Kraft Heinz with 5% yield: High value at a low price (NASDAQ:KHC)

")

Thin glass

introduction

A full hour.

That’s how long the average American has to work to afford a six-pack of beer and a burger. That’s an increase from 51 minutes in 2019.

Rabobank

These figures come from the Dutch Rabobank, which BBQ Index.

The latest results were released on June 26, showing that a barbecue for 10 people on the Fourth of July costs $99 – the highest amount ever. Beer, beef, soda and salad make up 64% of that cost.

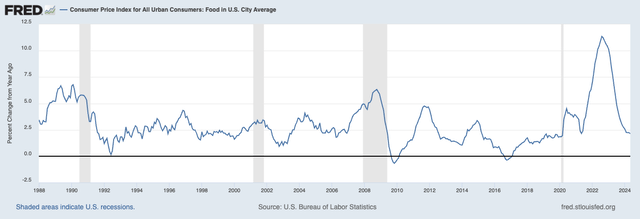

In general, food inflation is a big problem. Since 2019, total costs for consumers have increased by 25% – and there are additional headwinds.

As a result, Food inflation rose by 25% from 2019 to the end of 2023. But the additional inflation We saw more than that in the first half of 2024, albeit far more modest, was the turning pointMany consumers who have stayed the course despite 40-year highs in food prices, are now withdrawing and reassess their budgets. – Rabobank (emphasis added)

The quote above is key. While the inflation rate has fallen, prices have continued to rise – just at a slower rate.

Federal Reserve Bank of St. Louis

This is hurting stocks of consumer goods companies, especially those with low margins that face the threat of generic drugs.

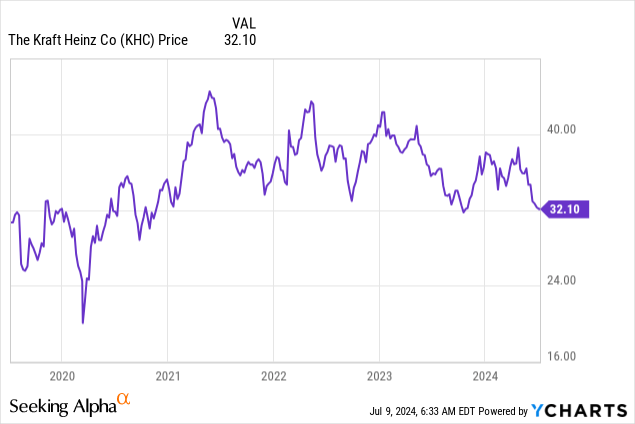

One of them is the Kraft Heinz Company (NASDAQ: KHC)a stock that I have reported on frequently in the last year.

My most recent article about the company was written on February 17 and was titled “Kraft Heinz remains undervalued with a yield of 4.6%.”

Since then, the undervaluation has narrowed even further, with the stock down 6 percent (including dividends), lagging the S&P 500’s return of 11.7 percent.

In this article, I update my thesis and explain why the company doesn’t seem to be taking a break – and what this could mean for its future.

So let’s get started!

A decent performance considering the headwind

Accordingly YouGovHeinz Ketchup is the 28th most popular brand in the United States. This is no surprise, as it is literally everywhere. It can be found in almost every home, restaurant, and place that serves food.

The product is also very popular beyond the country’s borders. Unfortunately, this does not protect Kraft Heinz from the extremely unfavorable economic environment.

One of the headwinds is market volatility as the company faces headwinds from a tight consumer environment and persistent inflation, mainly in commodities such as dairy, sweeteners and coffee.

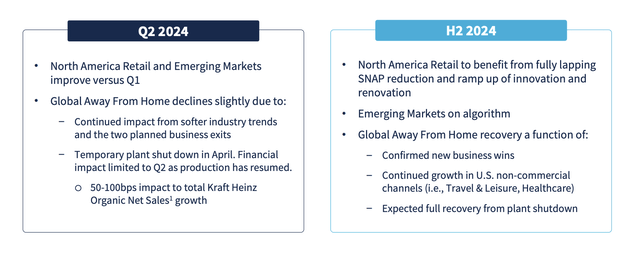

In addition, the company expects challenges in the US out-of-home segment due to weakening markets, particularly in the restaurant industry.

