Chimera Investment: Great value, extreme discount to book value (NYSE:CIM)

")

Editor’s note: Seeking Alpha is proud to welcome Value Op as a new contributing analyst. You can be one too! Share your best investment idea by submitting your article to our editors for review. Publish, earn money and unlock exclusive SA Premium access. Click here to learn more »

Christiantdk/iStock via Getty Images

The share of Chimera Investment (NYSE: CIM) started this year undervalued, and as the year has progressed, the stock price has continued to decline. However, this decline has not been reflected in the company’s book value, and Chimera’s book value has not only increased over the same period, but it has increased while the company has also paid healthy dividends of just over 10% annualized. Chimera’s economic yield in the first quarter of this year was 7% (about 31% annualized). Today, in early July, the stock’s price-to-book ratio is lower than it has ever been. times since the panic cry in 2020 at the start of the pandemic. It is well below the same ratios of its peers and seemingly for no good reason. This split between the company’s book value and market value cannot continue indefinitely. Therefore, I am trying to predict a bottom for this unsustainable trend.

| 01.07.24 Price to reported book value for Q1 2024 | |

| Chimera Investments (CIM) | 0.59 |

| Redwood Trust (RWT) | 0.73 |

| MFA Finance (MFA) | 0.73 |

| Two Ports (TWO) | 0.83 |

| Ellington Financial (EFC) | 0.86 |

| ARMOUR Residential REIT (ARR) | 0.87 |

| Dynex Capital (DX) | 0.89 |

| Annaly Capital (NLY) | 0.95 |

| AGNC Investment (AGNC) | 1.07 |

Repair loans

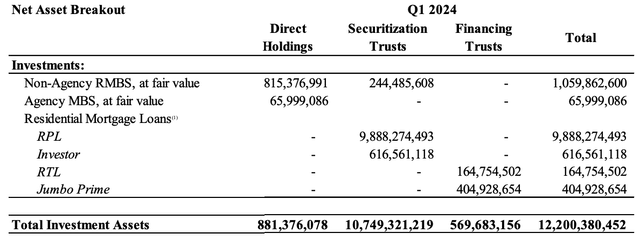

Chimera Investment Corporation is a mortgage REIT that invests almost exclusively in mortgage loans and mortgage-derived assets. Most of these loans are reperforming loans, which are loans that are often purchased at a discount and held directly on Chimera’s books. Chimera finances these loan purchases with a mix of secured and unsecured debt. In the past, Chimera had larger concentrations of non-agency RMBS and agency CMBS, but today these assets represent a much smaller portion of the overall portfolio.

Chimera Investment

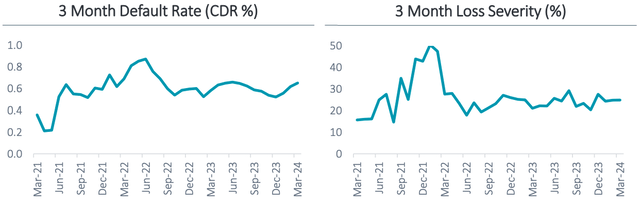

Despite the concerns some investors have about repair loans, they are actually a really good investment. Why? Because, like all mortgage loans, they have an established and publicly available performance history that is largely unaffected by correlated factors. And Chimera is open about the risk inherent in its own loan portfolio. Chimera characterizes and quantifies the risk of its loans using two statistics disclosed in its most recent investor presentation, both of which are standards for the industry: the conditional default rate and the loss given default, or “loss severity.”

Chimera Investment

To get a better idea of what these statistics mean for the overall portfolio, I would suggest some rough calculations that will hopefully be meaningful. If the average 3-month CDR is about 0.6%, that would mean an average annualized value of about 2.4%. And if that were combined with an average loss level of 25%, one could expect credit losses for the entire portfolio of about 0.6% per year. And if you multiply that by Chimera’s 3.7:1 leverage ratio, you could get the amount by which credit losses typically impact the common stock: maybe about 2.2% per year?

2.2% of loan losses attributable to common stock each year may seem like a lot, but it’s also important to remember that the underlying investments were likely originally purchased at a discount to offset that. Moreover, the underlying CDR and loss severity rates aren’t necessarily likely to increase in the future. The economy is strong. Home prices are higher than ever. There’s no apocalypse in sight, at least not in this space. Although Chimera has a very small portion (about 5%) of “agency CMBS” in its portfolio, that term actually refers to multifamily properties with more than 5 units, nothing we would normally consider commercial. From what I can see, Chimera’s portfolio doesn’t appear to have any of today’s truly risky assets: no office, no malls, no theaters, no brick-and-mortar retail, etc. In my opinion, the CDR and loss severity rates for residential mortgages tomorrow will most likely be pretty similar to what they are today, even for mortgages that are recovering.

