Weave Communications stock: Market leader with strong value proposition (NYSE:WEAV)

")

Melpomenem/iStock via Getty Images

Investment overview

My recommendation for Weave Communications (NYSE:WEAV) is a Buy rating. WEAV is a market leader in the space it competes in and I expect it to continue to gain market share given the strong value Proposition that its platform offers to small businesses. Since it can sustain 20% growth even in the current difficult macroeconomic environment, I am convinced that it can sustain 20% growth in the coming years.

Business Overview

WEAV

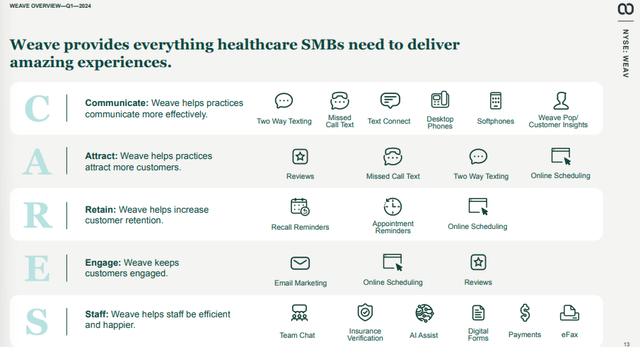

WEAV provides a customer engagement platform for small businesses such as dental practices, opticians, veterinarians, home services and others. The WEAV platform combines four key functions – Unified Communications as a Service, Communications Platform as a Service, Marketing and Payment Processing – in one product.

Life for small businesses becomes much easier

WEAV

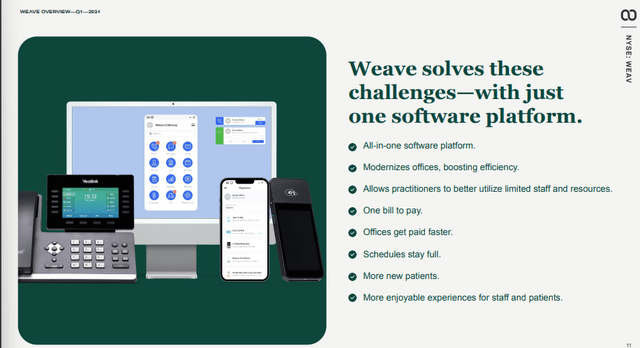

Smaller companies usually do not have the necessary IT skills or sufficient Save resources to invest in the best digital solutions. Even when they do, it’s usually by stringing together multiple point solutions that don’t work well together. This leads to a lack of efficiency: employees have to learn multiple platforms, work with multiple platforms for a workflow because they aren’t well integrated with each other, etc. Ultimately, this leads to low customer satisfaction. A good example is when you call a dentist in your area to make an appointment but you’re stuck on hold for 15 minutes. (I’d hang up and call another dentist if I had to wait that long.) This is why WEAV is critical for these companies. WEAV’s offering is essentially an all-in-one practice management platform (answer phone calls, schedule appointments, SMS reminders) and also includes other value-added services like payment processing.

Unlike multipoint solutions, using WEAV is much more productive and efficient. With WEAV, when a patient calls, the front desk can immediately see important details like names, upcoming appointments, outstanding balances, etc. This already makes life easier for staff, as they don’t have to search the Excel database or flip through physical folders to find the patient’s file. Going back to my dentist appointment above, staff can use WEAV’s features to find the next best appointment time. By using just one platform to handle this entire process (including payments, which I’ll discuss in more detail below), the company becomes much more productive. In some cases, I can also imagine these small businesses downsizing their customer-facing team, which saves costs.

WEAV

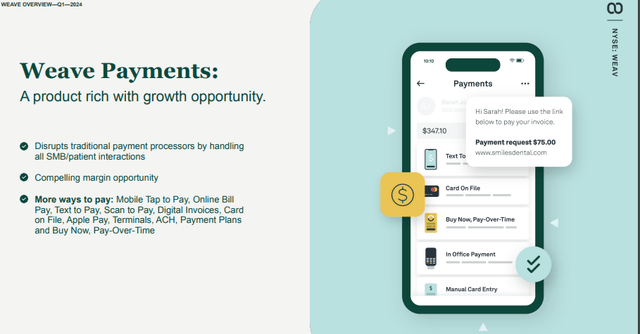

I am a firm believer in the WEAV payment solution as it will make life much easier for small businesses and will also improve WEAV retention rate. Cash flow management is a very important aspect for small businesses as they usually do not have a very strong balance sheet. The traditional method is to write down how much the customer owes and constantly call customers to remind them to pay next time. This is extremely inefficient from an operational perspective and results in poor cash collection.

With a digital payment processor, small businesses can better track outstanding balances and send notifications to consumers with just a few clicks. From a customer perspective, the payment process is also much more straightforward, as it is also much easier to simply pay over the phone (via digital wallets or credit cards) than to go to the clinic to pay. The end result is less effort spent tracking payments and faster receipt of payments.

