Energizer: Continuous value creation through debt repayment (NYSE:ENR)

")

ElementalImaging

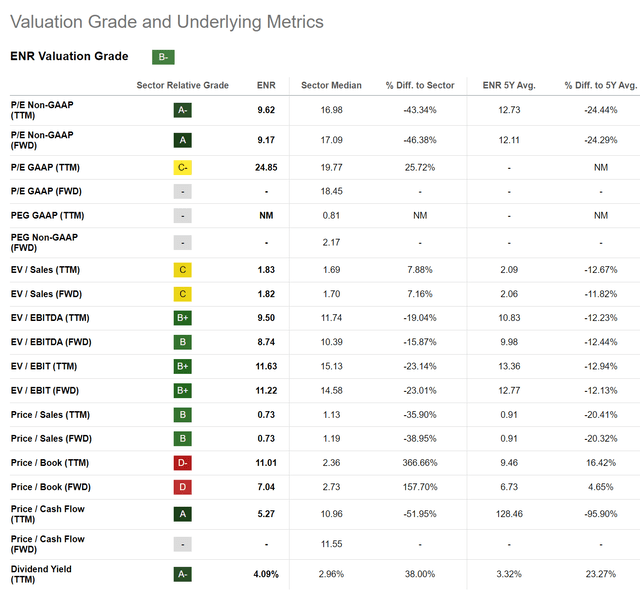

Recently I came across Energizer Holdings, Inc. (NYSE:ENR) when looking for cheap companies. ENR certainly meets the “cheap” condition, as the company trades at just a non-GAAP Fwd P/E of 9.2 and a dividend yield of 4.1% (Figure 1).

Figure 1 – ENR is trading at a favorable valuation (Search Alpha)

But is ENR a “value trap” or a “turnaround” candidate?

In my opinion, ENR is an interesting investment for patient investors. Provided the company can execute on its strategy of generating FCF and paying down debt, I see a total return potential of 60-100% for ENR shares.

The main risk for ENR is the company’s high debt load, which limits the company’s financial flexibility if the economy falters. I rate ENR as buy.

Company overview

Energizer Holdings is primarily responsible for the manufacture and sale of batteries and portable lighting products under the name Energy booster, ALWAYS READY, RayovacAnd VARTA brand names. ENR is also a leading developer and marketer of automotive cleaning and fragrance products under well-known brands such as A/C Pro, Armor All, Bahama & Co., California Scents and many others.

Energizer’s corporate history dates back to 1896, when WH Lawrence invented the first dry cell battery for personal use. The current version of the company was spun off from the Edgewell Personal Care Company (EPC) in 2015.

Unfortunate transaction burdened the company with excessive debt

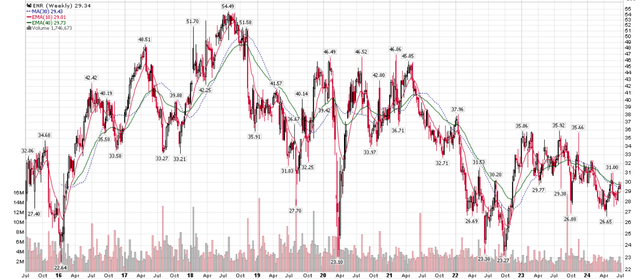

Energizer’s stock price peaked at approximately $55 per share in 2018 and has been on a downtrend for six years (Figure 2).

Figure 2 – ENR share price development (stockcharts.com)

The turning point in the company’s stock price appears to have been Energizer’s ill-fated 2019 acquisition of Spectrum Brands’ (SPB) Rayovac, VARTA, Armor All, STP and A/C Pro brands (announced in 2018) for $2 billion in cash. The transaction saddled ENR with more than $3 billion in long-term debt.

