CK Hutchison: Value trap with 7% yield, but we bought some (OTCMKTS:CKHUY)

")

Nikada/E+ via Getty Images

Note: All monetary amounts are in Hong Kong dollars unless otherwise stated.

The conglomerate

Hong Kong-based conglomerate CK Hutchison Holdings Limited (OTCPK:CKHUY) has a presence in 50 countries and operates four business segments.

The companies

In Search of Alpha – Getty Images

Ports and related services: CKHUY operates 53 ports in 24 countries and also provides related services such as distribution centers, ship repair facilities, and cargo and container handling, to name a few. The reach of this business extends across Asia, the Middle East, Africa, Europe, the Americas and Australasia. This segment is characterized by the world’s leading port network.

In Search of Alpha – Getty Images

Retail trade: CKHUY subsidiary AS Watson Group is the world’s largest retailer of health and beauty products. It is present in 28 markets and has a portfolio that includes health and beauty products, supermarkets, consumer electronics, electrical appliance chains, beverages and luxury perfumeries. This segment is operating in Hong Kong and mainland China, Asia and Europe.

In Search of Alpha – Getty Images

Infrastructure: CKHUY invests in energy, water transport and domestic infrastructure. It is also involved in waste management, waste-to-energy and other infrastructure-related businesses. This arm operates in Hong Kong and Mainland China, the UK, Europe, Australasia and North America. CKHUY is present in these diverse businesses through its majority shareholding in CK Infrastructure Holdings Limited, a global operator in this field.

In Search of Alpha – Getty Images

Telecommunications: CKHUY serves the cellular and Wi-Fi needs of over 175 million customers in Europe, Asia and domestically.

But wait, there’s more:

CKHUY Website

These investments give CKHUY access to various business areas including, but not limited to, aircraft management, maintenance and design, manufacturing and sales of household and industrial products, logistics services, biopharmaceuticals and e-commerce. A special thanks goes to CKHUY’s 16.69% stake in Cenovus Energy Inc. (CVE), one of our personal investments that we have also covered a few times on this platform. Our last public review was in December of last year.

The Value Trap Diagram

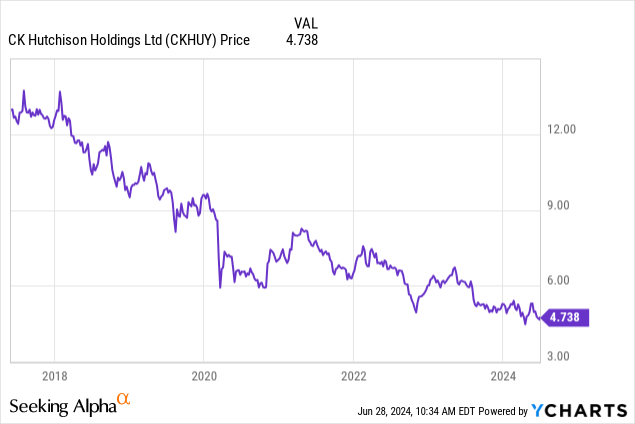

Since it is a conglomerate with a long history, the first thing that is noticeable about the share price is the drop.

Above is the OTC chart, but the one in Hong Kong dollars, going back to 2000, isn’t exactly inspiring either.

Google Finance

While management has made some poor decisions, this is at least partially a value impairment. Let’s look at this and see why we bought some today.

Annual figures 2023 (all in HKD)

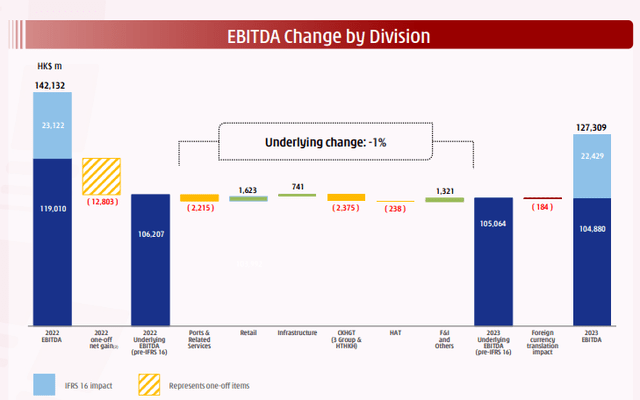

We start with their EBITDA and its change in 2023. This remained relatively stable in infrastructure, retail and financials, investments and others, offsetting declines in ports and related services. You can see the dance around IFRS 16, a change in accounting standards related to leases.

CKHUY March 2024 Presentation

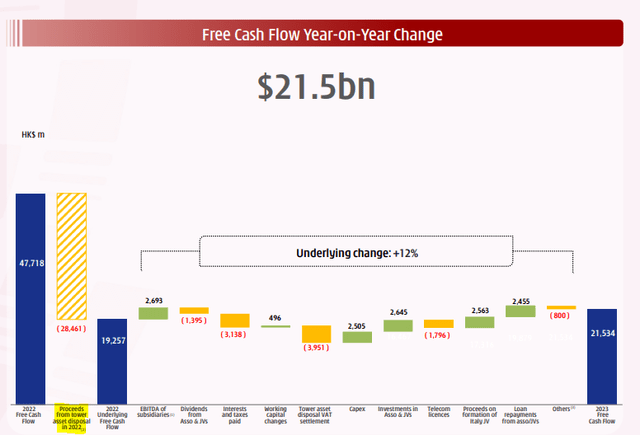

Next we come to free cash flow. There are two things to note here. First, there is a large delta in these numbers due to the impact of IFRS 16. Second, there is a large impact from the disposal of the towers, which has skewed the 2022 numbers upwards.

