Value Line stock remains less attractive than the risk-free alternative (NASDAQ:VALU)

")

PM Pictures

It’s been a little over six months since I published my “Avoid” article on Value Line Inc. (NASDAQ:VALU), and during that time the shares returned about 12.3% compared to a gain of about 16.6% for the S&P 500. I also think it would be fair to mention that the yield on the 10-year bond I recommended instead of stocks rose from 4.146% on the day my article was published to 4,284% now, so my alternative has underperformed the stock over the past half year. A lot has happened since then, including the release of some new financial results, so I thought I’d check the name again to see if it makes sense to buy it now. I’ll make that decision by looking at the relative valuation here and by looking at the alternatives available to investors. If you’re one of my regular clients, you know that the “alternative” I will be looking at is the 10-year risk-free bond.

We’re all busy. For example, I assume my readers are busy deciding between exotic vacations or which supermodel to take to dinner this weekend. Maybe they’re working late in the lab trying to uncover the mysteries of the universe. I’m also busy catching up on old episodes of The Young and the Restless. I’m embarrassed to report that the last thing I saw was Nick visiting Victor at the Newman Ranch. I don’t know why Victor is so cynical about Adam slipping back into the darkness while in the same breath recognizing that Adam has come a long way to better his life! That Victor Newman is a character I love to hate sometimes! Anyway, we’re all busy, that’s my point. That’s why I state a thesis at the very beginning of each of my articles to give investors a chance to quickly understand the core of my argument without getting lost in the details or correct spelling. You’re welcome. So I think 10-year Treasury notes still offer better value than this stock. For the equity investor to get the same cash flows as the 10-year Treasury note holder, the dividend would have to grow at a compound annual growth rate of over 11%. Given the factors I describe below, I think that’s very unlikely. Given that equity investors should demand higher returns than they get from notes given the risks present, the dividend would have to grow much more than 11% annually. In my view, that’s not going to happen. Therefore, any new capital should go into the 10-year Treasury note, which has a better-than-average chance of generating a nice capital gain if rates fall over the next few years. That ends my thesis. If you read on from here, that’s up to you.

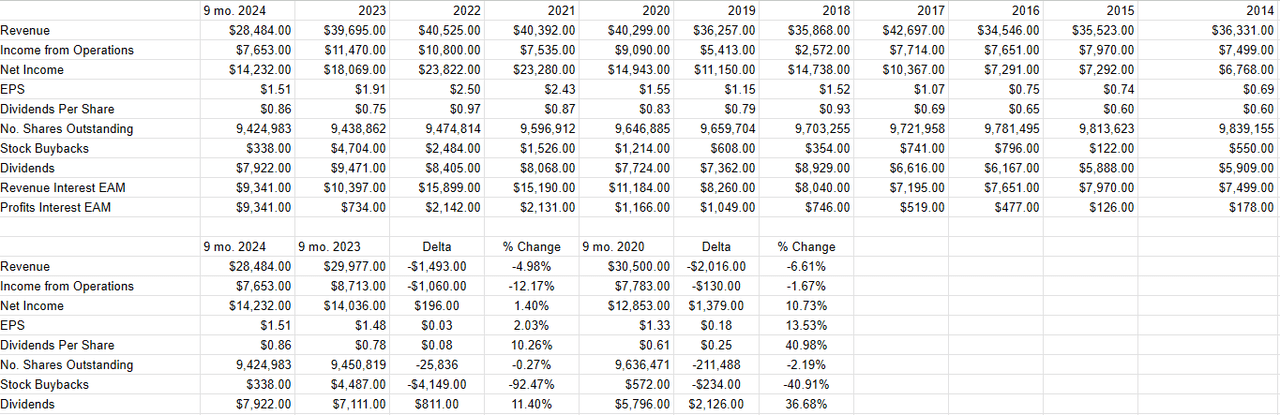

Financial Overview

I’ve written it before and will no doubt write it again. I believe this company is a low-growth cash cow and nothing about the recent financial results has changed my mind. While revenue fell about 5% compared to the same period last year, net profit actually rose about 1.4%, largely due to cost-cutting measures. For example, advertising and promotion expenses and office and administrative expenses each fell 4.8% compared to the same period last year.

The balance sheet remains rock solid in my view, with very liquid working capital of around $69.7 million against total liabilities of around $45.3 million. The balance sheet is one of the cleanest I’ve seen in a long time, which I think is significant given the widespread deterioration in capital structures that we’ve seen recently.

In my opinion, the dividend is the most important thing, and it has grown rapidly in recent years. For example, it is up about 41% compared to the same period in 2020, a growth rate that is as extraordinary as it is unsustainable in the long term. However, the payout ratio is only 56%, so there may still be room for dividend growth from current levels. Given the strength of the balance sheet and the fact that management has done a great job of rewarding investors with dividend increases, I would be willing to buy the shares if the relative valuation is attractive enough.

Value Line Finance (Value Line Investor Relations)

Relative rating

I come from a world where I believe risk-taking should be rewarded by a combination of lower valuations and higher return potential. The fact that higher return potential and lower valuations are two sides of the same coin makes things easier for me to understand. Since stocks are riskier than Treasuries, I will only buy them if they offer higher return potential than Treasuries. In addition, I believe one could credibly argue that Treasuries have the potential to increase in value because interest rates are likely to fall over the next few years.

With that in mind, I want to compare the cash flows an investor would receive from a dividend-paying stock and a 10-year Treasury bond. If the stock yields less than the bond, I want to answer the question: by how much does the dividend need to increase for the stock investor to receive identical cash flows as the bond investor. Given the risks present, the stock investor should demand more, but I first want to examine what growth is needed for the two assets to produce identical cash flows.

Value Line vs. Treasury Note Cash Flows (Author’s calculations)

I’ve answered that question and present it in the chart above, which I hope is both “practical” and “awesome.” In order for the stock investor to receive the same cash flows that the Treasury note investor is guaranteed over the next decade, the dividend must grow at a compound annual growth rate of about 11.25% for a decade. To put this in company-specific context, Value Line has managed to grow its dividend at an impressive compound annual growth rate of 6.6% since 2014.

Given this, and the fact that this is not a growth company and the payout ratio is already relatively high, I think the likelihood of an average annual dividend increase of more than 11% is slim.

Remember, this interest rate is simply the risk-free cash flows. We should expect higher payments from riskier stocks. Since investors should always look for the highest return with the least risk, they should avoid Value Line at its current price. The risk is too high and the return too low in my opinion. Although the return has increased somewhat since my last article on this name, I think it is wise to make the same trade again with new capital.

Rashida Jones befriends a robot in the Apple TV+ series

Michigan State Basketball is looking for an interesting guard for 2025