Despite market share gains in non-commercial channels, planned exits and operational disruptions, such as temporary plant closures, have impacted revenue growth expectations.

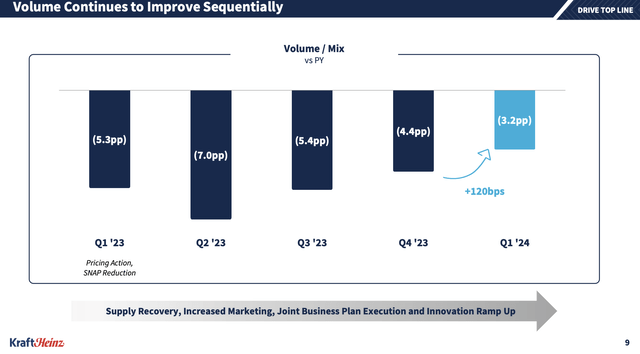

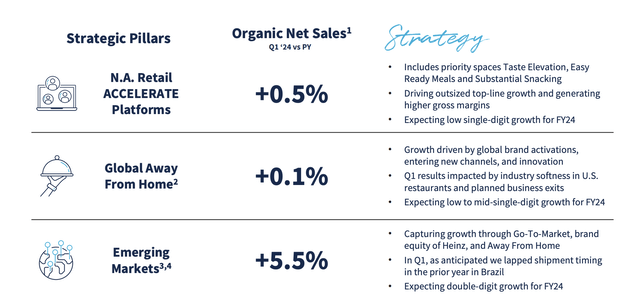

All in all, the volume/mix ratio remains deeply negative. While the 3.2% decline in Q1 2024 is less severe than the 4.4% decline in Q4 2023, the following numbers clearly show how difficult it is to grow in this environment.

The Kraft Heinz Company

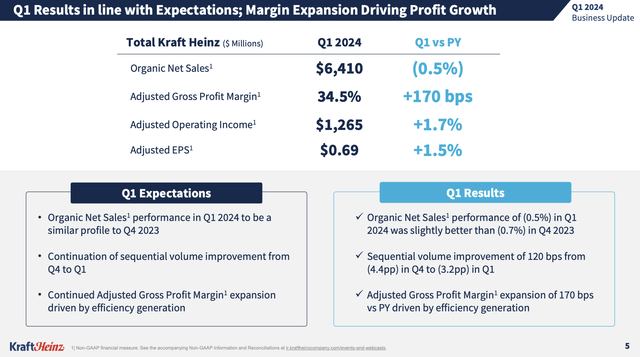

Despite a slight 0.5% decline in organic net sales, the company saw a significant improvement in adjusted gross profit margins, which increased by 170 basis points year-on-year, as pricing offset some volume weakness.

The Kraft Heinz Company

This enabled an increase in adjusted earnings per share of 1.5%.

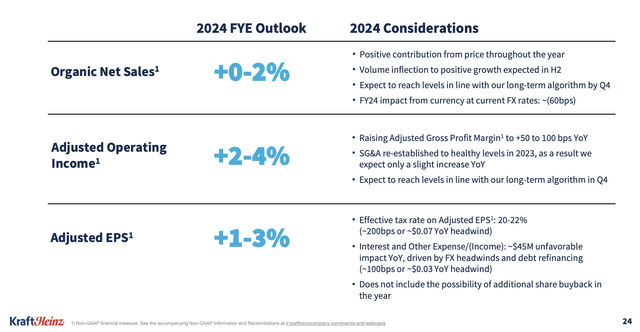

It also helps that the company has reiterated its guidance for 2024, expecting moderate organic net sales growth of between 0 and 2 percent and higher margins, which could potentially lead to adjusted operating profit growth of up to 4 percent.

The Kraft Heinz Company

In addition, the company raised its outlook for adjusted gross profit margin improvement to a range of 50 to 100 basis points. The previous range was 25 to 75 basis points.

According to the company, this adjustment reflects continued success in increasing efficiency and optimizing supply chain operations.

In addition, the Company expects stronger demand tailwinds (volume growth) in the second half of the year, supported by new business wins, non-commercial growth and a recovery from the above-mentioned plant closure.