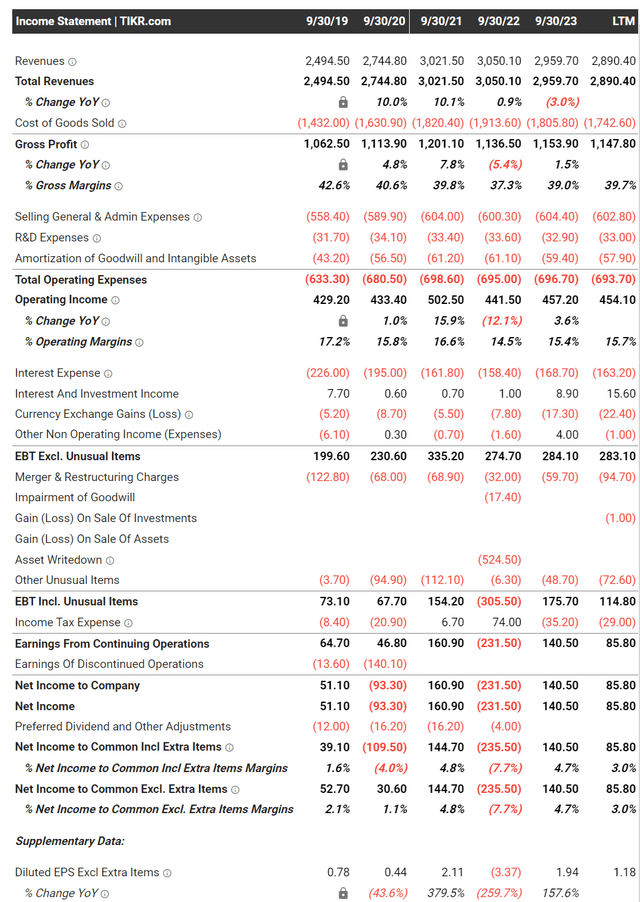

After over $1 billion in write-downs and restructuring charges over the past five fiscal years, Energizer shareholders do not appear to benefit much from the transaction, as the company earned $1.52 per share in fiscal 2018, compared to $1.18 over the past twelve months (Figure 3).

Figure 3 – ENR Financial Overview (tikr.com)

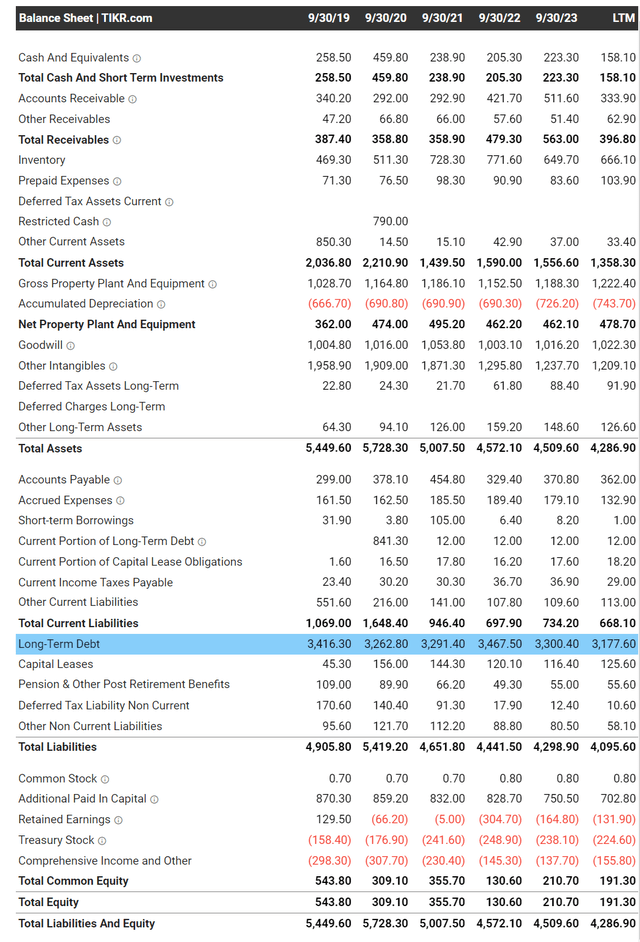

The company’s balance sheet also does not appear to show much progress, as Energizer still has $3.2 billion in long-term debt, compared to $3.4 billion at the end of fiscal 2019 (Figure 4).

Figure 4 – ENR balance sheet overview (tikr.com)

Is Energizer finally on the road to success?

However, selling disposable batteries to consumers seems to be a wonderful business in principle, as evidenced by Energizer’s operating margins of 15 to 17 percent and its low capital expenditure intensity.

