IUS: A value ETF based on a company size allocation criterion (NASDAQ:IUS)

")

deepblue4you

While equity market leadership is focused on mega-caps, funds like the Invesco RAFI Strategic US ETF (NASDAQ:IUS) offer a different approach by weighting stocks based on operating metrics such as revenue, cash flow and book value, as opposed to market-cap weighted benchmark indices.

This approach used by IUS gives this ETF a bias towards value given its low valuation multiples and also offers greater exposure to companies and sectors that can benefit from an expansion of stock market gains in the coming months. Nevertheless, I think IUS is an interesting alternative for investors looking for value and diversified investment strategies.

ETF description and highlights

IUS is an exchange-traded fund that aims to provide exposure to high-quality, large companies in the US market, tracking the allocation of the underlying Invesco Strategic US Index.

Based on a universe of US stocks with The Invesco Strategic US Index methodology assigns each security a company size score based on the average of four factors over the last five years: 1) revenue, 2) operating cash flow, 3) return on assets, and 4) book value. It then creates the first filter by selecting the top 90% of the initial universe of eligible stocks.

After the initial screening, a second filter is applied to select the top 80% of remaining eligible stocks based on a quality score. This quality score is calculated as the average of two quality factors: 1) efficiency (previous year’s sales-to-assets ratio) and 2) growth (percentage of sales-to-assets ratio over the past five years).

After these two reviews, the selected stocks will be included in the Invesco Strategic US Index, and the weighting of each stock will be based on its company size. Reweighting and reconstitution will occur annually.

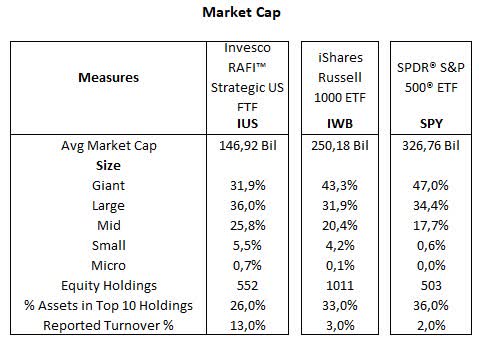

As of July 11, 2024, IUS has allocations to 552 companies tracking the underlying Invesco Strategic US Index with an average market capitalization of $146.9 billion, with 31.9% of total assets in mega caps, 36.0% in large caps, 25.8% in mid caps, and only a marginal 5.5% exposure to small caps.

This allocation is relatively more large cap than mega cap compared to the Russell 1000 Index, a benchmark for large cap companies in the US market, represented here by the iShares Russell 1000 ETF (IWB). This benchmark has an average market capitalization of $250.2 billion and a heavier allocation to mega caps, with 43.3% of total assets and 31.9% to large caps. Both IUS and the Russell 1000 Index are primarily comprised of larger cap companies, as mid and small caps make up less than a third of the total composition.

IUS’s top 10 holdings (Apple, Alphabet, Microsoft, Berkshire Hathaway, Exxon Mobil, Meta, Amazon, Chevron, AT&T and UnitedHealth) represent 26% of total assets and are a mix of large technology companies and some value players such as Berkshire, Exxon and Chevron.

Morningstar, consolidated by the author

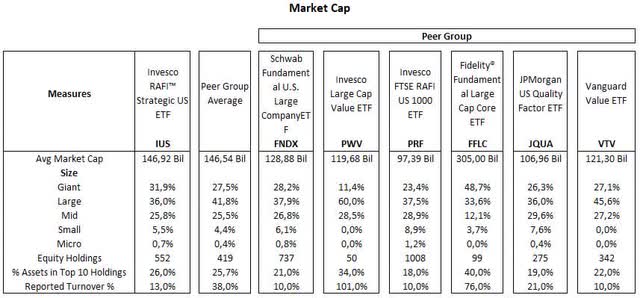

Below is a comparison between IUS and a peer group of large-cap ETFs with a fundamental approach. The first and third ETFs (FNDX and IUS) follow RAFI indices with a fundamental approach. PMV and VTV are both value-oriented funds, with PMV being a fairly concentrated fund with only 50 holdings. Meanwhile, JQUA follows a quality-focused methodology and FFLC is an actively managed ETF.

