Samsara: Attractive value proposition with new growth catalysts (NYSE:IOT)

")

NewSaetiew/iStock via Getty Images

Summary

Following my report on Samsara (NYSE:IOT) in March 2024, which I rated as a buy as the execution was excellent and I expected the market to value IOT at a higher multiple than its historical value. In general, this post is intended to provide an update of my thoughts on the business and the stock. I am much more bullish on IOT after reviewing the new product launches. I believe that IOT’s value proposition to customers has improved significantly with these new products and that IOT should see strong adoption, further improving its stickiness and competitive advantage. The growth trajectory remains attractive as many customers have not yet met their renewal cycles and IOT is still underpenetrated in terms of customers acquired.

Investment thesis

I believe that the growth prospects for IOT have just increased quite a bit better with the latest product launches: Asset Tag, Connected Workflows and Connected Training.

Internet of Things

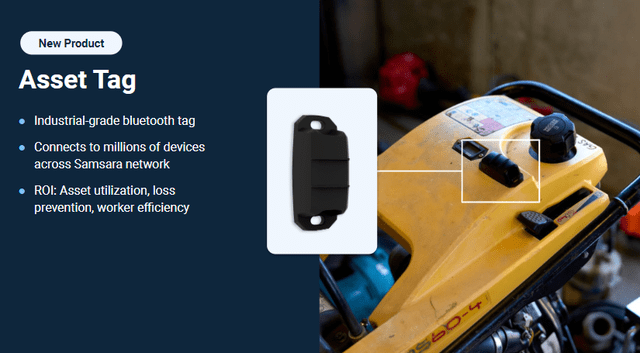

IOT’s new Asset Tag product is something I’m very excited about and I see it as a game changer for customers. A key differentiator is the smaller size. The main reason IOT has been able to reduce the size of the product is because it uses a completely new architecture compared to the traditional connection method over the cellular network. This product leverages IOT’s extensive network of IOT devices to connect to nearby gateways and IOT hardware. Additionally, because these asset tags can communicate with gateways on the network, they are able to communicate over a longer range than RFIDs that rely on nearby readers. Ultimately, it improves customers’ ability to recover assets, improves asset utilization and ensures the right tools are in the right job at the right time.

This product basically increases the appeal of IoT and makes it significantly harder for competitors to keep up. Because of the way the architecture works, the customer needs to have a lot of IoT hardware in the environment, and by that definition, the customer is already using IoT hardware and devices. To switch to another vendor, they would have to replace all of that equipment, which will cause operational issues over time.

Internet of Things

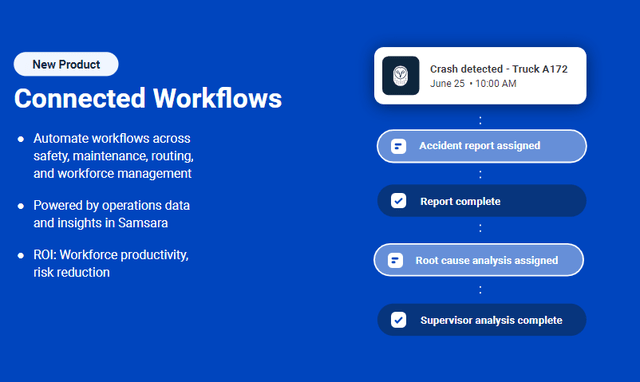

The second product I really like is Connected Workflows (CW). CW is a platform that integrates Connected Forms with data and automation. Two key features in particular stand out. First, the ability to automatically trigger an event when another event occurs. For example, if a supervisor enters a geofence (Event 1), they will automatically be prompted to perform a security check (Event 2, triggered by Event 1). Second, the ability to pre-populate various CW-dependent forms with the data IOT has already collected (i.e. the security checklist can be pre-populated with the location, date, key things to check, etc.), which speeds up the whole process.

You can imagine how powerful this automation process is, as it allows for the automation of tasks with contextual data to trigger multi-step workflows. In other words, there is less need for a team to constantly be on the lookout for errors, be ready to notify the appropriate personnel, and plan what to do in case of triggers. This entire human process is inefficient and costly, so I believe that automating and streamlining traditionally manual tasks will be a major driver for adoption.

Internet of Things

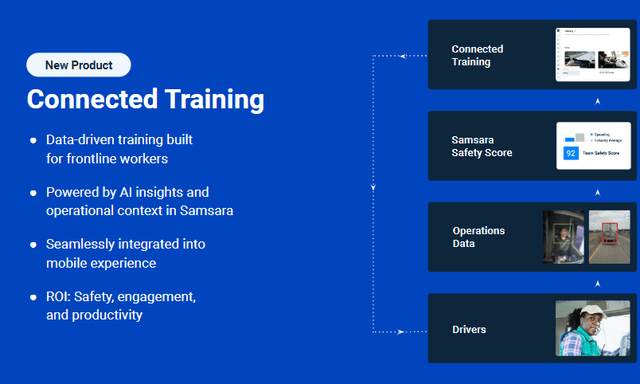

The third product is Connected Training (CT). CT allows customers to proactively deliver required training in response to events. For example, a driver whose attention is distracted by their phone can receive an automated training session that they must complete at their next rest stop. Additionally, customers have the ability to develop their very own training programs (some customers have more niche needs, so this certainly helps). Given that safety is one of the most important elements underlying customers look for, I expect strong adoption of CT.