The Kraft Heinz Company

This brings me to the next part of this article, creating value for shareholders.

How Kraft Heinz plans to create value for shareholders

During the dbAccess Global Consumer Conference last month, the company said it had increased its capital spending to 3 to 4 percent of its revenue and put more capital into areas such as marketing, research and development and technology.

Essentially, the company aims for a marketing investment ratio of around 4.5-5% and an R&D ratio of 1% to ensure sustainable innovation.

The Kraft Heinz Company

The company wants to drive innovation and remain more competitive in a demanding market.

A cornerstone of Kraft Heinz’s strategy is the Agile@Scale initiative, which uses digital tools and “agile methods” to drive innovation and efficiency.

The Kraft Heinz Company

The company argues that the success of these teams has made it a pioneer in the application of agile practices in the consumer goods industry.

Additionally, it leverages internal AI models and data-driven decision making powered by Microsoft (MSFT).

In addition, the company is increasingly focusing on emerging markets such as Brazil, Mexico, Indonesia and China. In the first quarter of 2024, these sales far exceeded those of other segments.

The Kraft Heinz Company

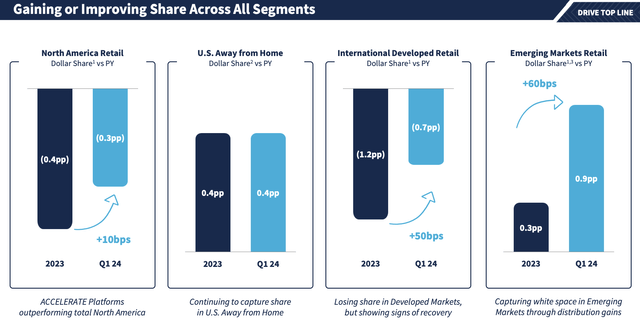

With a global penetration rate of just 19% for the Heinz brand, the company sees significant potential to increase its market share. In the first quarter, the company increased its market share in all segments, led by emerging market retail.

The Kraft Heinz Company

In addition, KHC is focusing on higher margin products. This makes sense as the low-price segment is in a difficult position given the increasing popularity of generics. Walmart (WMT), for example, is very successful in the generics business, as I explained in a recent article.

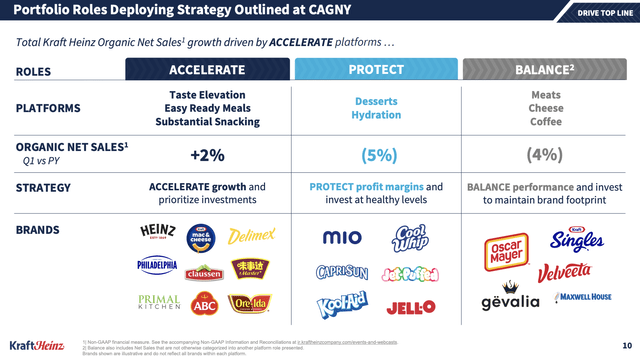

By divesting standardized and private label-focused businesses, Kraft Heinz has strengthened its core portfolio while focusing on its “improving taste quality” strategy.

The portfolio is now divided into three clear areas:

- Accelerate: High-growth categories such as sauces and ready meals.

- Protect: Stable business areas with high margins such as desserts and beverages.

- balance: Stable revenue generators such as meat, cheese and coffee.

The Kraft Heinz Company

Technically speaking, this all bodes well for shareholders.

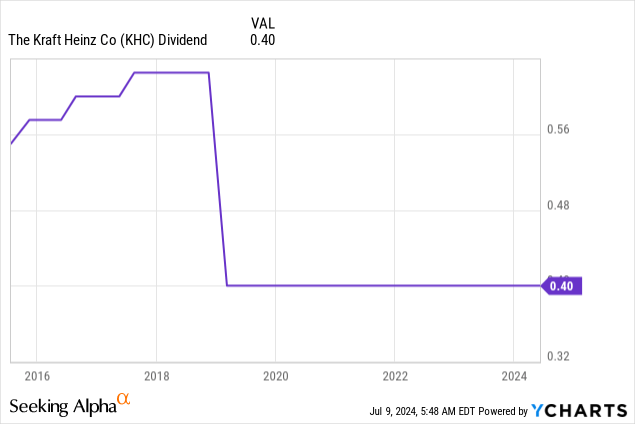

One advantage is that the company is focused on its balance sheet. In the first quarter, it paid out $636 million to shareholders while meeting its net leverage target of 3.0x EBITDA. It has an investment-grade credit rating of BBB.