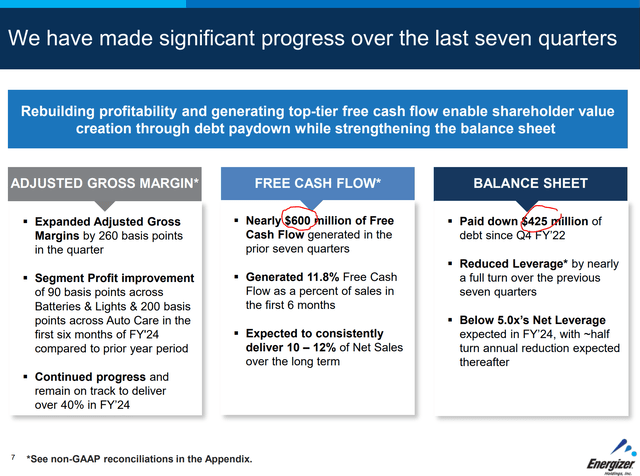

In fact, there is reason for hope, as the company reports generating nearly $600 million in free cash flow (“FCF”) and paying down $425 million in debt over the past seven quarters (Figure 5).

Figure 5 – ENR appears to be turning the tide (ENR investor presentation)

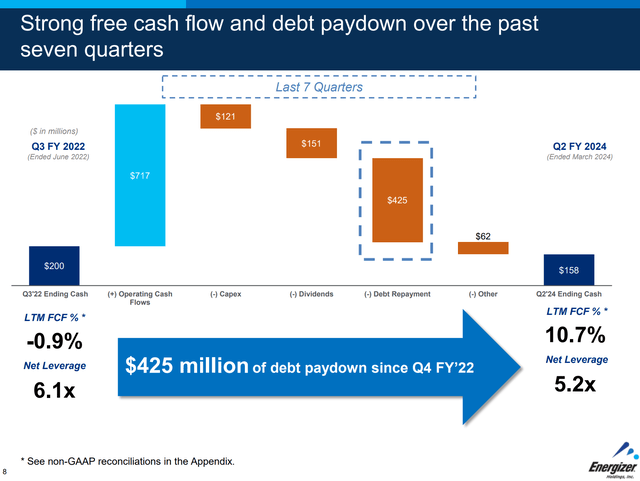

Since Q3/F22, management’s restructuring efforts have increased free cash flow from a negative FCF yield of 0.9% to 10.7% (Figure 6).

Figure 6 – ENR’s restructuring efforts are paying off (ENR investor presentation)

Looking ahead, management believes the company can consistently generate 10-12% of net sales as FCF. This should allow Energizer to rapidly reduce the company’s leverage, from 6.1x net debt/EBITDA in Q3 2022 to 5.2x currently and <5.0x by the end of fiscal 2024. Management believes it can reduce leverage by half a turn each year thereafter.

Path to continuous value creation

If we take management at its word, I believe shareholders have a clear chance of seeing their shares return 60% or more over the next few years.

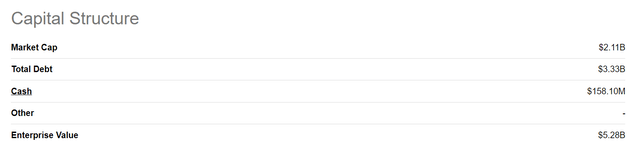

In Figure 1 above, we see that Energizer is currently valued at 8.7x Fwd EV/EBITDA. At the same time, we see that ENR’s balance sheet is highly leveraged with $3.3 billion in debt and outstanding leases (Figure 7).

Figure 7 – ENR’s enterprise value is highly leveraged (Search Alpha)

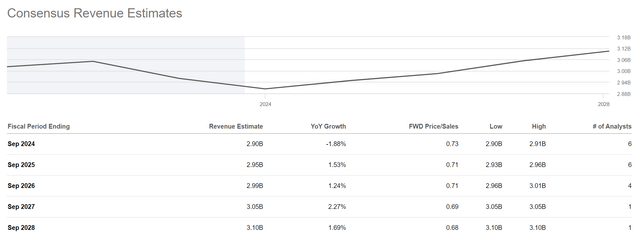

Assuming the company can generate 10% of net sales as FCF, this equates to approximately $300 million in FCF annually for the next 5 years (Figure 8). If all of ENR’s FCF goes to paying down debt, I estimate Energizer’s debt level at the end of 2028 will be approximately $2.0 billion ($3.3 billion less $1.35 billion in FCF).

