Intuitive Surgical shares: Price rises steeply, but is now close to fair value (rating downgrade) (ISRG)

(ISRG)")

PhonlamaiPhoto/iStock via Getty Images

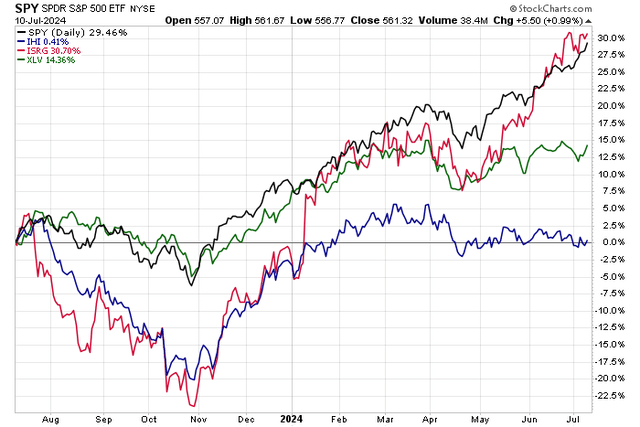

Intuitive Surgery (NASDAQ:ISRG) was a winner last year, while the healthcare sector has lost ground compared to the S&P 500. Within the sector, the iShares US Medical Devices ETF (IHI) has barely made any On a total return basis, stocks have been up over the past 52 weeks. This relative weakness comes ahead of the second-quarter earnings season.

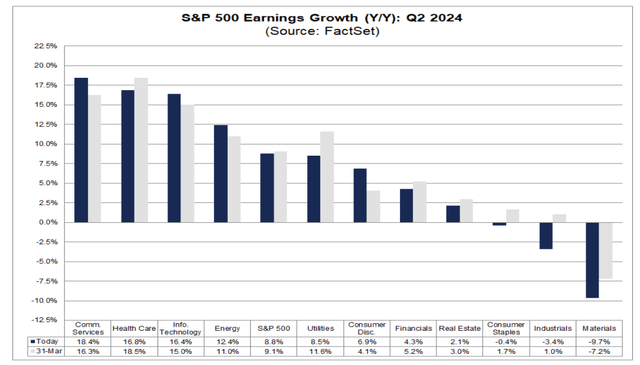

FactsSet However, the data shows strong EPS growth in Q2 2024 in healthcare, so we generally Encouraging figures and perhaps optimistic guidance from this underperforming niche of the S&P 500.

As far as ISRG is concerned, I am Downgrade the stock from a buy to a hold. It’s been a while since I last analyzed the California-based healthcare equipment industry stock with a market cap of $158 billion. After a series of strong earnings reports and solid gains from da Vinci Surgical System, along with the fact that it is a favorite For momentum investors, shares now trade at a non-GAAP P/E of 81. However, bulls can point to robust EPS growth going forward and a very strong technical chart.

ISRG beats medical device stocks, S&P 500 year-on-year

Stockcharts.com

Sectoral EPS growth rates expected in Q2 2024

Facts

According to Bank of America Global Research, IRG is the pioneer and market leader in soft tissue surgery robotics, first receiving FDA clearance over 20 years ago. ISRG sells robotic systems and related instruments that can be used in a wide range of surgical procedures. ISRG has an installed base of nearly 8,000 robots worldwide.

Already in April Posted a solid set of quarterly numbers. Non-GAAP earnings per share (EPS) for Q1 of $1.50 beat the Wall Street consensus forecast of $1.42, while revenue of $1.89 billion, up 12% year over year, was a modest increase. The strong financial performance at the start of 2024 was driven by growth in da Vinci procedure volumes and, importantly, an increase in the installed base of its systems. Robust demand due to a large backlog of procedures post-COVID was seen as a significant increase. Overall, global da Vinci procedures increased 16% year-over-year. Net profit of $547 million increased to over $361 million in the first quarter of 2023.