Interest rate risk

The main risk Chimera has faced in recent years is not actually credit risk, but simply interest rate risk. 2022, the year in which the Fed accelerated its rate hikes, was certainly the worst in the last decade for Chimera:

Chimera does not list the reasons for portfolio losses in its 10-K filings, but only reports the fair value of its assets, with those fair values derived from the company’s own pricing models and validated by third-party pricing services. However, some confirmation of the reasons for the 2022 losses was provided in the Q1 2022 conference call, where management – again, my reading – indicated that about 75% of the quarter’s significant losses were caused by two-year and 10-year rate increases of about 160 basis points and 80 basis points, respectively, and the other 25% of the losses were due to increases in credit spreads. Of course, none of these metrics relate to actual credit losses: just because spreads are widening does not mean that credit losses will actually occur. It seems to me that none of this really reflects any real change in potential loan losses, and in fact, as seen in the CDR and loss severity charts, far from increasing in 2022, loan losses have actually normalized at this point. And now, after a year and a half, increased loan losses still have not materialized.

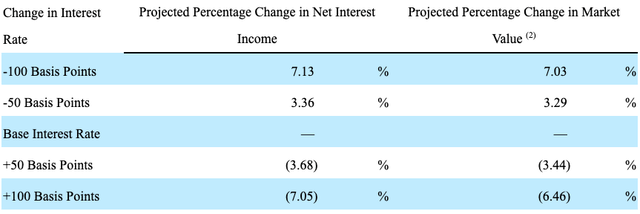

Chimera is also open about the significant interest rate risk in its portfolio. In its recent 10Q filing for Q1 2024, the company made this clear:

Chimera Investment

There is no doubt that CIM is an interest rate-sensitive stock. My own empirical calculations — which, in fairness, could contain significant errors — place CIM’s effective maturity at anywhere between 8 and 18 years versus the 10-year Treasury bond. One may question why, if CIM has hedged its convexity so expertly, hasn’t done the same for its maturity. Ultimately, I don’t know the answer; however, management noted in its most recent 10-K report that it is limited in its ability to hedge its portfolio because it must maintain its REIT status. Regardless, it is important to note that when 10-year rates rise, a certain amount of losses are to be expected. Likewise, however, declines in the 10-year rate should result in comparable increases in the value of Chimera’s loan book. From the table above, negative convexity does not appear to be as big a problem for Chimera as it is for some other mortgage servicers.

However, there is also reason to believe that significant increases in 10-year rates are simply unlikely. While the market is currently hyper-focused on when the Fed might next cut short-term rates, confidence is growing in the Fed’s ability to bring inflation down to acceptable levels over the long term. While it is not known exactly how long it will take for inflation to reach the 2% target, many are confident that rates do not need to remain this high indefinitely. Many people believe that Fed rate cuts will come. Some believe they are coming soon. In my opinion, the yield curve is inverted today not because of recession fears, but because many people simply believe that rates do not need to be as high in the future as they are now. I personally agree with this view, and this state of affairs is perfectly fine with CIM.

Risk factors

Although Chimera stock is severely undervalued and the company’s very low price-to-book ratio does not appear to reflect increased portfolio risk, that does not mean that buying CIM stock is completely risk-free. Ultimately, the reason the market has undervalued the stock recently is unclear, and one must accept the possibility that the market may continue to undervalue the stock in the near future, perhaps even more so. If the market perception of the stock continues to deteriorate, a purchase of CIM stock could become a value trap even without underperformance of book value. In this case, an investor could be forced to hold CIM stock for an undesirable period of time or sell at a loss before recouping their investment.

A second risk is that while most investors believe that interest rates could fall soon, they may not. Interest rates are notoriously difficult to predict, and near-term rate hikes are still possible despite what experts predict. A rise in the 10-year Treasury yield could lead to losses for CIM shares.

Diploma

Chimera’s stock is severely undervalued. The company’s very low price-to-book ratio does not appear to reflect increased portfolio risk, and therefore the stock looks like a very good buy. The reason the market is undervaluing the stock is unclear, and one must accept the possibility that the market will continue to undervalue the stock in the near future, perhaps even more. However, in the long term, rising stock performance seems very likely, as the low share price does not appear to reflect any underlying problems with Chimera’s loan portfolio.

Reading University waives one-word Ofsted rating following Ruth Perry’s death

New “The Penguin” poster gives a taste of Colin Farrell’s Dark Batman spin-off series – News about comic book adaptations and superhero films