Arbor Realty: 12.1% yield, 91% payout ratio, rising book value (NYSE:ABR)

")

Dragon Claws

Arbor Realty Trust, Inc. (NYSE: ABR) is a well-managed real estate investment trust focused on mortgage investments, particularly in the multifamily sector.

The trust provides loans and services to the single-family and multi-family housing industries and also owns other commercial real estate assets.

What makes Arbor Realty Trust an attractive income-oriented investment for passive income investors is the trust’s dividend of $0.43 per share per quarter, which has been consistently covered by distributable earnings over the past year, as well as the consistent growth in the trust’s book value per share.

I think Arbor Realty Trust offers a high-quality 12.1% yield that passive income investors will find hard to resist.

My rating history

My last stock rating for Arbor Realty Trust was Strong Buy because I thought the mortgage real estate fund’s multifamily investments The trust is a unique investment instrument in the mortgage market.

Arbor Realty Trust has avoided dividend cuts in its recent history, which is not something you can say about every mortgage fund. I think the 12% yield is reasonably safe and the fund’s overfunding provides an additional cushion for the dividend.

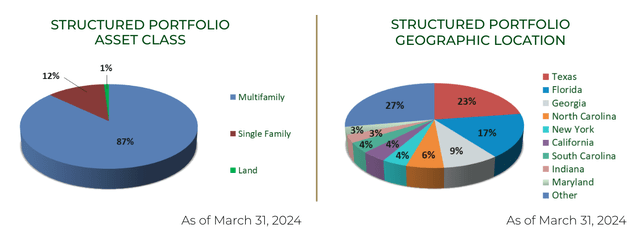

Portfolio allocation

Arbor Realty Trust’s business consists of two parts. The main part, the structured business, consists of investments in the multifamily, single-family rental and commercial real estate markets. Most of these are multifamily loans of various types (bridge loans, mezzanine loans), but the trust also invests in other mortgage-related securities.

The agency business, the second pillar of Arbor Realty Trust’s investments, is engaged in the sale and servicing of multifamily loan products, such as through government-sponsored enterprises Fannie Mae and Freddie Mac. Multifamily assets made up the majority of the Trust’s structured portfolio (87%) and balance sheet as of March 31, 2024.

Portfolio Breakdown (Arbor Realty Trust)

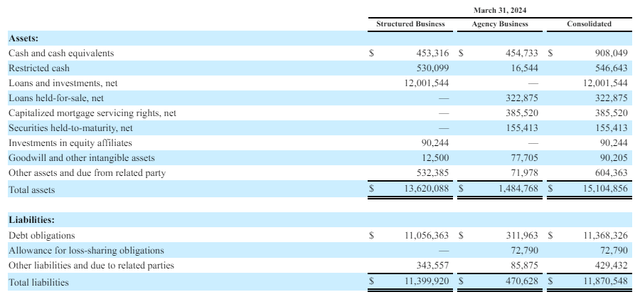

The structured business held a whopping 90% of assets, or $13.2 billion, as of March 31, 2024. Overall, the mortgage fund owned $15.1 billion in assets, down 4% from the previous quarter due to loan sales.

Summary of Assets and Liabilities (Arbor Realty Trust)

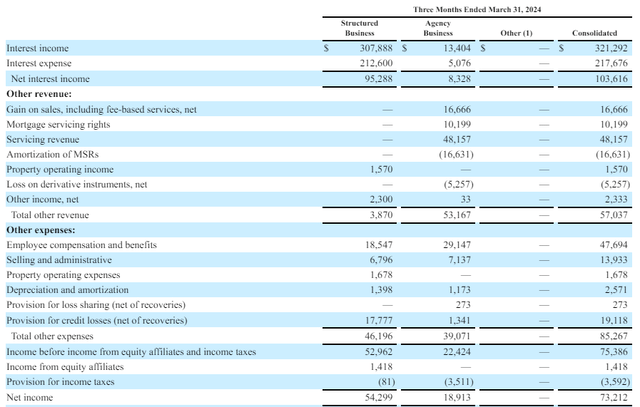

Arbor Realty Trust’s assets generate a steady stream of income for the mortgage trust: In Q1 2024, the mortgage real estate investment trust generated $103.6 million in net interest income, the trust’s primary source of income passed on to unitholders, a 5% year-over-year decrease primarily due to loan sales.

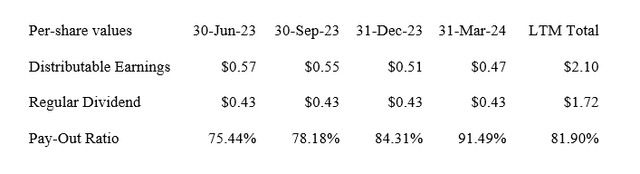

The most important thing for a mortgage fund like Arbor Realty Trust is to generate its dividend from distributable income, and the fund has had no problems doing so so far.

Revenue (Arbor Realty Trust)

Well covered 12% return

Arbor Realty Trust earned more from distributable earnings than its dividend both in the first quarter and last year. The trust’s portfolio assets produced distributable earnings of $0.47 per share in the first quarter, giving it a dividend payout ratio of 91.5%.

