Ellington Financial: Issuing Series A Preferred Stock with Yields of Over 10% (NYSE:EFC)

")

matdesign24

introduction

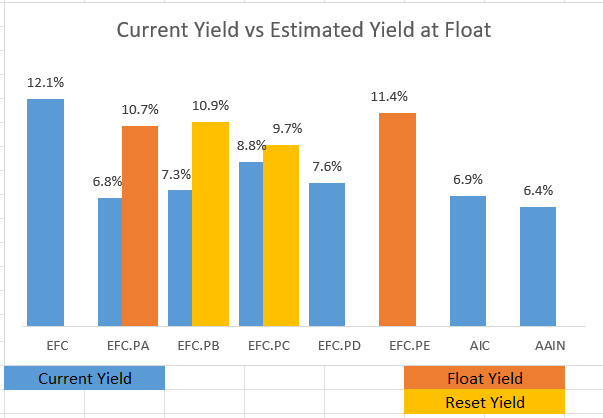

Ellington Financial (NYSE: EFC) is a real estate investment trust that invests primarily in residential mortgages. The company uses leverage to increase its earnings. Ellington Financial shares currently pay a dividend yield of over 13%. The company also offers five high-yield preferred stock options. One of these preferred shares (NYSE:EFC.PR.A) is just a quarter away from the variable yield and, based on today’s interest rates, would yield 10.7% at the variable yield in the fall, which I believe makes the stock an attractive investment for income investors.

Microsoft Excel API

Ellington Financial earnings performance

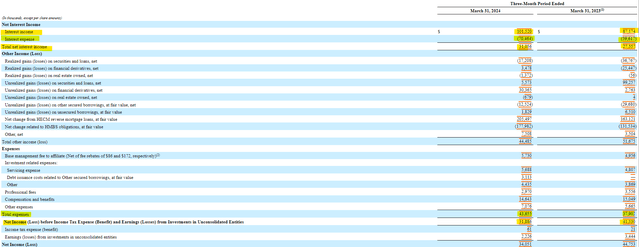

Companies that use debt to make loans struggle with higher borrowing costs and struggle to increase earnings to keep up with higher interest rates. Fortunately, Ellington Financial’s interest income grew faster than interest expense. Net interest income (interest income less interest expense) increased $3.5 million, or more than 10% to $31 million in the first quarter. Unfortunately, the increase in net interest income was more than offset by the $6 million increase in expenses related to debt issuance costs. Ultimately, net income decreased by almost $10 million to $31 million.

SEC10-Q

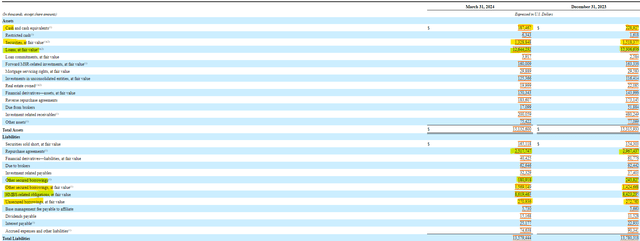

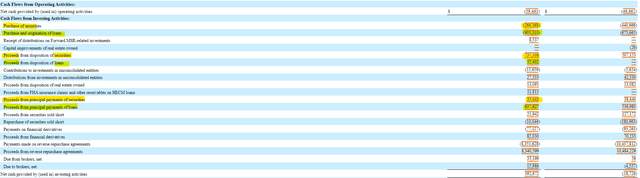

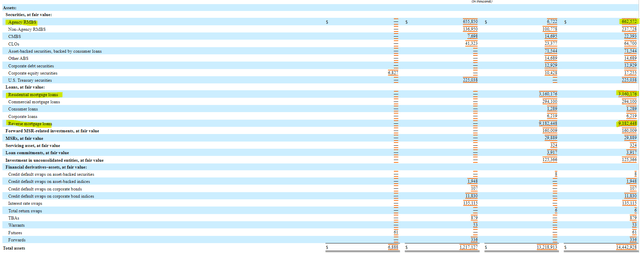

Ellington Financial’s balance sheet shows some interesting changes the company made in the first quarter. Ellington sold some of its securities holdings and used the proceeds to purchase more loans (see cash flow statement), which now represent over 80% of total assets. On the debt side, the company has moved away from short-term repurchase agreements and focused on secured loans and HMBS-related loans. Shareholders’ equity remained stable in the first quarter.