Interestingly, IUS and the peer group average have relatively similar exposures across different holding sizes, with few differences, such as FFLC’s higher allocation to mega-caps.

Morningstar, consolidated by the author

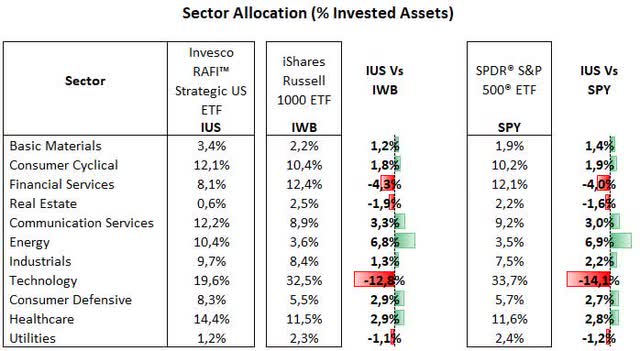

From a sector allocation perspective, IUS’ largest allocation is the technology sector at 19.6% of total equities, followed by healthcare at 14.4%, communication services 12.2%, consumer discretionary 12.1%, energy 10.4%, industrials 9.7%, consumer discretionary 8.3%, financial services 8.1%, materials 3.4%, utilities 1.2% and real estate 0.6%. Relative to the Russell 1000 index, IUS is overweight in energy (+6.8%), communication services (+3.3%) and healthcare (+2.9%), but heavily underweight in technology (-12.8%) and financial services (-4.3%).

Morningstar, consolidated by the author

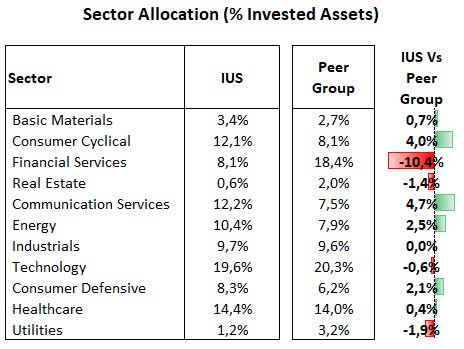

Compared to its large-cap ETF peer group, IUS is overweight in communication services and consumer discretionary, while underweight allocations are concentrated in financial services and utilities. IUS’s divergence from its peer group is consistent with the underlying index methodology, where the company size score includes metrics such as revenue and operating cash flow, while the quality score focuses on efficiency and growth rather than valuations. Therefore, it is no surprise that IUS has a higher allocation to profitable and high-revenue companies in the communication services industry than to low-multiple sectors such as financials and utilities.

Morningstar, consolidated by the author

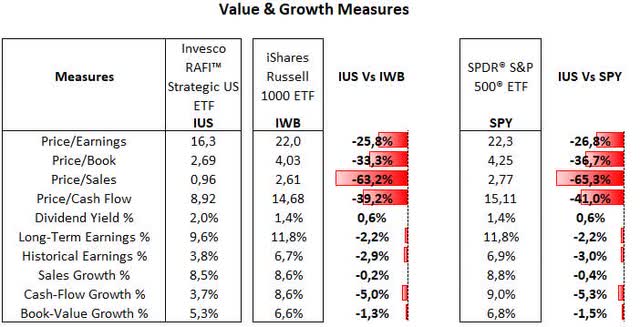

IUS’s multiples are significantly lower than those of the Russell 1000 and S&P 500 indices. For example, IUS has a P/E of 16.3, which is 25% below the benchmark’s 22.0x multiple. This is largely due to IUS’s small exposure to a premium sector like technology, coupled with its overweight in less important sectors like energy, consumer staples and healthcare.

Morningstar, consolidated by the author

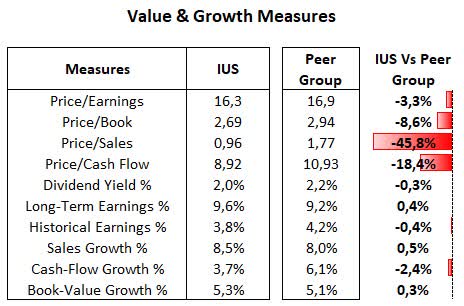

Compared to the peer group, IUS’s P/E ratio is similar to that of its competitors, but other valuation metrics are significantly lower because the underlying index methodology places greater emphasis on metrics such as book value, sales and cash flow.