Excluding a realized loss of $1.6 million on a non-performing loan, Arbor Realty Trust had adjusted distributable earnings of $0.48 per share and a dividend payout ratio of 89.6%.

Over the last twelve months, Arbor Realty Trust paid out just 81.90% of its distributable earnings (unadjusted), meaning the mortgage fund offers passive income investors a very well-covered 12% yield.

The industry’s largest mortgage real estate investment fund, Annaly Capital Management, Inc. (NLY) 90.6% of distributable profits have been paid out, giving Arbor Realty Trust a better margin of safety than the industry’s heavyweights.

Distributable profits (table created by author using trust information)

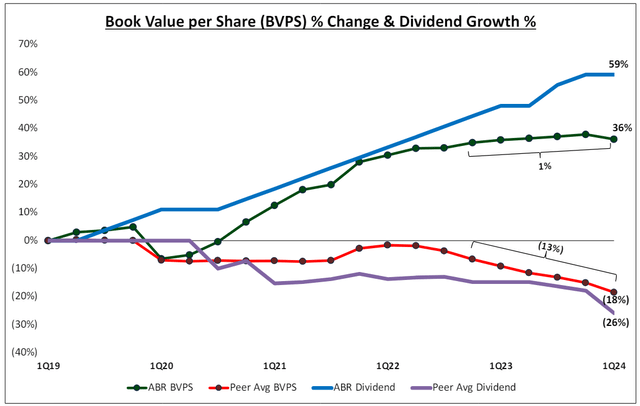

Book value growth and multiplier

Arbor Realty offers passive income investors a differentiated value proposition through its ability to grow its book value even in difficult markets.

The Mortgage Real Estate Investment Trust has increased both its book value and its dividend since the first quarter of 2019 and has significantly outperformed its competitors in the mortgage loan fund space.

Arbor Realty had a GAAP book value of $13.02 (my intrinsic value estimate) as of March 31, 2024, which was 36% higher than in Q1 2019.

Book value per share (Arbor Realty Trust)

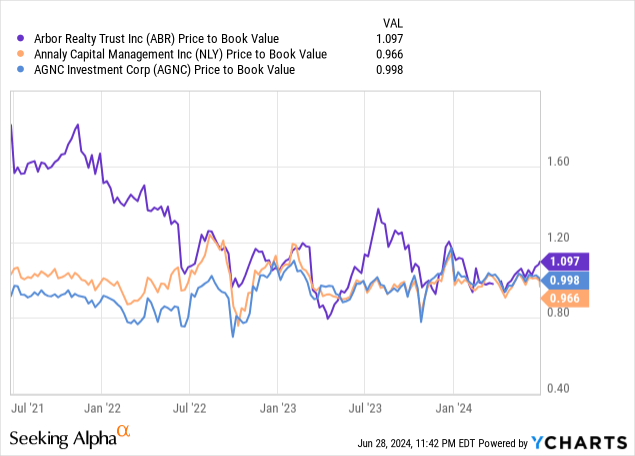

Passive income investors currently pay a 9% premium for the opportunity to invest in Arbor Realty Trust’s business. Other mortgage real estate investment trusts with large agency investment approaches such as Annaly Capital Management and AGNC Investment Corp. (AGNC) are sold at a book value multiple of 1.0.

Because both Annaly and AGNC own large portfolios of interest-rate-sensitive mortgage-backed securities, their shares came under selling and valuation pressure after the central bank said in June that it would now consider only one cut in short-term interest rates, instead of the previously possible three.

The fact that Arbor Realty Trust is selling at a higher price than book value is due to the trust’s lower focus on interest rate-sensitive mortgage-backed securities, a solid dividend payout ratio, and its ability to grow its book value per share over time.

Why an investment in Arbor Realty Trust may underperform

Arbor Realty Trust focuses on multifamily properties, so it could take a severe hit if the multifamily sector were to be hit by either higher interest rates or a wave of credit problems. If more borrowers are unable to make their multifamily payments, Arbor Realty Trust would likely take a severe hit to its earnings and book value.

Higher interest rates or a correction in the US real estate market could be a catalyst for such a scenario.

My conclusion

Three things stand out about Arbor Realty Trust:

- The Mortgage Real Estate Investment Trust focuses on multifamily investments, which distinguishes it from other mortgage trusts that are overly invested in agency MBS;

- Arbor Realty Trust’s dividend is well covered by distributable earnings and has been so consistently over the last twelve months;

- The trust was able to avoid the problems of other mortgage trusts that are more focused on agency mortgage-backed securities, allowing it to increase its book value per share, resulting in a higher book value multiple.

In my opinion, passive income investors have the opportunity to earn a solid 12.1% return from a differentiated mortgage trust.

I think the trust’s track record, particularly in book value growth, is a strong reason to overweight ABR. I’ve made Arbor Realty Trust a core holding in my passive income portfolio with a 3% weighting.

Jared Padalecki reveals the story of the 5th season of “Walker” after the series finale

Katy Perry wears a long dress with lyrics to an unreleased song