Internet of Things

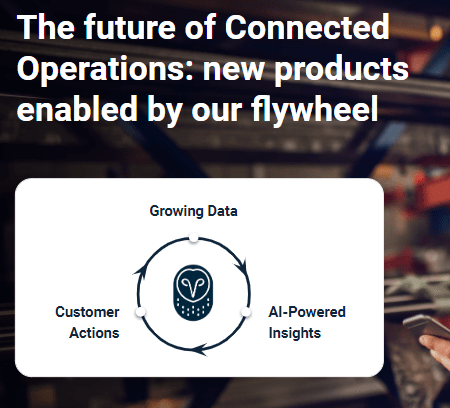

With the introduction of these products, which I expect to see widespread adoption, the competitive advantage of IoT should increase significantly. The side effect of the introduction of these products is that IoT can collect significantly more data than in the past, and this becomes a data flywheel: more data leads to more insights, which enables IoT to improve customer productivity and innovate products. All of this enables IoT to improve its value proposition to customers (improve productivity, safety and ultimately cost).

Internet of Things Internet of Things

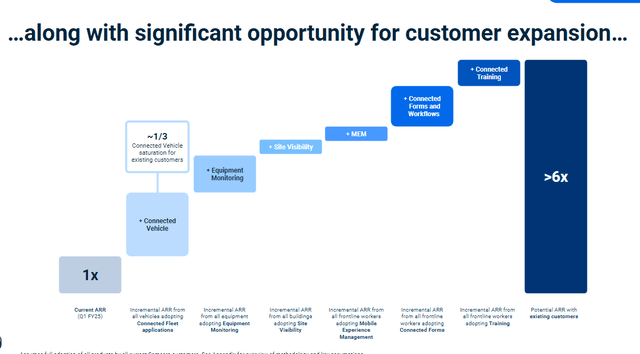

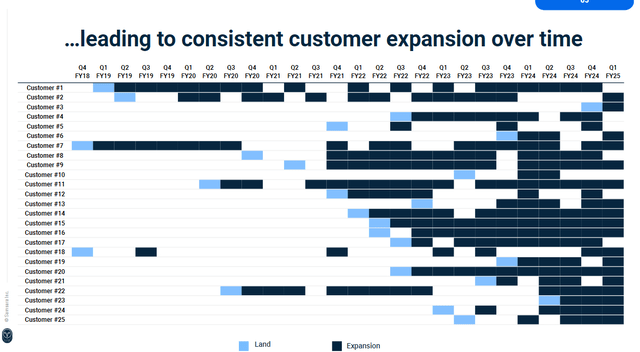

Therefore, I remain firmly convinced that IOT will deliver consistently strong growth with increasing margins for the foreseeable future. In fact, I became even more optimistic after reviewing the investor day presentation, as management noted during the investor day that they see a lot of opportunities to upsell or cross-sell in the current base. I point this out because a significant portion of IOT’s customer base has not yet met its renewal cycle, meaning there is still a lot of room for IOT to upsell or cross-sell all of these new products.

Remember, we have only been selling for a little over eight years and are doing three to five year deals, so less than 50% of our total ARR has still been through a renewal cycle. As that ARR continues to renew over time, it will drive more leverage in sales and marketing. Investor Day Transcript

Evaluation

Own calculation

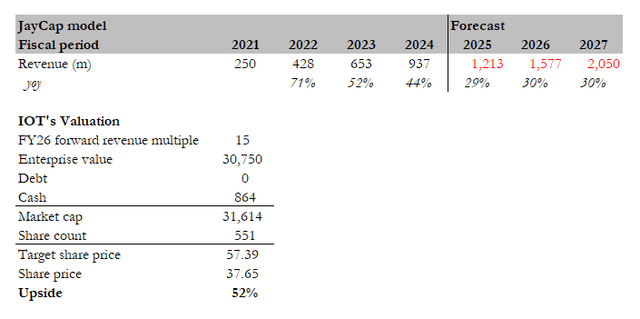

My target price for IOT is ~$57 according to my model. My model is now based on FY27 numbers as I am modeling 2 years ahead of the current fiscal year. I am much more optimistic about IOT’s growth now than I was a few months ago and thankfully the market does not seem to have fully priced this in yet. My latest model assumes IOT will generate $1.213 billion in revenue in FY25 (top end of management’s guidance), representing 29% growth with growth heading towards 30% over the next two years. I must point out that IOT could well achieve much higher growth given the new products being launched (IOT’s growth was 44% in FY24 for reference). The catalyst for higher growth could be rate cuts, which will lower the cost of capital for IOT’s customers and allow them to invest more in new digital solutions.

I have also increased my valuation multiple assumption from 13x to 15x as I am more optimistic about the growth potential today. The market’s willingness to apply a higher multiple after the investor day (from ~12x to 15x today) also suggests that investors are positive about the new products.

risk

IOT’s gross margin could fluctuate in the short term as IOT point-of-sale devices used to collect customer data are on the rise. If the new products (Asset Tag) see a huge surge in adoption, this could put pressure on gross margin, and the market could extrapolate this weakness in its models. Any data breach will significantly damage IOT’s reputation. Since customers value privacy and data security (they don’t want others to know where their assets are), this could reduce customer confidence in the reliability of IOT’s products.

Diploma

In summary, I am buying IOT. I believe IOT’s recent product launches significantly improve the value proposition and solidify the competitive advantage, which has made me even more optimistic about the growth potential. All of these new products are driving a data flywheel effect for IOT that will help further refine the IOT offering. Looking ahead, there is still significant growth potential and untapped upselling potential.

USA allows Ukraine to use its weapons to attack Russian forces not only in the Kharkiv region

Country star dedicates controversial song to Trump after assassination attempt