Fair value estimate of USA Truck, Inc. (NASDAQ:USAK)

")

Does USA Truck, Inc. (NASDAQ:USAK)’s June share price reflect its actual value? Today we will estimate the stock’s intrinsic value by projecting its future cash flows and then discounting them to today’s value. Our analysis will use the Discounted Cash Flow (DCF) model. Believe it or not, it’s not too difficult to follow, as you’ll see from our example!

Companies can be valued in many ways, so we would like to point out that a DCF is not perfect for every situation. For those who enjoy stock analysis, the analysis model from Simply Wall St listed here might be of interest.

Check out our latest analysis for USA Truck

Step by step through the calculation

We will use a two-stage DCF model which, as the name suggests, considers two phases of growth. The first stage is generally a higher growth phase that stabilizes toward the terminal value captured in the second “steady growth” stage. First, we need to get estimates of the next ten years of cash flows. Since we don’t have analyst estimates of free cash flow available, we extrapolated the previous free cash flow (FCF) from the company’s last reported value. We assume that companies with shrinking free cash flow will slow their rate of shrinkage and that companies with growing free cash flow will slow their growth rate over this period. We do this to account for the fact that growth tends to slow more in the early years than in later years.

A DCF is all about the idea that a dollar in the future is worth less than a dollar today. So we discount the value of these future cash flows to their estimated value in today’s dollars:

10-year free cash flow (FCF) forecast

|

2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

2030 |

2031 |

|

|

Leveraged FCF (in million US dollars) |

22.9 million US dollars |

22.3 million US dollars |

22.1 million US dollars |

22.1 million US dollars |

22.2 million US dollars |

22.4 million US dollars |

22.7 million US dollars |

23.0 million US dollars |

23.3 million US dollars |

23.7 million US dollars |

|

Source of growth rate estimate |

Estimated @ -4.08% |

Estimated @ -2.28% |

Estimated -1.02% |

Estimated -0.14% |

Estimated 0.48% |

Estimated 0.91% |

Estimated at 1.21% |

Estimated at 1.43% |

Estimated at 1.57% |

Estimated at 1.68% |

|

Present value (in million US dollars) discounted at 9.1% |

21.0 euros |

18.8 euros |

17.0 euros |

15.6 US dollars |

14.3 US dollars |

13.3 US dollars |

12.3 US dollars |

11.4 US dollars |

10.6 US dollars |

9.9 euros |

(“Est” = FCF growth rate, estimated by Simply Wall St)

Present value of 10-year cash flow (PVCF) = 144 million US dollars

After calculating the present value of future cash flows in the first 10-year period, we need to calculate the terminal value that takes into account all future cash flows after the first period. The Gordon growth formula is used to calculate the terminal value at a future annual growth rate equal to the 5-year average of the 10-year Treasury yield of 1.9%. We discount the terminal cash flows to today’s value at a cost of equity of 9.1%.

Final value (TV)= FCF2031 × (1 + g) ÷ (r – g) = $24 million × (1 + 1.9%) ÷ (9.1% – 1.9%) = $336 million

Present value of terminal value (PVTV)= TV / (1 + r)10= 336 million US dollars ÷ (1 + 9.1%)10= 140 million US dollars

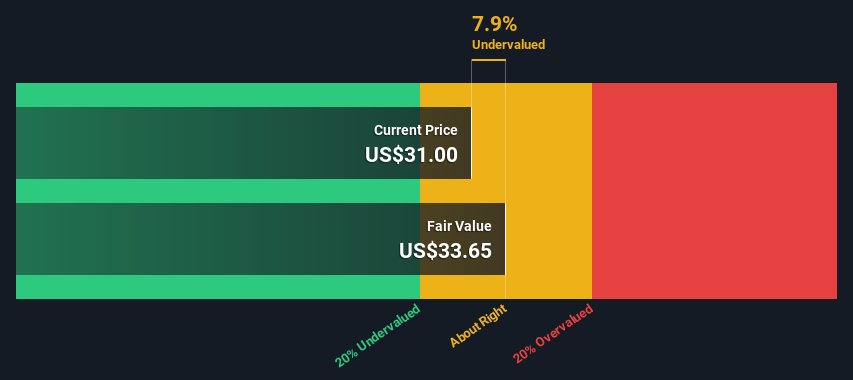

The total value or equity value is then the sum of the present value of future cash flows, which in this case is $284 million. To get the intrinsic value per share, we divide this by the total number of shares outstanding. Compared to the current share price of $31.0, the company appears to be about fair value, at a 7.9% discount to the current share price. However, keep in mind that this is only an approximate valuation and as with any complex formula, where there’s garbage in, there’s garbage out.

The assumptions

The above calculation relies heavily on two assumptions. The first is the discount rate and the other is cash flows. Part of investing is making your own assessment of a company’s future performance, so try the calculation yourself and check your own assumptions. DCF also does not take into account the possible cyclicality of an industry or a company’s future capital needs and therefore does not provide a complete picture of a company’s potential performance. Since we are viewing USA Truck as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or weighted average cost of capital, WACC) which takes debt into account. In this calculation, we used 9.1%, which is based on a leveraged beta of 1.698. Beta is a measure of a stock’s volatility relative to the market as a whole. We get our beta from the industry average beta of globally comparable companies with an imposed limit of between 0.8 and 2.0, which is a reasonable range for a stable company.

Next Steps:

While the DCF calculation is important, it should not be the only metric you consider when researching a company. It is not possible to get a foolproof valuation using a DCF model. Instead, the best use of a DCF model is to test certain assumptions and theories to see if they would lead to an undervaluation or overvaluation of the company. For example, changes in the company’s cost of equity or risk-free interest rate can significantly affect the valuation. For USA Truck, we have compiled three other elements you should evaluate:

-

Risks: Consider, for example, the ever-present specter of investment risk. We have identified 1 warning signal with USA Truck, and understanding this should be part of your investment process.

-

Future income: How does USAK’s growth rate compare to competitors and the overall market? Learn more about analyst consensus numbers for the coming years by using our free chart of analyst growth expectations.

-

Other high-quality alternatives: Like a good all-rounder? Explore our interactive list of high-quality stocks to get a sense of what else you might be missing out on!

PS The Simply Wall St app runs a discounted cash flow valuation for every stock on the NASDAQGS every day. If you want to find the calculation for other stocks, just search here.

Do you have feedback on this article? Are you concerned about the content? Get in touch directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment based solely on historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

Bebe Rexha claims she can “bring down” the music industry with her knowledge

New construction worth $680 million drives up property values in the county