ISRG is a leader in robotic healthcare technology, and the launch of the da Vinci Surgical System (dV5) is expected to continue to boost the company’s revenue and earnings in the coming years. The question investors must be asking today is, “How much am I willing to pay for this growth stock?” Another positive factor is that the company’s pay-per-click model is becoming more widely used in hospitals, making it easier for healthcare providers to expand their capacity. ISRG’s high growth comes at a time when some of its surgical peers have reported more modest growth.

ISRG’s key risks include a decline in backlog as the peak of the COVID pandemic occurred years ago, lower hospital spending in the event of a funding cut or a macroeconomic slowdown, and increased competition as other medical device companies develop comparable technologies and robots more quickly.

Ahead of next week’s Q2 report, the options market has priced in a 4.4% move when analyzing this at-the-money straddle. After the last four quarterly releases, shares have traded lower following the earnings release.

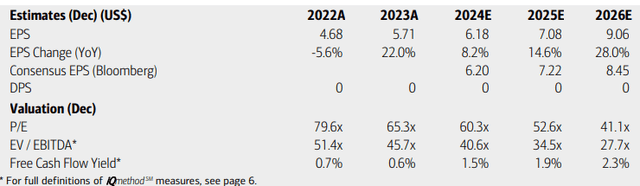

As for earnings, analysts at BofA expect operating earnings per share to grow by a high single-digit percentage this year, with gains accelerating over the following two years. Current consensus numbers from Seeking Alpha show a similar but slightly less optimistic growth trajectory, while revenues are expected to grow 13% this year, 16% in 2025 and 15% in 2026. The company is not expected to pay dividends.

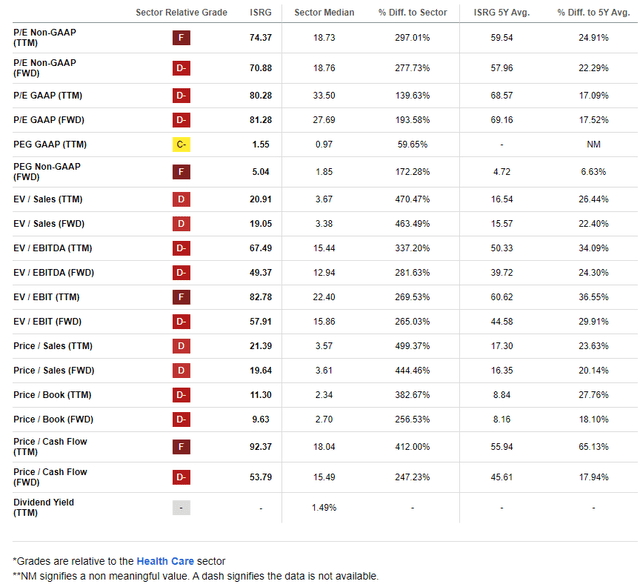

With a P/E ratio of over 70 and an EV/EBITDA ratio roughly three times that of the overall market, there is certainly a growth premium added to the current valuation. While ISRG has positive free cash flow, its FCF yield is modest.

ISRG: Earnings, valuation and free cash flow forecasts

BofA Global Research

If we have a PEG ratio approach With ISRG, I see the valuation as follows. If we assume EPS growth of 15% and apply the company’s 5-year average PEG of 4.7x, then we are talking about a fair P/E of around 70. That seems aggressive at first glance, but is now the average across all cycles.

If we assume current year earnings of $6.50 and apply 70x, the stock should be around $455 – very close to where it is today. If we were to use 2025 earnings per share of $7.35 with the same multiple, ISRG would have a fair value of $514. However, the price-to-sales ratio is significantly higher, so the valuation is mixed.

ISRG: A premium valuation but high growth

I’m looking for Alpha

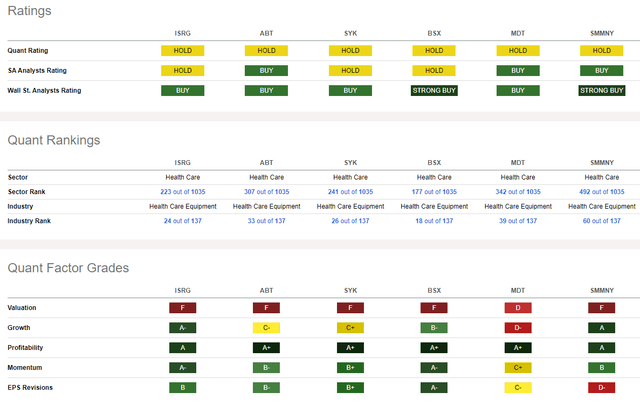

Compared to its competitorsISRG has a poor rating, although this is common in this high-growth industry. Therefore, the company’s growth rating is almost the best in class, while Profitability trends appear increasingly positive.

