VF Corporation: Turnaround successes should not be taken at face value (NYSE:VFC)

")

Subscribe to

VF Corporation (NYSE: VFC) sells branded clothing, shoes and accessories under a portfolio of brands. The brands include large, globally known names such as The North Face, Vans, Timberland and Dickies, but also smaller brands such as Icebreaker, Napapijri, JanSport and Supreme, which was acquired in 2020 for $2.1 billion.

The stock has lost most of its value from 2021 as VFC’s poor brand management and expensive M&A strategy have led to high debt and poorly performing brands. A comprehensive turnaround plan is underway, but no impact was yet seen in the fourth quarter as revenue fell by -13.4%.

Ten-year stock chart (Search Alpha)

VFC’s weak brand performance is not yet in sight

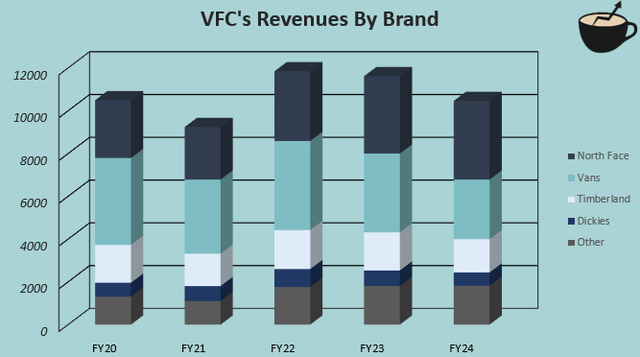

VFC has recently seen weak growth from many of the company’s key brands. Vans, VFC’s largest brand through fiscal 2024, reported a decline in revenue of $4,063.4 million in fiscal 2020.before the major problems with the Covid pandemic to only 2785.7 million US dollars in the 2024 financial year at a compound annual growth rate of -9.0%. Timberland, the third largest VFC brand, recorded a compound annual growth rate of -3.1% over the same period, followed by Dickies with a compound annual growth rate of -1.1%. It seems that the company is unable to adapt to changing customer demand with many stagnant brands.

The 2020 acquisition of Supreme is also an example of VFC’s history of poorly managed brands. The brand contributed around $500 million to VFC’s revenue in fiscal 2022, with ambitious plans to drive growth to $1 billion through new stores, brand collaborations, and global expansion with VFC’s large global distribution network. With Google Trends showing stable global search term volume for Supreme, the company recorded goodwill and intangible asset impairments totaling $735 million in fiscal 2023 and an additional $313.1 million in fiscal 2024 due to the brand’s weak performance. VFC is now reportedly considering selling the business.

Author’s calculation using VFC’s 10-K filing data

The North Face brand is VFC’s outlier, as the stagnant brand image from FY2014 to FY2017 has been transformed into an impressive 8.0% compound annual growth rate from FY2020 to FY2024 as the company has become VFC’s largest brand. However, the rapid growth of the top-performing brand has also started to stagnate, with -5.3% YoY sales in Q4 and 1.7% growth for the whole of FY2024. Total sales growth in Q4 was -13.4%, representing one of VFC’s sharpest sales declines in recent history.

The weak revenue performance has ultimately led to declining margins, as operating margins were only 6.0% in fiscal 2024, after a long-term double-digit growth and an average of 11.4% from 2016 to 2020. Further declines also pose a similar threat, as SG&A expenses rise with inflation and failed growth initiatives while gross profits fall.

Don’t take the success of a “Reinvent” turnaround plan at face value

To counteract the poor performance, VFC introduced the turnaround plan “Reinvent” in the Q2/FY2024 report press release. The plan was presented by Bracken Darrell, VFC’s new CEO who was appointed a few months before the plan was announced.

As part of the plan, VFC aims to improve results in North America by changing its operating model, transform the Vans brand by appointing a new brand president, reduce fixed costs by $300 million and reduce debt. These changes reflect a fundamental shift in VFC’s strategy and place a clear focus on transforming Vans.

The $300 million fixed cost reduction looks to be a big profit driver if successfully implemented without degrading company performance. However, a brand turnaround is needed to maintain the company’s profits as margins are continually suffering from lower sales, exacerbated by VFC’s nearly $6 billion in interest-bearing debt.

I don’t think the Reinvent Plan’s turnaround targets should be taken at face value until the brands’ performance is better documented – a turnaround plan for Vans was already presented at the 2022 Investor Day for Vans, as was previously presented for The North Face. Yet several quarters later, the Vans brand has not even experienced stabilization. Communicated growth targets for Timberland and Dickies were also missed, and sales have continued to decline.

The plan is now more comprehensive than the one unveiled at Investor Day 2022, especially with Bracken Darrell appointed as the new CEO to lead a transformation at the company. Bracken Darrell has an impressive resume: He was previously CEO of Logitech International (LOGI) and worked in senior roles at Procter & Gamble (PG), Whirlpool (WHR), and General Electric (GE). Still, leading fashion brands can be challenging, as maintaining and creating demand requires deep, constant customer and trend knowledge—while the new CEO is being praised for the turnaround of the Old Spice brand, a similar turnaround at Vans could be more challenging and likely require a different type of brand strategy.