Morningstar, consolidated by the author

Short-term underperformance impacted by low allocation to Nvidia

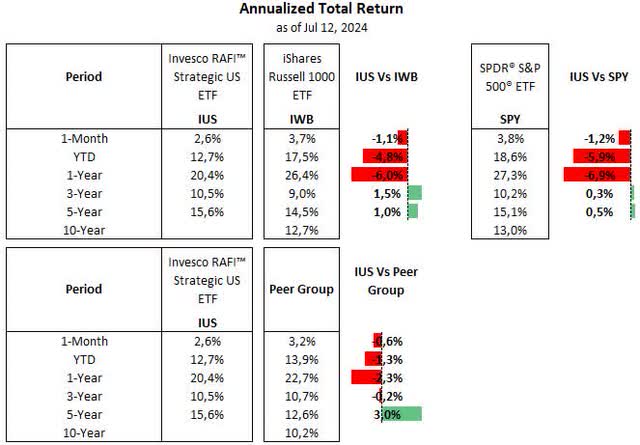

IUS’s total return has been positive overall over the long term, slightly outperforming the Russell 1000 Index and peer group. However, this has not been the case over the past year, as the fund gained 20.4% while the Russell 1000 Index returned just 26.4%.

This underperformance is primarily due to one reason: IUS’s low exposure to Nvidia, which represents only 0.90% of IUS’s total capital, versus 5.9% for the Russell 1000 Index, as IUS was unable to experience Nviodia’s meteoric gains of 194% over the past 12 months. Thus, Nvidia shares contributed only 2.8% to IUS’s returns during this period, while they accounted for almost 11.5% for the Russell 1000 Index, a gap of 8.6% due to this stock alone. Without Nvidia’s influence, IUS’s performance over the past 12 months would have been 17.6% versus 14.9% for the Russell 1000 Index.

Morningstar, consolidated by the author

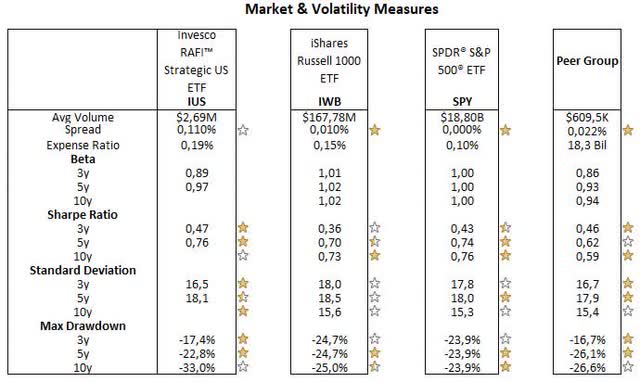

IUS’s equity allocation has resulted in lower volatility compared to the Russell 1000 and S&P 500 indices, as reflected in the lower beta, standard deviation and maximum drawdown. This has resulted in better risk-adjusted returns on a relative basis, as measured by the Sharpe ratio.

Morningstar, consolidated by the author

In summary, IUS’s underlying index allocation strategy has created a dynamic that avoids over-allocation to mega-caps, as the index uses operating metrics such as revenue, cash flow and book value to weight stocks, rather than market capitalization. Nevertheless, large technology companies such as Apple, Alphabet, Microsoft and Amazon are still among the top 10 holdings, while an overweight bias towards energy, healthcare and consumer staples gives IUS a bias towards value, as shown by its low valuation multiples.

However, the small allocation to Nvidia has been a negative for performance over the past 12 months and may continue to be so for the foreseeable future as narrow market leadership can persist for an extended period. IUS appears well positioned for a potential extension of stock market gains once the start of an easing cycle can benefit other sectors outside of technology.

R&B singer Victoria Monét shows off her stunning six-pack

Tickets are still available for the presentation of Francis Gary Powers’ Capture in the Cold War on July 29