of capital, WACC) which takes into account the debt. In this calculation, I have used 13.9% which is based on a leveraged beta of 0.852. This is derived from the bottom-up beta method based on comparable companies with an imposed limit of 0.8 to 2.0 which is a reasonable range for a stable company.

Next Steps:

Although a company’s valuation is important, it should not be the only metric you consider when researching a company. For ASIANTILES, I have compiled three relevant aspects that you should examine in more detail:

-

Financial health: Does ASIANTILES have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors such as leverage and risk.

-

Future income: How does ASIANTILES’ growth rate compare to competitors and the overall market? Learn more about analyst consensus numbers for the coming years by using our free chart of analyst growth expectations.

-

Other high-quality alternatives: Are there other high-quality stocks you could hold instead of ASIANTILES? Explore our interactive list of high-quality stocks to get an idea of what else you might be missing out on!

PS. Simply Wall St app calculates discounted cash flow for every stock on NSE every 6 hours. If you want to find the calculation for other stocks, just search here.

To help our readers look beyond the short-term volatility of the financial market, we aim to provide you with long-term focused research analysis based solely on fundamental data. Please note that our analysis does not take into account the latest price-sensitive company announcements.

The author is an independent writer and had no ownership interest in any stocks mentioned at the time of publication. If you find any errors that need to be corrected, please contact the editor at [email protected].

“Scrubs” star Sarah Chalke lands next film role in Alan Ritchson’s action comedy

Player ratings for the Netherlands vs France match: The stars are disappointing and Xavi Simons’ goal is controversially disallowed