The trend continues to show no signs of improvement. Vans sales fell by -26.3% in the fourth quarter, The North Face by -5.3%, Timberland by -13.7% and Dickies by -15.2%. Other brands remained almost stable with slight declines. The search term Vans continues to show weakness on Google Trends.

Just recently, in February, VFC announced that it was conducting a strategic portfolio review and may now be looking to sell many of its smaller brands. The review could create upside potential, but no sales have been announced so far.

The stock valuation prices in too many improvements

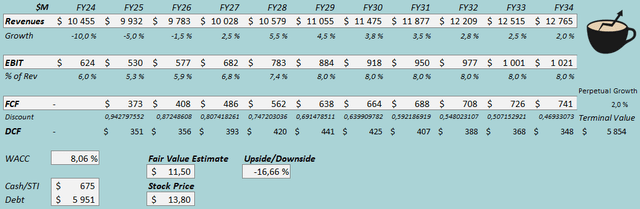

I’ve created a discounted cash flow (DCF) model to determine an approximate fair value for the stock. In the model, I factor in a semi-successful turnaround that leads to higher margins than currently, but not quite at long-term levels.

For revenue, I expect a decline of -5% in fiscal 2025, a decline of -1.5% in fiscal 2026, but a return to better performance from fiscal 2027 onwards. From fiscal 2026 to fiscal 2034, I estimate the average annual revenue growth rate at 3.4%, after which growth stops at a constant 2%.

Since VFC is targeting $300 million in cost savings and I expect higher revenues after a few years, I expect the EBIT margin to increase from 5.3% in fiscal 2025 to 8.0% eventually. The company has quite low capital expenditure and additional working capital needs, so the cash flow conversion is quite good.

DCF model (Author’s calculation)

VFC’s fair value is estimated at $11.50, 17% below the stock price at the time of writing. Even though Reinvent’s turnaround plan shows many improvements, the stock seems slightly overvalued. Good upside potential seems to require a nearly complete brand turnaround, which I don’t think investors should expect just yet.

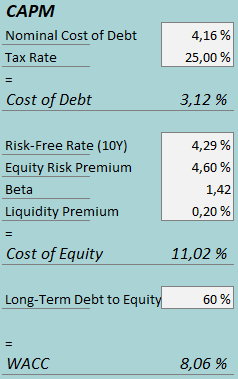

The DCF model uses a weighted average cost of capital of 8.06%. The WACC used is derived from a capital asset pricing model:

CAPM (Author’s calculation)

In the fourth quarter, VFC had interest expense of $61.8 million, so the company’s interest rate at the current level of interest-bearing debt is 4.16%. I estimate the long-term debt ratio at 60% due to VFC’s continued leveraged balance sheet but plans to deleverage. I believe refinancing debt now would likely result in a higher interest rate, which poses a moderate risk to the cost of capital.

To estimate the cost of equity, I use the 10-year US bond yield of 4.29% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s most recent estimate for the United States, updated on 5 June 2016.th January. Seeking Alpha estimates VFC’s beta at 1.42. Finally, I add a liquidity premium of 0.2%, which gives a cost of equity of 11.02% and a WACC of 8.06%.

Significant upside risk

The bearish thesis still carries a large upside risk – if Vans’ turnaround proves very successful, an increase in long-term margins and better growth could make the stock undervalued at the current price. With an average operating margin of 11.4% in fiscal 2016-2020, the DCF model would estimate an upside potential of 65% from fiscal 2027. Nevertheless, signs of such a turnaround are not yet in sight, and such a scenario should not be considered likely yet.

Additionally, the review of strategic alternatives could provide upside potential if VFC is able to sell well-known brands at a good price – the Timberland, Dickies and Supreme brands could be good choices for VFC if a potential buyer has more confidence in the leadership of those brands. Speculation about potential sales is increasing and in my opinion a sale of one or more of VFC’s brands is likely at some point. However, valuation in potential sales could be disappointing; sales are not a sure way to create upside.

I urge investors to closely monitor the brand’s performance in the coming quarters, as a complete turnaround could still be of great value to shareholders.

Bring away

VFC’s new CEO has launched a major turnaround plan to improve its underperforming brands. Costs are to be cut dramatically and Vans is to perform better through a leadership change and operational changes. However, investors should not believe in a near-complete turnaround just yet – a Vans turnaround has been attempted for some time and Bracken Darrell does not have much experience running fashion brands, which could still prove challenging. Q4 performance also continues to show weakness across all brands, with even The North Face now showing weakness after a previous turnaround. Valuation seems to assume good improvements as a base case, which I doubt for now. While brand sales or a turnaround could provide great upside, the risk-reward ratio does not seem good and I am starting with a sell for VF Corporation.

“Take your grandparents to camp” day 2024

Idaho Talking Book Service launches new website