Since WEAV is already the main platform its customers use to deal with their patients, I believe it is best positioned to offer payment processing services as it integrates seamlessly with the core product (so there are no issues with receiving payments). So far, this is still a small part of the business, with less than 10% of revenue in Q4 2023. However, I expect this to grow quickly in the future as the value proposition is just too strong compared to traditional methods. Aside from that, it also improves the customer retention rate for WEAV as it becomes more integrated into its customers’ workflow. I would remind readers that these are small businesses, so once they get used to a product that works well, it is very unlikely that they will go through the trouble of removing and replacing everything, especially if it affects their ability to pay. WEAV’s net retention rate over the past few years (>90%) really shows how integrated it is, as small companies typically have higher turnover (deals fail and close) than large companies.

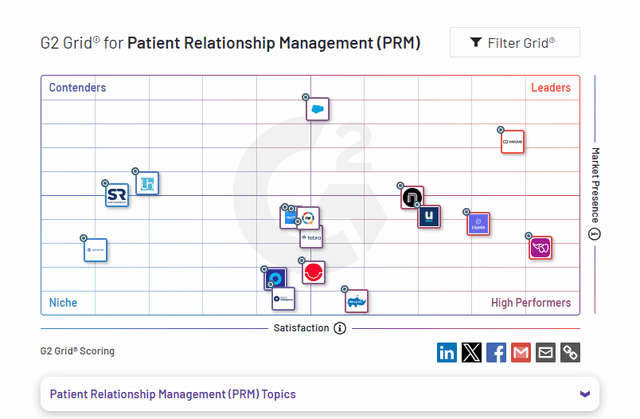

As far as competition goes, WEAV is the market leader for its target audience. The main competition is actually all-point solutions that do not integrate well. I expect WEAV to continue to gain market share in this market because its solution is targeted at small customers.

G2

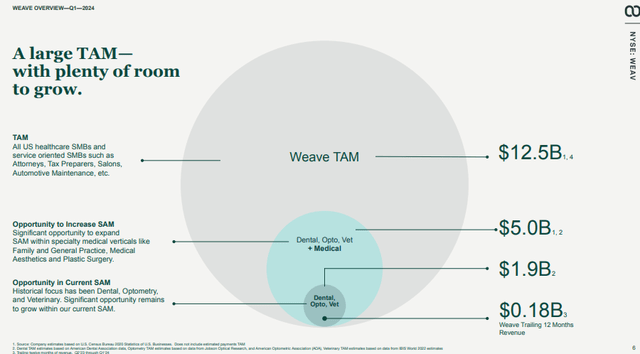

Target market: $12.5 billion

WEAV

Although the revenue and profits WEAV can generate from each small business are not very high (given the size of the customers), the TAM is extremely large because these businesses make up a large portion of the economy. Based on WEAV’s trailing 12 months, the company has generated around $180 million in revenue in Q1 2024, which represents only a small fraction of the addressable market.

The question is whether WEAV has been able to succeed and grow in this large market. The answer is yes, as WEAV has managed to: (1) increase its number of locations from 13,000 in FY19 to 31,000 in FY23; (2) deliver strong revenue growth from $45 million in FY20 to ~$180 million over the last 12 months, with Q1 2024 growth in line with Q1 2023 at 19% (showing that the company is not heavily impacted by the weak macroeconomy).

Evaluation

Redfox Capital Ideas

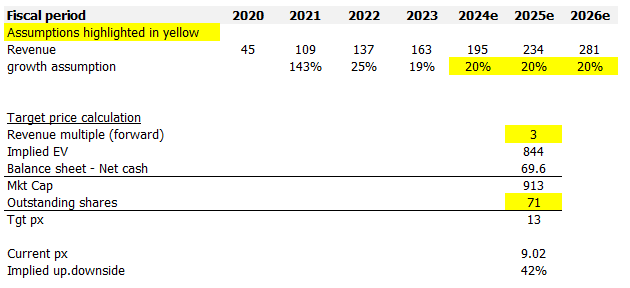

I model WEAV using a forward revenue approach and, based on my assumptions, I believe WEAV is worth $13. WEAV’s growth over the past few quarters has essentially set a base growth rate for the coming years. In my view, the company has continued to grow at 20% despite the worst macroeconomic environment in recent history, which should have hurt WEAV greatly given its focus on small businesses. With interest rates now likely to fall, easing pressure on small businesses, growth should be at least 20%. This should support the current revenue multiple of 3x.

Risks

WEAV solutions may not perform as well outside of their current focus market. This could limit growth prospects. In addition, further rate hikes over a longer period of time will certainly place a greater burden on small companies, and WEAV will ultimately suffer. WEAV is not currently profitable, which I think is understandable given the focus on growth. However, if WEAV does not show further signs of margin improvement as it grows, this could put pressure on valuations.

Diploma

I recommend WEAV for purchase. WEAV is a market leader in this space. Its all-in-one platform significantly increases operational efficiency, increases customer satisfaction, and improves cash flow management for users. Execution has been excellent, as evidenced by strong revenue growth and expanding customer base. I expect the company to sustain 20% growth in the coming years. This should support the current 3x forward revenue, leading to a price target of $13.

Nintendo on the inappropriate use of its intellectual property and games: “Action must be taken”

Anna Benson to Dr. Phil – “I’m the most famous baseball wife since Marilyn Monroe”