Of that $636 million, $486 million was used for dividends. The company pays $0.40 per share per quarter, which is a yield of 5.0%. This dividend is protected by a payout ratio of 54%.

The bad news is that this dividend has not been increased for many years.

The good news is that the first signs are emerging.

For example, under a $3 billion buyback authorization, approximately $150 million was spent on buybacks (7.6% of the $39 billion market capitalization).

This buyback program was approved in December. It is the company’s first-ever buyback program and could mark the beginning of a long period of steadily increasing distributions to shareholders if the company can meet its targets.

Evaluation

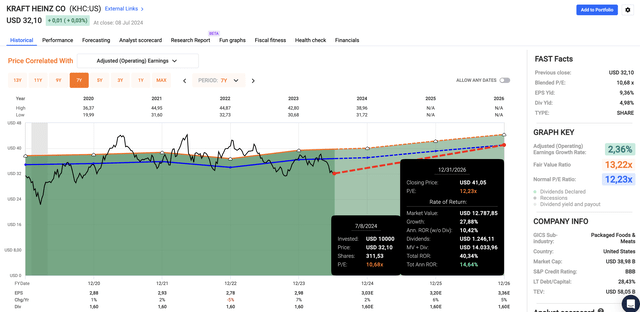

Kraft Heinz remains very cheap. After the recent share price decline, it now trades at a blended P/E of just 10.7, below its five-year average of 12.2.

I believe a multiple of 12.2 is fully justified. Based on the FactSet data in the chart below, the company is expected to grow its earnings per share by 5-6% annually after 2024.

FAST graphics

This would imply a fair price target of $41, 28% above the current price.

If we add the 5% return, the total return for the foreseeable future is at least 10%. At least in theory.

Unless consumer sentiment improves, I doubt that even a multiple of 12.2x will be justified, as investors seem to not care at all about consumer stocks in this environment.

While I’m not a fan of this industry, there is definitely long-term value. As I’ve said in previous articles, if I had an income-focused portfolio, I’d probably own some KHC shares as a long-term recovery/income investment with a great risk/reward ratio.

Bring away

In a difficult economic environment with persistent inflation and consumer caution, Kraft Heinz is facing significant headwinds.

However, despite a slight decline in organic sales, the company managed to improve adjusted gross profit margins and reaffirm its forecast for 2024.

With strategic initiatives such as Agile@Scale and a focus on higher-margin products, Kraft Heinz aims to drive innovation and increase shareholder value.

With an attractive valuation and a well-covered dividend yield of 5%, the company represents a potential opportunity for long-term investors looking for income and value.

All in all, Kraft Heinz remains a cautious but promising bet in an unpredictable market environment.

For and against

Advantages:

- Undervaluation: Kraft Heinz is trading at a historically low P/E ratio and therefore offers a potential (large) opportunity for value appreciation.

- Dividend yield: The stock offers a high dividend yield of 5%, which is attractive for income-oriented investors.

- Cost-cutting measures: Company initiatives such as Agile@Scale and supply chain optimization could lead to improved efficiency and higher margins.

- Market position: Despite all the challenges, Kraft Heinz maintains strong market positions with brands like Heinz and continues to innovate in high-margin categories.

Disadvantages:

- Sales challenges: The continued decline in organic sales and volume/mix remains a significant impediment to revenue growth.

- Raw material price pressure: Inflation in key commodities such as dairy products and sweeteners continues to squeeze margins.

- Consumer trends: Consumer preferences may continue to shift towards healthier alternatives and private labels.

- Execution risks: The success of recovery efforts depends on effective implementation in the face of a volatile market and operational disruptions.

The Boys and Girls Club honored 36 students for their work outside the classroom

This 2021 Mercedes-AMG GT Black Series with 165 miles is no ordinary grand tourer