CKHUY March 2024 Presentation

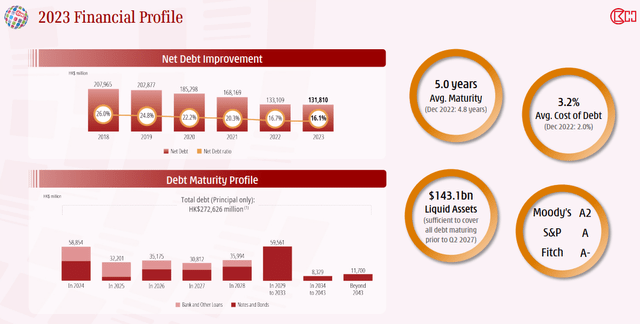

What we can see is that underlying free cash flow is up 12% year over year after these adjustments. There is nothing here that even remotely suggests there is any kind of trouble. What has CKHUY done with all this cash inflow? It has continued to reduce its debt and further strengthen its already strong balance sheet.

CKHUY March 2024 Presentation

There were some corresponding comments on this from a previous earnings Call that was also interesting.

Healthy free cash flow profiles typically lead to pretty healthy financial profiles, like the one on Slide 11. The first and most obvious positive development was the very significant reduction in our net debt relative to net total capital position, which I talked about, but I didn’t talk about how much gross debt was reduced. And that addresses the impact of rising interest rates, right, and it also addresses managing refinancing risks and so on. So we actually reduced gross debt by $41.7 billion while reducing net debt by $35 billion. So this is the year where I think gross debt reduction is important. So that $284.6 billion is literally $41.7 billion less than at the end of 2021.

Source: Transcript of the CKHUY conference

Although the company has increased its dividend, it remains a low percentage of free cash flow and a low percentage of earnings (around 40%).

Our earnings per share, of course, are the same 10%, and our dividend, as we just announced, will be increased by the same 10%, which is consistent with our 2015 promises to keep our payout ratio stable and increase dividends as earnings and the knock-on effects increase. But fortunately, we had a very healthy increase in earnings and an increase in dividends for 2022.

Source: Transcript of the CKHUY conference

Rating & Verdict

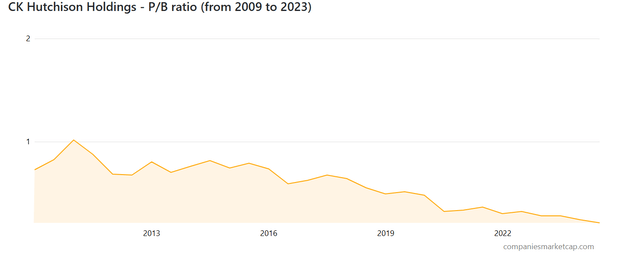

Here is the price-to-book chart from 2009. The stock was once trading at book value and is now at one-fifth of that value.

Market capitalization of companies

The stock is trading at a P/E ratio of just under 6.0. The dividend yield is 6.8% with a payout ratio of 40%. It is quite rare to get such values from a company with an A rating. The credit rating also seems to be on the verge of an upgrade. According to Fitch, an EBITDAR of 3.1 or less is enough for a higher rating.

CKHH’s ratings are supported by its business diversification across geographies and business lines, which provides stable cash flows and underpins its strong business profile. A solid record of conservative and prudent financial management and a coherent strategy also support the business profile.

Factors that could, individually or collectively, lead to a positive rating action/upgrade:

Provided that CKHH’s business profile remains unchanged:

– a sustainable EBITDAR net leverage ratio of 3.1x or less; and

– Positive free cash flow after acquisitions and dividends over a sustained period.

Source: FitchYou achieved a ratio of 3.3X last year and with continued deleveraging you could see a ratio below 3.0X.

So there’s nothing fundamentally wrong except that management has no regard for the share price whatsoever. There are no serious attempts to increase it. Yes, there’s that lax dividend policy tied to earnings, but beyond that they seem to be continuing to pull back despite a phenomenal balance sheet. Ideally they could commit to buying back shares with any remaining earnings or free cash flow after dividends. That could certainly shake up this sick puppy. But none of that is really happening. The key metrics show that the stock is incredibly undervalued. Some of the port and infrastructure multiples you see in the capital markets today are pretty wild and we think that range alone could justify almost all of the share price. There have been various sums of the parts numbers, like this one and this one, and they all suggest that the stock would need to triple to reach fair value. In our view, this is likely to remain a value trap with a 7% yield. In fact, it could even go lower. But there are some serious upside options here. Looking out over the next ten years, it’s very likely that an investor will earn at least 7% per year. For that to happen, the company would have to squander the remaining 9% of earnings yield year after year. On the other hand, if management decides that this share price doesn’t make sense, the stock could really soar. We bought some shares at $4.85 and plan to buy more at around $4.40.

Please note that this is not financial advice. It may look and sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and limitations.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.

CASA of Liberty, Chambers County receives $1,000 donation from Lions Club

Teachers’ strike to continue on Wednesday after failed talks