Homebuyers are still on strike even as mortgage rates fall to lowest levels since March, but refinancings rise to highest levels since August 2022

A trend we are observing: While refinancing rose from its collapsed levels, the Fed’s MBS QT increased for the fourth consecutive month.

By Wolf Richter for WOLF STREET.

The average 30-year fixed-rate conforming mortgage rate fell to 6.87% in the latest reporting week, the lowest since mid-March, the Mortgage Bankers Association reported today. Not so ironically, two things happened, the MBA also reported today:

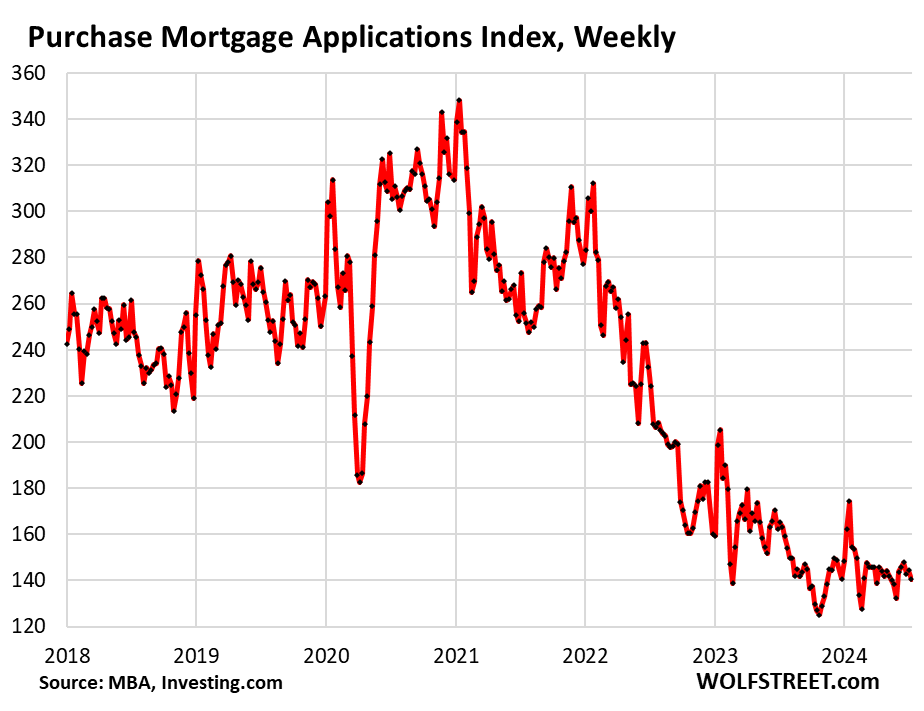

- The number of mortgage applications to purchase a home fell to the lowest level since early June as prospective homebuyers continued to strike and wait for lower prices and interest rates.

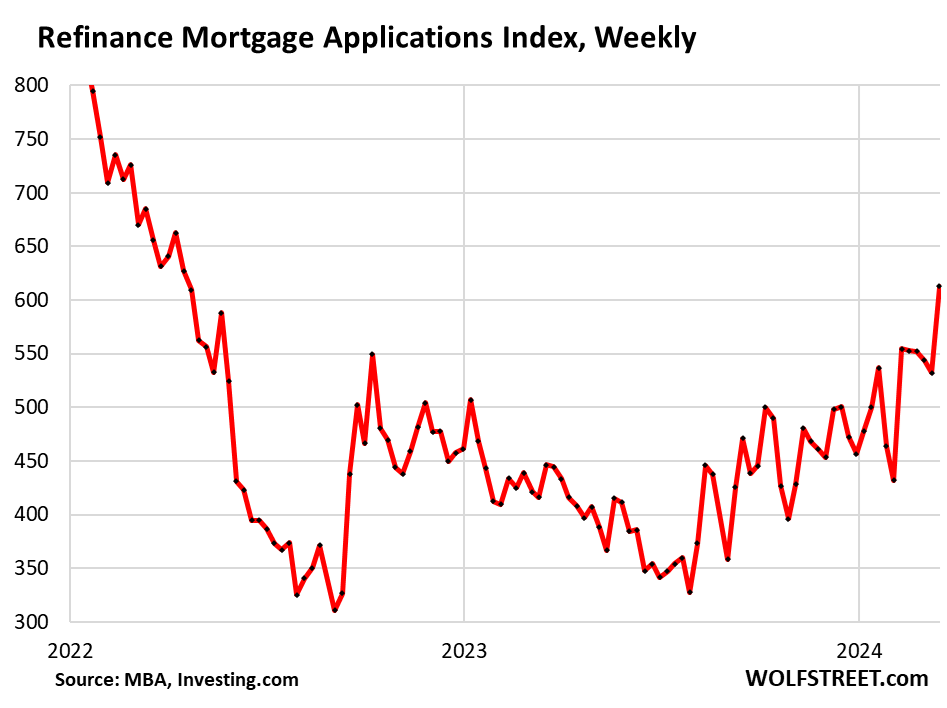

- Applications to refinance an existing mortgage rose to their highest level since August 2022 and have nearly doubled since last November’s plunge, which has implications for the Fed’s QT.

The mortgage rate of around 7% has been a fixture of the real estate market since July 2023, briefly reaching 7.9% in October 2023. It has been above 6% since September 2022.