Also, the sales page is optimistic about ISRG, as evidenced by 18 earnings improvements in the last 90 days compared to only five downgrades. Finally, Share price dynamics was excellent and I will detail a positive technical chart later in the article.

Competitive analysis

I’m looking for Alpha

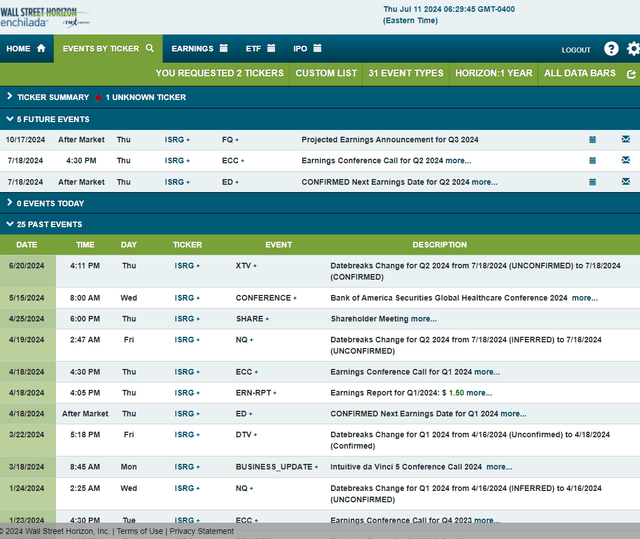

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed Q2 2024 earnings date on Thursday, July 18th for AMC with a conference call immediately following the release of the numbers. You can listen live hereThere are no further volatility catalysts visible on the calendar.

Risk calendar for corporate events

Wall Street Horizon

The technical view

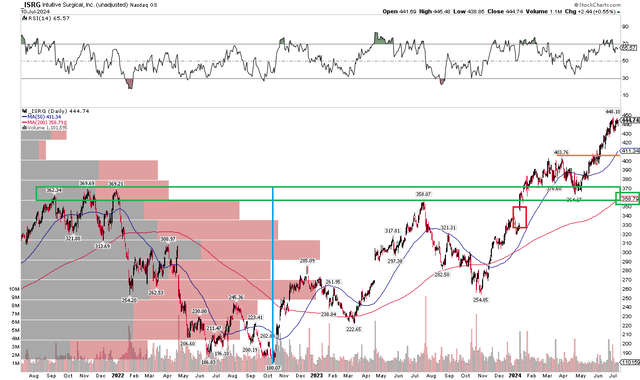

With strong revenue and earnings growth, a neutral rating, and momentum heading into earnings next week, ISRG’s technicals are excellent. Notice in the chart below that shares broke out above key resistance in the $364-$370 range. Once shares broke through this zone, a bullish upside target of $560 came into play based on the top of the $190 consolidation range that occurred from late 2021 to early 2024.

Also, look at how the stock tested this support area on a decline in April. The bulls did what they were supposed to do, buying up shares and helping push ISRG to new all-time highs in recent weeks. Now, with a rising long-term 200-day average and solid RSI momentum trends, the bulls control the major trend. Support is seen at $404 and below that at $364.

Overall, ISRG is currently a stock with top momentum on the market and appears technically strong.

ISRG: Shares break above $360, strong momentum trends

Stockcharts.com

The conclusion

I have a hold recommendation on ISRG. The valuation is high but fair in my view, while the technical outlook appears positive.

Temperatures in Death Valley could reach record levels: Current forecast

Famous intermittent fasting doctor disappears on vacation