Figure 8 – ENR revenue estimates (Search Alpha)

If we assume that Energizer’s valuation remains unchanged at an enterprise value of $5.3 billion, this means that the company’s equity should be worth $3.5 billion at the end of 2028 ($5.3 billion EV – $2.0 billion debt + $160 million cash), up 65%.

Furthermore, we can see that Energizer is currently undervalued compared to its peers in the consumer staples sector, which trade at an average multiple of 10.4x Fwd EV/EBITDA. This is most likely due to the company’s poor balance sheet and poor growth prospects.

If Energizer can reduce its debt overhang, ENR’s valuation multiple can be expected to increase. Assuming a modest increase in ENR’s valuation multiple to 9.4x Fwd EV/EBITDA (still a discount to peers due to slower growth), ENR’s equity could be worth $3.8 billion (9.4 x $600 million EBITDA – $2.0 billion debt + $160 million cash), or 80% upside.

Finally, Energizer should be able to easily pay out its 4.1% dividend yield if it can generate the expected FCF value. Assuming management can execute on its plans, patient investors can expect a total return of 60-100% on their investment in ENR stock over the next few years.

Risks for ENR

While I have laid out an optimistic scenario above that provides shareholders with returns of 60-100% on ENR shares over the next few years, there are risks that must also be considered.

First, investors are relying on management to stay true to its strategy and continue to de-stress ENR’s balance sheet rather than pursuing illegitimate M&A transactions. Readers are reminded that ENR’s current CEO, Mark Lavigne, was Energizer’s general counsel prior to his current appointment in 2021 and thus, as an Energizer executive, led the disastrous Spectrum transaction. Once Energizer’s debt is reduced, he could return to empire-building mode and pursue another value-destroying acquisition.

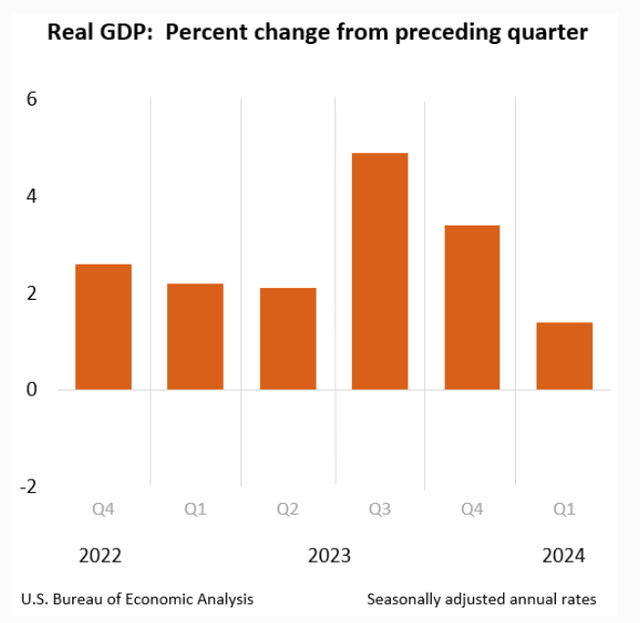

Another risk for Energizer concerns the US economy. The optimistic scenario above assumes that the economy remains stable over the next five years and there are no major shocks. This could be wishful thinking, as economic growth has slowed significantly in recent quarters (Figure 9). If the economy goes into recession, Energizer’s revenues could be negatively affected.

Figure 9 – Economic growth has slowed (BEA)

While batteries are considered a staple and are likely to remain in demand even in a recession, this is not the case for car care products. When consumers are financially strained, they can save on essentials such as ArmorAll or Californian fragrances.

Diploma

In my opinion, Energizer Holdings could represent an interesting opportunity for patient investors. Provided the company can execute on its strategy of operating its business with sufficient cash flows to pay off debt, shareholders could receive a total return of 60-100% over the next five years.

The risk for Energizer, however, is the company’s high debt load, which limits the company’s financial flexibility if the economy falters. When weighing the rewards against the risks, I believe Energizer’s cheap valuation is a buy Evaluation.

NWA EDITORIAL | Federal authorities should return woman accused in death of mother and baby to Benton County for arraignment

Fidelity and Sygnum sign agreement with Chainlink to transform tokenized asset data