The problem is not mortgage rates, but real estate prices. A 7% mortgage rate used to be a good deal. From 1970 to 2001, mortgage rates ranged between 7% and 18%. Relatively lower real estate prices made these higher mortgage rates possible.

But when mortgage rates fell as low as 5.5% in 2005, they fueled the housing bubble 1, which led to the housing crisis from 2006 to 2012. Mortgage rates fell below 5% in 2010 and then mostly hovered between 3.5% and 4.5% until they crashed to 2.5% in 2020. Those mortgage rates, especially the 3% during the pandemic, led to incredible home price increases, and those home prices don’t work with anything but 3% mortgages—or even with them.

Buyers’ strike continues, prices are too high.

Real estate prices are simply too high even for cash buyers, home purchases have declined, and the number of home purchases requiring a mortgage has fallen by almost half compared to pre-pandemic levels in 2019.

Mortgage applications to purchase a home fell to their lowest level since early June 2024 in the latest reporting week, down 14% year-on-year and 47% from the same week in 2019.

Mortgage applications are an early indicator of home sales volume, and sales volume is dismal even as the number of active listings has risen to multi-year highs. In November 2023, mortgage applications reached their lowest level since 1995.

This is a clear sign that potential buyers are waiting for lower prices and lower mortgage rates. They are still on a buyer’s strike, even as sellers become more willing to sell – hence the rising inventory and price reductions.

The number of applications for mortgage refinancing jumped from a previously low level.

The number of mortgage applications to refinance a home began to decline in 2022 as mortgage rates skyrocketed. Non-cash-out refinances have almost disappeared. According to data from the AEI Housing Center, most of the refinances completed are cash-out refinances.

But if we look more closely, we can see that refinancing volumes have been trending upwards since November 2023 from their collapsed levels, jumping to their highest level since August 2022 in the last reporting week after nearly doubling since November 2023.

That’s just a guess. It looks like an increasing number of homeowners seeking a cash-out refinance have been trying to wait out the 7% mortgage rates. They thought for months or a year that this too would pass. But now this too is still not over, and they can’t wait any longer and have pulled the trigger:

As a Fed observer here…

We keep an eye on refinances because an increase in refinance activity increases the QT pace with respect to the Fed’s MBS holdings. MBS are taken off the balance sheet when the underlying mortgages are repaid or paid off. A refinance pays off the old mortgage and passes the principal on to MBS holders. The QT pace for MBS was about $14 billion per month in early 2024, reflecting the historic low in refinance applications in November.

But the pace of MBS QT has increased for the fourth month in a row, reaching $19 billion in June, reflecting refinancing requests through about April. The current increase in refinancing will not be reflected in the Fed’s balance sheet until the repayments of the old mortgages that have been paid off start arriving at the Fed.

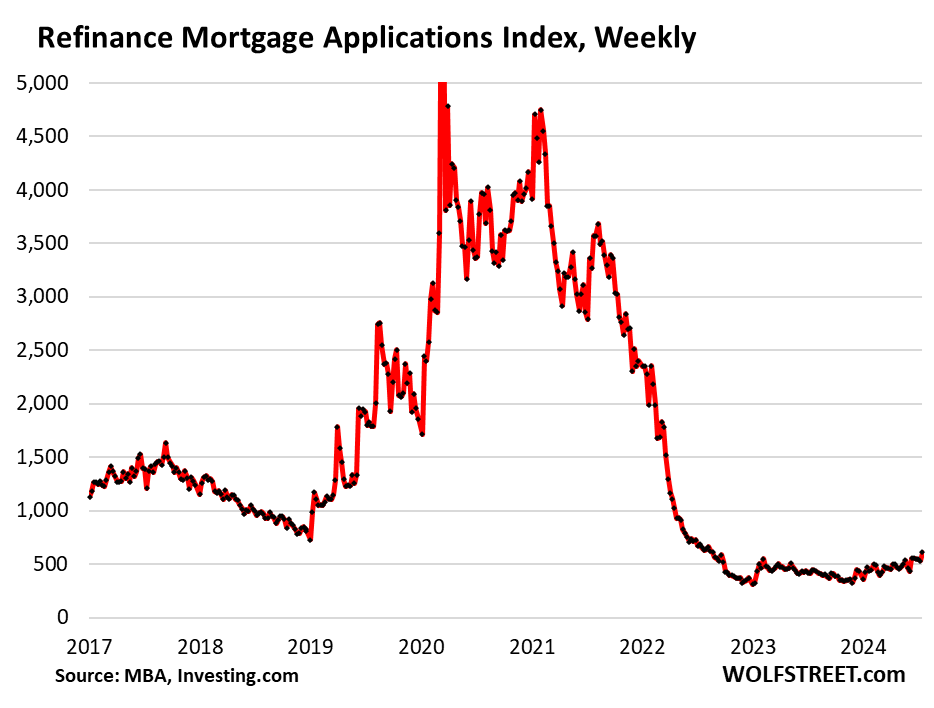

Refinancing and interest rates, the long-term view …

Refinance applications are still down 66% from the same week in 2019 and down 81% from the same week in 2021. Refinances are a function of mortgage rates, and they move dramatically in the opposite direction of mortgage rates. The chart shows this inverse relationship between refinance applications (red) and mortgage rates (blue).

If you enjoy reading WOLF STREET and want to support it, you can donate. I really appreciate it. Click on the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()

Blackmail at United Club: Staff demands for tips make passengers angry – now it’s enough

What music is Memphis famous for? Blues, rock’n’roll and much more