SEC10-Q SEC10-Q

A deeper look into investments and debt

Ellington Financial invests in a variety of loans, but over 90% of its loans are concentrated in reverse mortgage loans and residential mortgage loans, with reverse mortgage loans making up the vast majority of the portfolio. While the company has $660 million in agency-backed MBS holdings, that only represents 5% of the total portfolio. Investors can expect the value of these assets to increase when interest rates are lowered, benefiting shareholder value and the stock price.

SEC10-Q

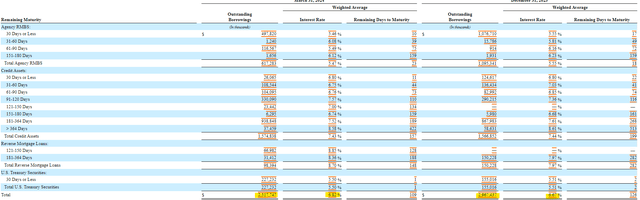

On the debt side, the company has $2.5 billion in repurchase agreements. The weighted average interest rate on this debt is a whopping 6.8%, but the average maturity is just 109 days, meaning investors can quickly anticipate future rate cuts to have a positive impact on earnings. The average interest rate on HMBS debt fell more than 20 basis points to 6.2%, which explains why Ellington moved away from repurchase agreements.

SEC10-Q SEC10-Q

Risks for Ellington Financial

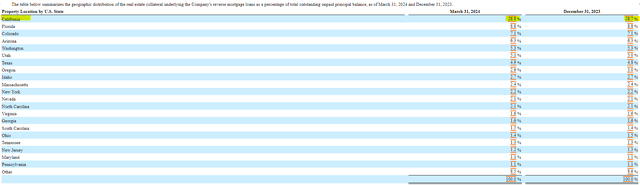

Although interest rates are expected to fall, investors should note that an unexpected rise in interest rates would severely impact the company’s earnings. Additionally, there is no evidence of insurance (such as agency MBS) in case the company’s investments perform poorly; therefore, Ellington will have to bear the full burden of any bad loans. There is also no provision for loan losses, meaning the company would likely take possession of the properties, liquidate them, and write off the difference as a loan loss. Finally, Ellington Financial’s reverse mortgage loans are heavily concentrated in California, which could be detrimental if any risks (climate, regulation, etc.) arise on the West Coast.

SEC10-Q

Series A or Series E

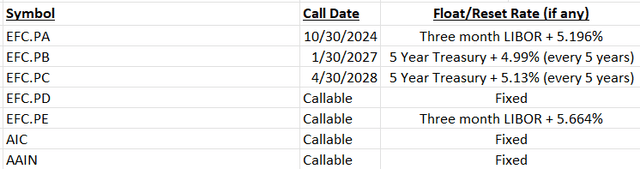

Investors may notice that Series A is not the only floating stock. Series E preferred stock (EFC.PR.E) is already trading at a forward rate of over 11% floating, and two other securities are resetting at higher prices. Investors should avoid the two resetting securities because their reset dates are not until 2027 and 2028, respectively. Series E shares are attractive, but currently trade above par and are subject to call rise risk. Although Series A shares are expensive, they currently trade just below par and retain a fixed dividend.

QuantumOnline/Author Table

Diploma

Ellington Financial’s earnings were hurt by higher expenses, but the company was able to increase its net interest income and cover its preferred dividends. The possibility of lower interest rates may help the company, but the concentration of loans, their geographic spread, and the prospect of performance issues hurting earnings keep me away from the common stock. I am confident that the Series A preferred stock will last longer than the Series E preferred stock and that interest rates will remain high enough to support earnings yields above the other fixed-rate preferred stocks.

Jelly Roll to provide theme music for WWE SummerSlam, says Triple H

Travis Kelce and Tom Cruise meet at Taylor Swift’s London concert